Growth can look healthy on the profit and loss account while cash feels permanently tight. Orders are up, the team is busy, and margins may even be improving, yet the bank balance still dictates every decision. That gap usually comes down to timing. Customers pay later than expected, stock sits too long, and suppliers want settling before cash has fully come back in.

That is why working capital management matters so much for UK businesses turning over £1 million to £15 million. It is not an academic finance term. It is the discipline of controlling how quickly cash moves through the business so growth does not create strain.

A business with strong working capital management has more room to hire, buy stock at the right time, invest in systems, and avoid leaning on short-term borrowing unless it makes commercial sense.

What Is Working Capital Management?

Working capital management is the control of short-term assets and short-term liabilities so the business can operate smoothly, pay what it owes, and keep enough cash available to grow.

At a practical level, it covers three moving parts:

-

Money owed in from customers

-

Cash tied up in stock or work in progress

-

Money owed out to suppliers, lenders, and HMRC

A simple formula sits underneath it:

Working capital = current assets – current liabilities

That sounds technical, but the commercial meaning is straightforward. If too much cash is trapped in debtors or stock, the business may be profitable and still feel under pressure. If liabilities fall due before cash comes in, management ends up reacting rather than planning.

Working capital in plain English

A useful way to view working capital is this. It measures how much effort the business needs to turn activity into usable cash.

For a manufacturer, that may mean buying materials, holding stock, producing goods, invoicing the customer, then waiting to be paid. For a construction company, it may mean funding labour and subcontractors before an application for payment is settled. For a SaaS business, it may look cleaner, but deferred income, tax liabilities, and slow enterprise collections can still create a squeeze.

Good working capital management turns trading activity into decision-making freedom.

The aim is not to hold the maximum amount of cash at all times. The aim is to avoid unnecessary cash drag. Strong businesses do not just look at profit. They manage the route from sale to banked cash.

The metric that matters most

The most useful operating measure is the Cash Conversion Cycle, often shortened to CCC. It shows how long cash is tied up between paying out and collecting back in.

When directors ask what is working capital management in real terms, this is usually the answer. It is the discipline of shortening that cycle where sensible and protecting liquidity without weakening the business.

That means collecting promptly, carrying the right level of stock, and using supplier terms intelligently rather than carelessly. It also means linking finance, operations, sales, and tax planning, because cash problems rarely sit in one department alone.

Why Working Capital Is the Lifeblood of a Scaling UK Business

Scaling businesses often assume cash pressure is temporary. Sometimes it is. Often it is structural.

When turnover rises, receivables usually rise with it. Stock requirements increase. VAT bills become larger. Payroll expands before collections fully catch up. A business can therefore grow and feel poorer at the same time.

According to research on the treasury cost of tied-up working capital, poor working capital practices in the UK tie up significant cash that could fund growth. Net working capital days reached a record high in 2020, businesses in sectors including manufacturing and construction saw significant deteriorations, and the Federation of Small Businesses reported in 2022 that 40% of UK firms with £2 million to £10 million turnover cited late payments as a primary liquidity killer, contributing to thousands of SME insolvencies.

That matters because cash shortages do not stay inside the finance function. They affect the whole operating model.

What poor working capital really costs

When cash is trapped, directors usually face one of these trade-offs:

-

Hiring is delayed because payroll feels too risky

-

Supplier relationships tighten because payment timing becomes reactive

-

Growth opportunities are missed because the business cannot fund the gap before cash arrives

-

Borrowing increases even though the business is already generating turnover

-

Management time is wasted chasing short-term fixes instead of making strategic decisions

A business in this position may still be solvent, but the margin for error gets thin. Where the pressure becomes severe, directors also need to understand the severe consequences of trading whilst insolvent, because cash distress can move from operational inconvenience to legal and personal risk faster than many expect.

Why this is a board issue, not a bookkeeping issue

Working capital is often treated as something to review after month end. That is too late. By then, the problem is already on the balance sheet.

The strongest operators use working capital as a management tool. They ask:

-

Are customers paying in line with agreed terms?

-

Is stock being purchased because demand requires it, or because planning is weak?

