A target business lands on the desk at exactly the wrong moment. The strategic fit is obvious, the owner is open to a sale, and the numbers look promising. Then the main question arrives. Can the buyer finance the deal without choking cash flow six months later?

That is where most acquisitions become either disciplined growth or expensive distraction. Business acquisition financing is not just about finding a lender willing to say yes. It is about building a deal that works for the lender, the seller, and the buyer’s balance sheet after completion.

The market has opened a window for prepared buyers. In the UK, business acquisition financing in 2025 is seeing a cautious resurgence, with private equity-led activity projected to rise 16% in volume, while only 8% of large UK firms plan to increase debt for M&A, preferring cash reserves instead, according to BPM’s 2025 M&A outlook. That caution from larger corporates creates room for sharper SME buyers who can move with a clean, credible funding package.

A good transaction starts before heads of terms are agreed. Even the early paperwork matters. When a buyer is shaping the first approach to a target, a practical guide to drafting a letter of intent can help frame price, timing, exclusivity, and deal structure in a way that supports financing later rather than undermining it.

Setting the Stage for Your Acquisition

An acquisition usually begins with a commercial reason, not a financing one. A buyer wants a stronger regional footprint, a new service line, a customer base that would take years to build organically, or control over a fragile supply chain. Those are good reasons to buy. They are not, on their own, reasons a lender will support the deal.

The first discipline is to separate strategic logic from financial capacity. A target can be attractive and still be unaffordable. It can also be affordable and still be a poor deal if the structure leaves too little cash for integration, stock, payroll, VAT, or remedial spend after completion.

What strong buyers do early

Buyers who secure business acquisition financing efficiently tend to do three things before the market sees them as “ready”:

- Define the acquisition thesis clearly. Lenders and sellers respond better when the buyer can explain how the target fits the existing business in plain commercial language.

- Assess internal funding tolerance. The question is not whether debt is available. The question is how much repayment pressure the combined business can carry safely.

- Match the funding route to the deal type. Asset-heavy targets, recurring-income businesses, and owner-managed firms each call for different structures.

A lender is not funding ambition. A lender is funding repayment capacity, management credibility, and a transaction structure that holds together under pressure.

For owner-managed businesses turning over £1.5 million to £15 million, the opportunity is often in smaller, sensible acquisitions that larger buyers ignore. That can be an advantage. Sellers in this part of the market often care about continuity, staff retention, and deal certainty as much as headline price. Buyers who understand that can use structure to win.

Where deals usually go wrong

Weak acquisitions tend to fail long before a formal rejection. The warning signs show up earlier:

- Headline-price thinking. The buyer fixates on purchase price and ignores the cash needed after the deal completes.

- Overconfidence in synergies. Management assumes savings will appear quickly and without disruption.

- Poor sequencing. The buyer approaches lenders before the commercial rationale, deal terms, and forecasts are coherent.

Business acquisition financing works best when the buyer treats it as part of the acquisition strategy, not an admin step at the end.

Can You Afford It? The Pre-Deal Financial MOT

The quickest way to waste time in an acquisition is to ask what a lender might provide before working out what the business can sustain.

Look past the purchase price

A proper pre-deal financial MOT starts with total funding need, not just price. The buyer needs a joined-up view of:

- Purchase consideration. Cash at completion, deferred consideration, and any contingent payments.

- Transaction costs. Legal, financial, tax, and funding fees.

- Working capital. The cash required to run the combined business without immediate stress.

- Integration spend. Systems, people, reporting, and operational changes that have to happen early.

The next step is to normalise the target’s earnings. Owner-managed businesses often carry costs or benefits that will not continue after sale. A realistic normalised EBITDA strips out one-off items and owner-specific expenses so the buyer can judge the target’s underlying profit more accurately.

That matters because lenders underwrite cash generation, not aspiration. In sectors such as manufacturing and logistics, UK lenders typically value businesses at 4-6x EBITDA and expect to see a post-acquisition DSCR of at least 1.25x plus a current ratio above 1.5x, according to Smartroom’s guide to business acquisition financing.

Model lender reality, not management optimism

A finance model for acquisition funding should answer a blunt question. If the first year is harder than expected, can the business still pay its debts and keep trading comfortably?

That means stress testing. The model should not only show the base case. It should test slower collections, delayed synergies, margin pressure, and extra integration cost.

A strong forecast usually includes:

- Profit and loss assumptions that show what changes on day one and what changes later.

