A Finance Director is ready to appoint a new board member, tidy up the group structure, and get the next filing over the line. The paperwork is routine. The timeline is tight. Then the process hits a new constraint. The filing route the business has always used is changing, and a Companies House submission that used to feel administrative now carries a compliance dependency.

That is where the authorised corporate service provider acsp regime matters.

For growing UK companies, this is not a niche rule for formation agents and legal technicians. It affects how businesses appoint directors, manage statutory filings, and keep corporate actions moving without delays. A company turning over £1 million to £15 million usually has little tolerance for process friction. If a filing stalls, the impact can spread into banking, investor conversations, internal approvals, and Year End work.

The regime sits under the Economic Crime and Corporate Transparency Act 2023 and changes who can file on behalf of companies in the UK. It is part of a wider push to improve corporate transparency and reduce fraud. For leadership teams, the practical issue is clearer. Know when an ACSP is required, choose the right provider, and make sure filing activity does not become a growth bottleneck.

For businesses still reviewing their wider Companies House processes, it also helps to understand the filing basics around incorporation and entity setup, particularly where future changes to officers or structure are likely. A useful starting point is this guide on how to incorporate a limited company in the UK.

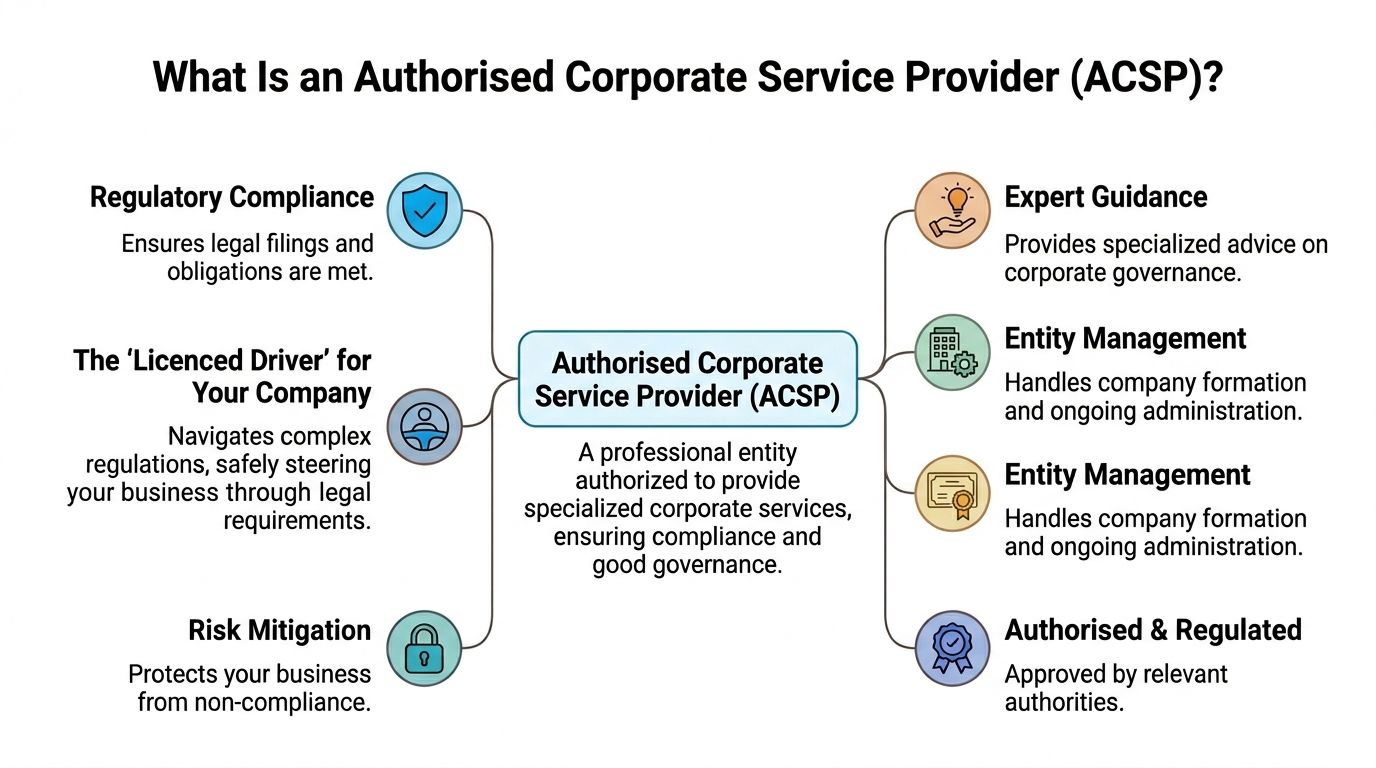

What Is an Authorised Corporate Service Provider

An Authorised Corporate Service Provider is an intermediary approved to carry out certain Companies House activities on behalf of clients. A useful way to think about it is this. If company filings are the road, the ACSP is the licenced driver. The business still decides where it needs to go, but the ACSP is the party formally permitted to handle the route in line with the rules.