-

Are supplier terms supporting growth, or are good terms being wasted?

-

Are tax liabilities visible early enough to avoid last-minute pressure?

For many growing firms, this is the point where finance support needs to become more commercial. A strong reporting and control process, such as the discipline described in what a virtual financial controller can do for your business, gives leadership a clearer view of where cash is going.

Profit is an outcome. Cash is a constraint. Working capital management sits between the two.

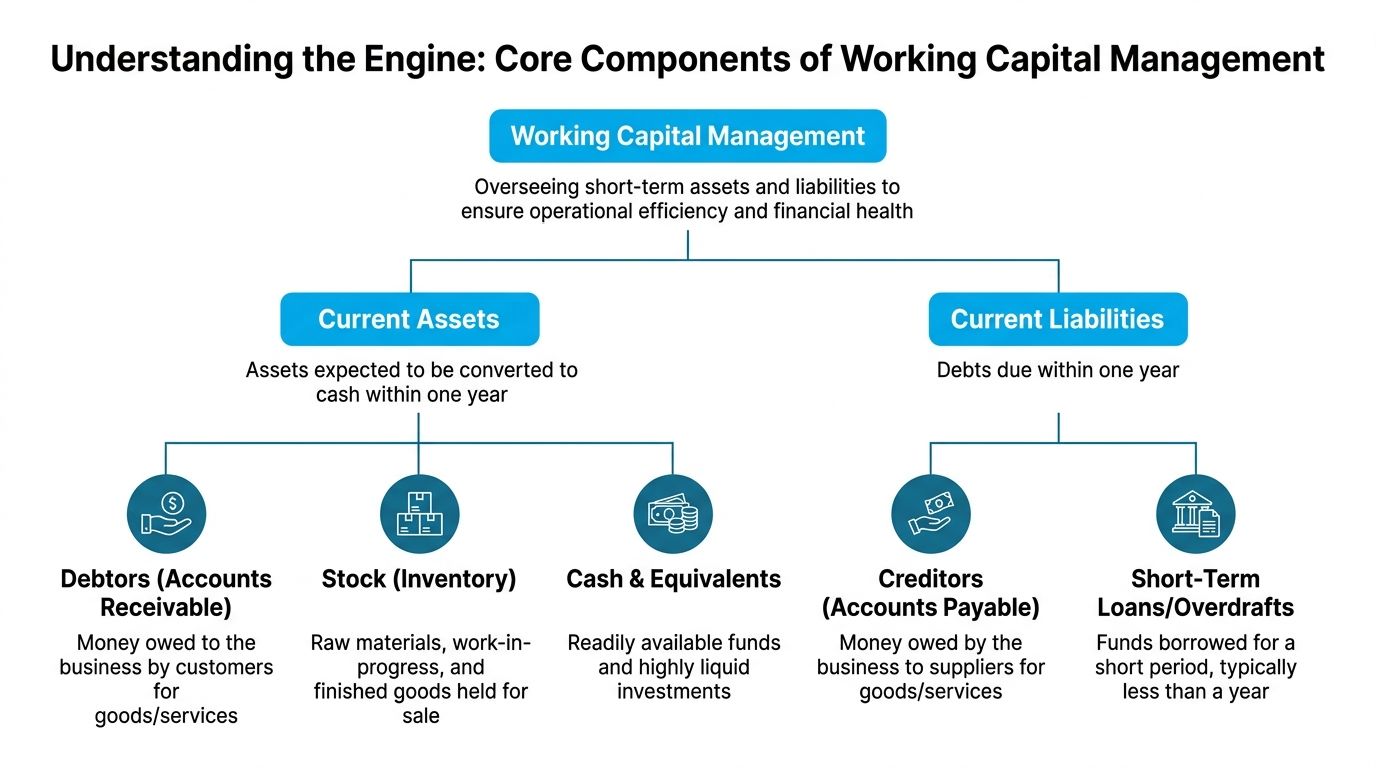

The Core Components of Working Capital Management

Working capital management becomes much easier once the moving parts are separated. Most cash pressure comes from a handful of short-term balance sheet items, not from some vague sense that “cash is tight”.