- Cash flow timing that reflects VAT, payroll, debt service, and seasonality.

- Balance sheet impact so management understands how the deal affects liquidity and headroom.

A buyer that cannot explain those points clearly is not ready to borrow for an acquisition.

For leadership teams that need a sharper forecast before speaking to lenders, this guide on how to build a great financial forecast is a useful starting point.

If the acquisition only works when everything goes right, it does not work.

The commercial aim of the pre-deal MOT is simple. It prevents management from overpaying, overborrowing, or underestimating the cash tied up in making the acquisition perform.

Your Financing Toolkit Debt, Equity, and Hybrid Models

There is no single best answer to business acquisition financing. The right answer depends on risk, sector, security, and how much flexibility the business needs after completion.

What each funding source is really for

Senior debt is usually the foundation. It is the cheapest layer in the structure, but it comes with scrutiny, covenants, and less tolerance for surprises. It suits deals where the target’s cash flow is understandable and asset backing is clear.

Equity does a different job. It absorbs risk and gives lenders comfort that the buyer has proper commitment to the deal. It is more expensive in ownership terms than debt, but it can protect cash flow in the early post-acquisition period.

Seller financing is often the missing piece in a sensible transaction. It reduces cash due at completion and keeps the seller commercially invested in a smooth handover. It also helps bridge valuation gaps where the buyer and seller disagree on certainty rather than headline value.

Hybrid structures are often the most practical route. A buyer may use senior debt for the core funding, equity for credibility and resilience, and deferred or seller-backed consideration to keep immediate cash outflow under control.

One underused route is government-backed lending. The Growth Guarantee Scheme offers 70-80% backed loans up to £2 million for acquisitions, yet only 8% of GGS approvals in Q1 2025 targeted acquisitions, according to the Milken Institute report covering the scheme. That does not mean it suits every deal. It does mean some buyers ignore a viable option too early.

A balanced discussion of the use of debt can also help leadership teams think more clearly about when borrowing supports growth and when it creates avoidable pressure.

Comparing Business Acquisition Financing Options

| Financing Type | Typical Source | Pros | Cons |

|---|---|---|---|

| Senior debt | Bank, challenger lender, government-backed lending route | Lower cost than equity, clear repayment structure, useful for stable cash-generative targets | Covenants, security requirements, less tolerance for underperformance |

| Equity | Existing shareholders, new investors | Strengthens balance sheet, improves lender confidence, reduces repayment strain | Dilutes ownership or consumes retained cash |

| Seller financing | Vendor note, deferred consideration | Reduces upfront cash need, aligns seller with transition, helpful in valuation gaps | Needs careful negotiation, seller may want strong protections |

| Hybrid structure | Blend of debt, equity, and seller support | Flexible, can match cash flow reality, often the most fundable approach | More complex documentation and negotiation |

The best funding stack is usually the one that leaves the buyer with room to operate, not the one that maximises borrowing capacity on paper.

A common mistake is to chase the highest possible debt level because it is available. That can leave the combined business technically funded but practically fragile. The more useful question is whether the structure gives management room to trade well, invest sensibly, and absorb disruption.