The practical definition

The regime was established under the Economic Crime and Corporate Transparency Act 2023, with mandatory ACSP status required for all third-party filings from spring 2026, and registration for agents providing identity verification services opened on 18 March 2025 according to 1st Formations’ summary of the ACSP regime.

That matters because many businesses have historically treated Companies House filing support as a back-office convenience. Under the new framework, it becomes a regulated gateway. An adviser filing on behalf of a company is no longer just helping with admin. That adviser must be properly authorised where the rules require it.

In plain terms, an ACSP can help verify identity and submit information to Companies House on behalf of clients. For the client company, that means less uncertainty about whether a filing route is valid and more confidence that an essential corporate action will be accepted.

Why the regime exists

The point is not bureaucracy for its own sake. The UK is trying to improve the integrity of the public register, strengthen identity verification, and make it harder for bad actors to hide behind weak filing controls.

For leaders responsible for finance and governance, the commercial takeaway is straightforward:

- Corporate actions need a compliant route. Director appointments, entity changes, and filing activity cannot rely on outdated assumptions.

- Identity checks now sit closer to filing activity. The compliance standard is higher than many businesses are used to.

- Provider quality matters more. A weak filing partner creates operational risk, not just admin irritation.

A broader primer on Financial Crime and Compliance for UK Businesses can help boards and finance teams place ACSPs in the wider context of governance, anti-money laundering controls, and business risk.

A sensible board treats ACSP readiness as part of operational resilience, not just legal housekeeping.

The Commercial Risks of Getting This Wrong

The legal angle gets attention first. The business angle is usually where the pain lands.

Under the Economic Crime and Corporate Transparency Act 2023, failure to use an ACSP for relevant filings can lead to significant disruption. It can trigger offences punishable by fines or criminal prosecution, and it can prevent important filings such as director appointments, as noted in Chartered Accountants Ireland’s guidance on UK ACSPs.

Where the problem shows up first

Most SMEs do not notice regulatory change when the law is passed. They notice it when something important stops moving.

That usually happens in one of four situations:

- Board changes. A business needs to appoint a director quickly because a lender, investor, or restructuring process requires it.

- Year End filings. Statutory work is ready, but the filing route creates a last-minute hold-up. Businesses that rely on external support for Statutory Accounts preparation and filing should pay close attention here.

- Corporate housekeeping. A change to the registered office, company officers, or ownership records becomes more urgent than expected.

- Transaction readiness. Due diligence begins, and advisers discover governance gaps or weak filing controls.

A blocked filing rarely stays contained. It can delay internal approvals, increase pressure on the finance team, and create avoidable friction with external stakeholders.

The hidden cost is loss of momentum

For a scaling company, speed matters. Not reckless speed. Controlled speed.

A filing issue can affect more than compliance:

| Business area | What can go wrong if filing support is not compliant |

|---|---|

| Funding activity | Investors and lenders may question governance discipline if basic corporate actions are delayed |

| Cash flow planning | Time-sensitive decisions can slip while management waits for formal changes to be processed |

| Recruitment at leadership level | A key appointment may not land when needed |

| Group restructuring | Internal changes can stall, leaving the wrong entity carrying contracts or liabilities |

The direct penalty risk is serious enough. The indirect cost is often worse. Senior management gets pulled into administrative firefighting instead of pricing, margin, hiring, or delivery.

The true commercial cost is not only the sanction. It is management time diverted from growth into preventable compliance repair.

What does not work is assuming the external accountant, company secretary, or adviser will “sort it” without checking their authorisation status and process readiness. What works is mapping the filings the business is likely to need over the next year, then making sure the route for each one is secure before urgency arrives.

Your Due Diligence Checklist for Choosing an ACSP

Choosing an ACSP is not a procurement formality. It is a governance decision with operational consequences.

Strong provider selection starts with the same mindset used in wider risk reviews. This short explanation of due diligence in business is useful for framing the standard leadership teams should expect before relying on any external party for important compliance activity.

Questions worth asking before appointing anyone

A good shortlist should survive direct questions. If a provider answers vaguely, that is already useful information.

-

Are they on the public register?

Companies House maintains a live list of authorised providers. A business should confirm the provider is listed, not merely planning to register. -

Who supervises them for anti-money laundering purposes

Eligibility is restricted to entities supervised by recognised UK AML bodies such as HMRC, FCA, ACCA, ICAEW, SRA, or ICA. If the answer is unclear, the risk is clear. -

What is their process for identity verification?

The right question is not whether they “do ID checks”. It is how they handle them, how records are retained, and how exceptions are escalated. -

How quickly can they handle urgent filings?

Service levels matter. A provider may be compliant but still too slow for a business that needs same-week action on director changes or registered office updates. -

Can they support connected services?

If the provider also supports registered office arrangements, this can reduce fragmentation. For businesses reviewing that area, acting as a registered office is often part of the same governance conversation.

What an effective provider relationship looks like

The strongest ACSP relationships are boring in the best sense. Clear onboarding. Clear evidence requirements. Clear turnaround expectations. No drama when an urgent filing appears.