Current assets

Current assets are items expected to turn into cash, or be used up, within one year. In most scaling SMEs, the main ones are:

-

Debtors. Amounts customers owe after invoicing.

-

Stock or work in progress. Cash already spent on items not yet sold or completed.

-

Cash and equivalents. Money already available to meet obligations.

These assets support trading, but they do not all help liquidity equally. Cash is immediate. Debtors are only useful once collected. Stock can be valuable commercially and still unhelpful in a cash squeeze.

Current liabilities

Current liabilities are amounts the business must settle within one year. Typical examples include:

-

Creditors owed to suppliers

-

VAT and PAYE liabilities

-

Corporation Tax falling due

-

Short-term borrowing or overdraft use

-

Accruals and other near-term obligations

These liabilities are not bad. In fact, sensible supplier credit is part of healthy working capital management. The issue is timing. If liabilities crystallise before assets convert into cash, pressure builds quickly.

Net working capital

Net working capital is the gap between those two groups:

| Measure | Formula | What it tells management |

|---|---|---|

| Working capital | Current assets minus current liabilities | The short-term liquidity cushion |

| Positive working capital | Assets exceed liabilities | There is headroom, though cash may still be trapped |

| Negative working capital | Liabilities exceed assets | The business may be exposed to timing pressure |

A positive figure is not automatically efficient. If the business is carrying excessive debtors or too much stock, capital is still tied up unnecessarily.

The metric that matters most

The operational heartbeat is the Cash Conversion Cycle.

CCC = DIO + DSO – DPO

In plain English, it measures how long it takes for cash spent on operations to return to the bank account through customer receipts.

-

DIO is how long stock sits before sale

-

DSO is how long customers take to pay

-

DPO is how long the business takes to pay suppliers

A shorter cycle usually means better liquidity. Not always. Some businesses shorten the cycle in the wrong way by under-ordering stock, pushing customers too hard, or damaging supplier relationships. The point is to improve speed without weakening service or resilience.

The best working capital decisions balance liquidity, margin, customer experience, and operational continuity.

This is why finance teams should not manage working capital in isolation. Sales controls DSO behaviour. Operations influences DIO. Procurement and leadership shape DPO. The numbers belong to finance, but the drivers sit across the business.

Key Performance Indicators You Must Track

A single working capital number is useful, but it does not tell management where the problem sits. Effective diagnosis comes from three operating KPIs.

Days Sales Outstanding

DSO = trade debtors / credit sales x number of days

DSO measures how long customers take to pay after invoicing. If DSO creeps up, the business is effectively funding customers for longer.

For many UK firms, high DSO is not caused by bad debt alone. It often comes from avoidable process issues:

-

Invoices sent late

-

Purchase order disputes

-

Weak collection discipline

-

Sales teams agreeing terms finance never approved

-

Applications or valuations submitted incorrectly

For UK logistics SMEs, working capital benchmarks for SMEs place DSO at 45 to 55 days and DPO at 60 to 75 days. The same source states that top-quartile working capital performers report 12% higher cash flow margins, often helped by real-time DSO tracking that accelerates receivables by 10 to 15 days.

A low DSO is generally positive, but not if it comes from offering discounts that unnecessarily erode margin.

Days Inventory Outstanding

DIO = average inventory / cost of sales x number of days

DIO shows how long stock sits before being sold or used. In manufacturing, distribution, and construction, this is often the quietest source of cash leakage because stock feels productive. It is still cash.

High DIO can point to:

-

Overstocking for “just in case” demand

-

Weak demand forecasting

-

Slow-moving or obsolete lines

-

Excess raw materials purchased without firm order visibility

-

Work in progress that is operationally stuck

A lower DIO usually improves liquidity, but directors need to stay practical. Cutting stock too hard can create missed deliveries, overtime costs, emergency buying, and weaker customer service.

Days Payables Outstanding

DPO = trade creditors / cost of sales x number of days

DPO measures how long the business takes to pay suppliers. This is the main lever on the liabilities side.

