R&D tax credits for SMEs can still be a meaningful cash flow lever, but they no longer reward loose narratives and rough cost estimates. A Finance Director in a £1 million to £15 million turnover business balances product investment, margin pressure, headcount decisions, and Corporation Tax. In that setting, R&D relief works best when it is treated as part of financial strategy, not as an afterthought filed near the deadline.

The commercial tension is clear. In the 2023-24 tax year, SME claims fell 31% to 36,885 from 53,150, while total SME relief fell 29% to £3.15 billion. At the same time, average claim value rose 33% because smaller claims dropped away disproportionately, which points to a system that now favours better-evidenced claims from better-prepared businesses, according to this analysis of HMRC’s September 2025 statistics. For finance leaders, that is the key message. The opportunity is still there, but the weak process now costs more.

For businesses developing protectable innovation, it is worth understanding how R&D relief can sit beside R&D tax credits and Patent Box support.

For most scaling businesses, R&D tax relief is not a tax topic. It is a funding topic.

A company that is redesigning a production process, building a more capable software platform, or solving a stubborn technical problem is already committing cash before the commercial return is certain. Relief matters because it can return part of that spend to the business and improve choices around hiring, delivery, and reinvestment.

That matters more now because the easy claims have been pushed out of the system. The businesses still claiming successfully tend to be those with a clear technical story, disciplined project records, and finance teams that can connect costs to real development activity.

Why Finance Directors should care

A good claim does three things:

- Improves cash flow by turning qualifying spend into a tax credit or payable benefit.

- Supports planning because likely claim value can be built into forecasts rather than treated as a surprise.

- Reduces risk by forcing the business to document what happened, who worked on it, and why it was technically uncertain.

For a Finance Director, that last point is often overlooked. The same discipline that strengthens an R&D claim also sharpens project costing and investment review.

Key takeaway: The strongest R&D claims usually come from businesses that run good finance and project controls anyway.

Where SMEs often get stuck

The problem is rarely that a business has done no qualifying work. The problem is that the work was never framed properly.

In practice, SMEs often miss relief because they:

- Confuse innovation with eligibility. Commercially new does not always mean technically qualifying.

- Miss operational R&D. Factory process changes, product reformulation, software architecture work, and failed trials are often overlooked.

- Leave evidence too late. Rebuilding technical reasoning months after Year End usually produces a weak narrative.

- Treat the claim as compliance only. That approach tends to understate costs and overstate confidence.

The smarter approach is to treat R&D relief as a recurring finance process. If a business spends heavily on product, process, or platform development, the claim should be built from the same operating rhythm as budgeting and management reporting.