A practical selection test is whether the provider can explain the process in commercial language. If they default to jargon, the business will probably feel that confusion again at the point of pressure.

Useful signs include:

- Defined escalation routes for urgent corporate actions

- Written scope covering filing responsibilities and limitations

- Consistent requests for evidence, rather than ad hoc chasers

- Comfort with multi-entity structures, if the group has them

An ACSP should reduce noise, not add another layer of it.

How a Firm Becomes an Authorised Corporate Service Provider

A finance team often finds out who is properly authorised only when something time-sensitive lands. A director appointment needs filing, a lender wants the group structure confirmed, or a transaction timetable depends on Companies House moving without friction. If the adviser handling that work is not set up correctly, the delay hits the company, not just the adviser.

For SMEs in the £1m to £15m range, that is the core commercial point. ACSP status is not a marketing label. It determines who can carry out certain filing and identity verification work in a way that keeps corporate actions moving.

Entry starts with regulated status

A firm cannot decide to become an ACSP because clients ask for it. It must already sit within a recognised anti-money laundering supervisory framework. In practice, that usually means the provider is an accountancy, legal, or regulated financial services firm already overseen by an approved UK body.

There is also a formal application to Companies House, and the application fee is £55, as set out in the official Companies House guidance on applying to register as an ACSP.

The fee is minor. The primary test is whether the firm already has the people, processes, and oversight to carry out identity verification and filing work properly.

The application is administrative. The operating model is the harder part

A provider needs clear internal authority over who can submit filings, verify identity, keep records, and deal with exceptions. Senior oversight matters because errors do not stay administrative for long. They become missed deadlines, rejected filings, and awkward conversations with banks, investors, and counterparties.

That is why good providers build the process before they rely on the registration. They set approval controls, record-keeping standards, and escalation routes for unusual cases.

Clients should read that correctly. ACSP status shows a firm has crossed the entry threshold. It does not, by itself, tell you whether the provider can handle pressure well.

Ongoing compliance is what separates a usable provider from a risky one

Once authorised, the firm has continuing duties. It must keep records of identity verification work and keep its own registration details up to date with the registrar. Those requirements shape how the provider operates day to day.

For a growing business, that has direct consequences. A provider with disciplined records and defined ownership is usually easier to work with when a filing becomes urgent. A provider treating ACSP work as a side task is more likely to create bottlenecks.

Cheap support can cost more than it saves. If a share issue, director change, or group restructure stalls because the filing route is weak, the commercial damage usually shows up elsewhere first. Funding timetables slip. Completion dates move. Internal teams lose time fixing avoidable admin.

A credible ACSP is judged less by the fact it registered and more by whether it can keep filings accurate, evidence complete, and responsibility clear when the pressure is on.

Frequently Asked Questions

Do I need an authorised corporate service provider acsp for every Companies House filing

Not every business action will feel different immediately, but third-party filing requirements are tightening. If another party files on behalf of the company in a situation covered by the regime, that provider needs to be properly authorised. Businesses with regular filing activity should review the full process early rather than waiting for an urgent event.

Can a company director just handle identity verification without an ACSP

In some cases, identity verification can be handled directly through Companies House rather than through an intermediary. The practical issue is not whether direct action is possible. It is whether the business wants directors and finance staff managing another compliance workflow internally when speed and accuracy matter.

What happens if an accountant is not registered as an ACSP

If the accountant is carrying out filing activity that requires ACSP status and is not registered, the business can face disruption. That can mean delayed submissions, governance friction, and a need to switch filing routes at the worst possible moment. This overview of Companies House requirements is useful for checking where those pressure points sit.

How much does ACSP registration cost for a provider

The registration fee is £55 for the applicant, based on the ACSP registration framework cited earlier. That is the provider’s registration cost. It is separate from whatever commercial fee the provider may charge clients for identity verification, filing support, or ongoing company secretarial work.

When should an SME review its ACSP arrangements

The best time is before any planned corporate action. If the business expects board changes, restructuring, investor due diligence, or Year End filing activity, it should review provider status and process readiness in advance. Leaving it until a filing is urgent reduces options.

Secure Your Compliance and Focus on Growth

The ACSP regime changes a part of company administration that many SMEs have historically treated as routine. It is no longer enough to assume a trusted adviser can file because they always have. Authorisation, process discipline, and evidence handling now matter far more.

For businesses in the £1 million to £15 million turnover range, the commercial issue is clear. Growth plans depend on clean execution. Director appointments, structural changes, and statutory filings need to move when the business needs them to move. That only happens if the compliance route is already in place.

The most effective response is practical rather than dramatic:

- identify which filings and corporate actions the business is likely to need

- confirm whether the current adviser is properly authorised where required

- test turnaround times and evidence requests before urgency hits

- treat filing compliance as part of business continuity, not just governance admin

Handled early, ACSP readiness becomes another controlled process inside the finance function. Ignored, it can create the kind of delay that arrives at exactly the wrong time.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.

Secure your company’s compliance today. Book a free 15-minute consultation with striveX Ltd to review your Companies House filing requirements with the expert team.