A business with low DPO may be paying too quickly and giving away free liquidity. A business with very high DPO may be funding itself by straining suppliers.

The useful question is not “how late can payment be pushed?” It is “what payment behaviour supports both cash flow and a dependable supply chain?”

DPO should be managed deliberately, not through drift, excuses, or firefighting.

A simple way to read the three KPIs together is set out below:

| KPI | Rising number usually means | Falling number usually means |

|---|---|---|

| DSO | Slower collections, more cash tied in debtors | Faster collections, better liquidity |

| DIO | More cash tied in stock | Leaner stock holding |

| DPO | More supplier credit retained | Faster payment outflows |

The value of these measures is not the formula. It is the conversation they force. They show whether the business is slow to collect, too heavy on stock, or paying out before it needs to.

Practical Strategies to Optimise Your Cash Conversion Cycle

Many businesses attack working capital in the wrong order. They chase an overdraft first, then look at the root cause later. That can be necessary in a genuine crunch, but it is not a strategy.

The better approach is to work through the cycle methodically. That matters even more because, according to analysis of working capital management and business success, 44% of SMEs struggle with working capital gaps exceeding 60 days. The same source notes that extending payables beyond 90 days carries 28% higher supplier default risks, and that linking R&D tax credit cashbacks averaging £250,000 for eligible tech firms can help bridge gaps more proactively.

Reducing DSO without damaging customer relationships

The aim is faster cash, not friction for the sake of it.

Useful tactics include:

-

Invoice immediately. Delayed invoicing pushes the whole cycle back.

-

Make commercial terms explicit. Credit terms should be agreed before work starts, not argued about after delivery.

-

Separate billing from chasing. The team issuing invoices should not assume collections are happening.

-

Use aged debt reviews weekly for overdue balances, disputes, and promised payment dates.

-

Escalate early when a customer repeatedly pays outside terms.

For project-led sectors such as construction, cash often slows because paperwork is incomplete rather than because the customer refuses to pay. Applications, supporting schedules, and approval chains need tight discipline.

Reducing DIO without creating stockouts

Stock reduction only works when planning improves. Blind cuts cause operational damage.

Practical measures include:

-

Review stock by movement, not just total value

-

Identify obsolete and slow-moving items before reordering

-

Align purchasing with realistic demand, not optimistic sales assumptions

-

Track work in progress separately so bottlenecks are visible

-

Challenge minimum order quantities where they distort cash use

Manufacturing and logistics businesses often benefit from tighter forecasting between operations and finance. If stock planning sits in one silo and cash forecasting in another, excess inventory becomes more likely.

A useful technical refresher on preparing a cash flow statement can also help teams connect stock, debtors, and creditors to the actual movement of cash rather than just month-end balances.

Extending DPO without hurting suppliers

Many businesses become too aggressive at this stage. Paying later can improve liquidity, but only if done deliberately and credibly.

What tends to work:

-

Negotiate terms before pressure hits

-

Prioritise strategic suppliers whose reliability matters most

-

Pay to agreed terms consistently once negotiated

-

Use staged payment schedules where supply cycles are complex

-

Take early-payment discounts only when the return is commercially sensible

What usually fails is stretching everyone indiscriminately. Suppliers notice fast. Once confidence drops, service levels often follow.

Sector-specific judgement matters

Working capital strategy should reflect the business model.

-

SaaS and tech firms should look carefully at billing frequency, annual prepayments, tax liabilities, and whether R&D tax claims are being handled in a way that supports cash timing.

-

Manufacturing businesses need tighter control over raw materials, work in progress, and purchase planning.

-

Construction firms should monitor applications, retentions, subcontractor terms, and contract billing discipline closely.

-

Logistics and distribution businesses need visibility over customer payment cycles, stock depth, and recurring operating commitments.

A stronger forecast ties all of this together. Directors who want a clearer planning framework can review how to build a great financial forecast to connect working capital decisions with hiring, tax, and funding requirements.

Strong working capital management is rarely about one dramatic fix. It is usually the result of better habits across invoicing, stock control, supplier terms, and forecasting.