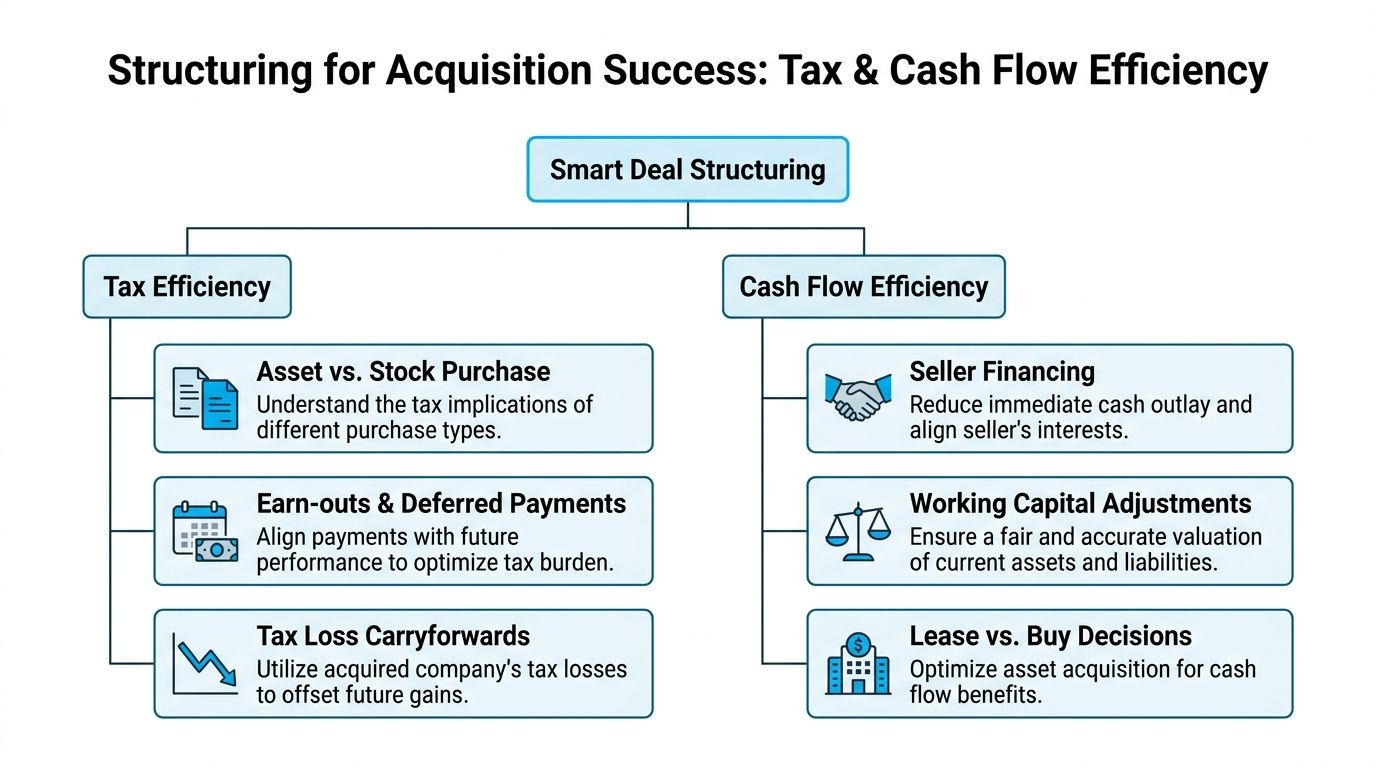

Structuring the Deal for Tax and Cash Flow Efficiency

The cheapest interest rate in the room can still produce the wrong deal. Smart buyers focus less on the loan headline and more on how the full structure affects tax, cash flow, and negotiation advantage.

A cheap loan can still be a bad structure

Deal structure determines who gets paid, when they get paid, how exposed the buyer is if performance slips, and how much cash remains in the business once the transaction completes.

That is why earn-outs, deferred consideration, and seller notes matter. They do different jobs.

An earn-out ties part of the consideration to future performance. That helps when the seller believes strongly in future upside but the buyer is wary of paying for growth that has not yet materialised.

Deferred consideration spreads cash outflow over time. It is less performance-sensitive than an earn-out, but it still eases day-one funding pressure.

Seller notes go further by turning part of the price into a financing layer. Commercially, that can be one of the strongest signals in a deal. A seller who is willing to leave money in often shows confidence in the numbers and in the transition plan.

Use the seller’s tax position intelligently

Seller psychology is usually discussed in soft terms. It should also be discussed in tax terms.

The extension of 100% Business Asset Disposal Relief incentivises sellers to accept seller notes because they can still benefit from the 10% CGT rate. Yet only 12% of UK SME acquisitions used seller financing in 2024, according to PGCOC’s guide to small business acquisition financing. That gap matters. It means many buyers are still negotiating as if every seller wants maximum cash on day one.

A better approach is to build proposals that answer both sides’ priorities:

- For the buyer: lower upfront equity, stronger cash retention, and less refinancing pressure.

- For the seller: a tax-aware structure, clearer timing of proceeds, and confidence that the buyer can complete.

- For the lender: a sensible capital stack with risk shared across parties.

Directors also need to think carefully about how acquisition funding interacts with shareholder balances and extraction planning. Understanding directors’ loans becomes relevant here, particularly when part of the funding mix involves shareholder support or temporary balance sheet movements before refinancing.

Good structuring does not just reduce the cost of capital. It reduces the chance that the buyer has to solve a cash crisis immediately after completion.

Tax efficiency should never drive the whole transaction. Commercial substance comes first. But where two deal structures produce the same strategic outcome, the one that preserves cash and improves tax treatment is usually the stronger answer.