Working Capital Management in Action A Worked Example

A simple example shows why the mechanics matter. Consider a fictional UK manufacturing company with £5 million turnover. Cash feels tight despite healthy sales growth.

Its management team reviews the cycle and makes three changes:

-

tighter credit control and faster invoice issue

-

better stock purchasing and reduction of slow-moving items

-

supplier term negotiation with key vendors

The effect can be shown clearly even without assigning an exact cash release figure.

| Metric | Before | After |

|---|---|---|

| DSO | High and inconsistent | Lower and more controlled |

| DIO | Excess stock and slow-moving lines | Leaner stock profile |

| DPO | Payments made too early on some accounts | Terms aligned to agreements |

| CCC | Longer cycle, more cash trapped | Shorter cycle, improved liquidity |

The commercial impact is usually immediate in feel, even if it takes time to stabilise fully. Management gets earlier visibility of overdue debt. Purchasing decisions become more disciplined. Supplier conversations become planned rather than apologetic.

What changed operationally

The finance function did not solve this alone.

-

Sales stopped agreeing loose terms without approval.

-

Operations reviewed stock ordering against actual demand.

-

Leadership set clear payment priorities for suppliers.

-

Weekly cash review meetings replaced ad hoc firefighting.

That is a key lesson from a worked example. Working capital improves when behaviours change across the business, not when finance reports worse numbers more neatly.

Establishing a Reporting Rhythm and Governance

Working capital management fails when nobody owns it between month ends. It needs a simple rhythm and clear accountability.

Who should own it

The finance lead should coordinate reporting, but ownership is shared:

-

Sales owns billing quality, terms discipline, and customer escalations

-

Operations owns stock levels, production flow, and purchasing signals

-

Procurement or leadership owns supplier terms and payment strategy

-

Finance owns reporting, challenge, and cash forecasting

A monthly review is the minimum. Many scaling businesses also need a shorter weekly cash meeting when pressure is high or growth is accelerating.

What a useful dashboard should show

A one-page dashboard is usually enough if it is current and discussed properly. It should include:

-

DSO, DIO, and DPO trends

-

Aged debtors

-

Key supplier exposures

-

Stock profile and slow-moving items

-

Near-term VAT, PAYE, and tax obligations

-

Short-term cash forecast

Teams that want stronger discipline around board reporting should also understand what are management accounts, because working capital control is far easier when reporting is timely, consistent, and commercially focused.

If a cash issue appears for the first time at month end, the reporting rhythm is too slow.

Frequently Asked Questions about Working Capital Management

What is working capital management in simple terms?

It is the day-to-day control of cash tied up in debtors, stock, and supplier payments. The purpose is to keep enough liquidity in the business to operate well and grow without unnecessary borrowing.

How can a business improve working capital quickly?

The fastest wins usually come from tighter invoicing, better collection discipline, and stopping avoidable early payments. Stock reviews can also release cash, but changes need to be handled carefully so service levels do not suffer.

Is invoice financing always a good idea?

Not always. According to guidance on the strategic importance of working capital management, 37% of £5 million to £15 million turnover firms face 45-day payment delays, so the issue is real. The same source says the right approach is selective financing, with fees kept below the cost of alternative debt.

How do R&D Tax Credits relate to working capital?

They can support liquidity if handled properly. The same source notes that 68% of qualifying UK tech start-ups mismanage claims, tying up capital despite the potential for a 33% cash uplift. For eligible businesses, tax planning should sit alongside cash planning, not apart from it.

What should management review first?

Start with the aged debtors report, stock profile, supplier terms, and a short-term cash forecast. That usually reveals whether the pressure comes from slow collections, excess stock, payment timing, or a combination of all three.

If cash feels tighter than profit suggests, it is usually time for a more disciplined working capital process. striveX Ltd helps UK businesses turning over £1 million to £15 million improve reporting, forecasting, tax planning, and finance control so cash supports growth rather than constrains it. To discuss the pressure points in the current cycle, book a conversation through the contact page or explore the relevant service pages for support with management reporting, forecasting, and tax strategy.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.