Building a Lender-Ready Pack and Negotiating Terms

A lender-ready pack is not a bundle of documents. It is an argument. It tells a coherent story about why this target is worth buying, why this buyer can run it well, and why the debt can be repaid without heroic assumptions.

What goes into a lender-ready pack

Buyers who treat the pack as a strategic document usually make faster progress than those who dump information into a data room and hope for the best.

A credible pack normally includes:

- Historic financial information. Statutory Accounts, management figures, and evidence that the buyer understands the target’s quality of earnings.

- Integrated forecasts. Profit and loss, cash flow, and balance sheet, with assumptions that can be defended.

- Commercial rationale. Why this acquisition makes sense, how it will be integrated, and where the risks sit.

- Funding structure. Who is providing what, on what basis, and in what order.

- Management capability. Why the existing leadership can absorb the acquisition operationally.

The value of that preparation is not theoretical. SME deals with a thorough due diligence and loan package have a 70% financing success rate, compared with 45% for those without, and 32% of deals are derailed by overoptimistic cash flow forecasting due to underestimated integration costs, according to Clearly Acquired’s analysis of acquisition loan packages.

For teams that need tighter monthly visibility before approaching lenders, strong management accounts are often the missing ingredient. They help turn a loose narrative into a finance case that stands up to scrutiny.

Negotiate the terms that matter after completion

Borrowers often spend too much time on headline rate and too little on the terms that affect operational freedom.

Focus on issues such as:

- Covenant headroom. Tight covenants can create pressure even in a decent trading year.

- Repayment profile. Early capital repayment can strain a business that still has integration work to fund.

- Information requirements. Reporting obligations should be realistic for the finance team.

- Security package. Management should understand what is being pledged and what that means in practice.

A lender that offers slightly less borrowing with more workable terms can be the better partner. The objective is not to win the negotiation on paper. It is to protect the business during the messy part after completion, when systems, people, and cash flow are still settling.

Managing Due Diligence and Post-Acquisition Integration

Completion is not the end of the financing exercise. It is the point where every assumption starts meeting reality.

Due diligence is where weak deals get exposed

Due diligence should test the quality of earnings, customer concentration, working capital patterns, legal exposures, tax compliance, and operational dependency on the outgoing owner.

The buyer’s financing model needs to survive those findings. If diligence reveals margin weakness, overdue investment, or overstated stock value, the right response may be a reduced price, a revised structure, or a delayed completion. Forcing the original deal through usually stores up trouble.

The first 100 days decide whether the model was real

A successful integration starts with control. The combined business needs timely financial information, a common reporting timetable, and clear responsibility for cash management.

The early priorities are usually practical:

- Unify finance reporting. Management needs one version of the numbers quickly.

- Align cash controls. Supplier payments, debtor collection, payroll, and VAT cannot run on mixed disciplines for long.

- Clarify people decisions. Uncertainty around roles damages trading performance.

- Track synergy delivery carefully. Buyers should measure actual gains, not assumed gains.

The acquisition model is only useful if management can turn it into live reporting within the first few months.

Many deals underperform not because the purchase was wrong, but because post-deal governance was weak. Strong business acquisition financing gets the deal done. Strong integration makes it worthwhile.

FAQs on Business Acquisition Financing

How do lenders assess business acquisition financing in the UK?

They usually focus on affordability, management credibility, target quality, and deal structure. The buyer needs to show clear repayment capacity, realistic forecasts, and a coherent rationale for the acquisition.

Can seller financing help reduce the cash needed at completion?

Yes. Seller financing can lower the upfront equity required and improve cash flow immediately after completion. It also helps bridge valuation gaps when the buyer wants performance risk shared more fairly.

What financial metrics matter most before applying?

Cash flow matters most. Lenders also look closely at post-acquisition debt service capacity, liquidity, and whether the reported earnings are sustainable after normalisation.

Is debt or equity better for funding an acquisition?

Neither is automatically better. Debt is usually cheaper, but it adds repayment pressure. Equity is more flexible, but it costs ownership or consumes retained funds. Many sound deals use a blend of both.

What usually causes acquisition funding to fall over?

Poor preparation, weak due diligence, and unrealistic forecasting are common causes. Deals also fail when buyers focus on price and ignore working capital, integration cost, and covenant pressure.

If a leadership team is considering an acquisition and wants a commercially grounded view of what the business can afford, striveX Ltd can help build the forecast, pressure-test the deal structure, and prepare the financial case before lenders or sellers take a view. A focused conversation can clarify whether the deal is fundable, tax-efficient, and workable in practice. This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.