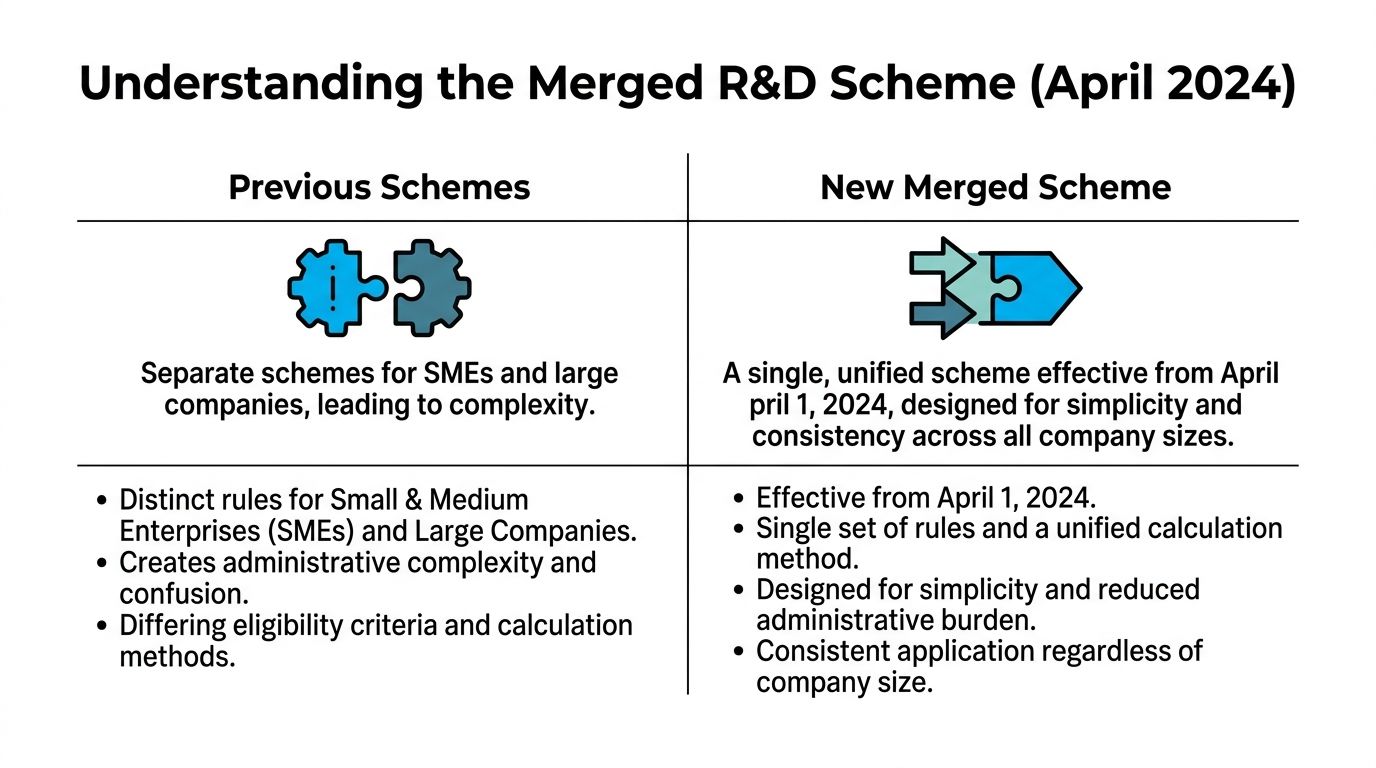

Understanding the Merged R&D Scheme from April 2024

The old system separated SME relief and the large company regime. For accounting periods beginning on or after 1 April 2024, most SMEs now claim under a merged scheme with a 20% taxable credit, while loss-making R&D-intensive SMEs spending at least 30% of total expenditure on R&D may qualify for ERIS, which offers a payable credit of up to 27%, according to this summary of the post-April 2024 SME position.

What changed in practice

The simplest way to think about the reform is this. The government moved from one set of rules for SMEs and another for larger businesses towards a more unified model, while preserving extra support for loss-making companies with high R&D intensity.

For finance teams, that creates a sharper decision process at Year End:

- identify qualifying expenditure accurately

- determine whether the company is profit-making or loss-making for tax purposes

- test whether R&D spend meets the intensity threshold for ERIS

- model the effect of a taxable credit versus a payable credit

That last step matters commercially. A taxable credit and a payable credit do not feel the same in a cash forecast, even if both are valuable.

The key commercial split

Most SMEs will now be looking at the merged scheme. That gives a clearer, more standardised route to relief, but it puts more emphasis on categorising costs correctly and understanding how the credit flows through the tax computation.

ERIS is different. It is built for loss-making companies where R&D is central to the business model rather than incidental. Software, product development, and deep process development businesses often need to test this position carefully because a small change in how expenditure is classified can affect whether the threshold is met.

A practical decision framework looks like this:

- If the company is profitable, the merged scheme is usually the starting point.

- If the company is loss-making, check whether qualifying R&D spend reaches the required share of total expenditure.

- If the business is close to the threshold, year-end forecasting and expense categorisation become important well before the accounts are finalised.

Practical point: The value in the post-2024 rules often comes from getting the classification work right during the year, not after the accounts are signed.

The businesses that handle this well usually involve finance early. They do not leave the technical team to describe projects in isolation from the numbers.

Qualifying Activities and Costs for Your R&D Claim

A common mistake is assuming qualifying R&D only happens in a lab. In reality, many valid claims come from commercial environments that look ordinary from the outside.

A manufacturer may be trying to achieve tighter tolerances, reduce failure rates, or adapt materials to a new production method. A construction business may be resolving buildability problems or integrating new systems under difficult site constraints. A software company may be tackling performance, scalability, data handling, or architecture issues that are not solved by buying standard software.

Businesses in sectors such as manufacturing often miss claims because the work feels like problem-solving rather than formal R&D. The label matters less than the substance. If the team is trying to overcome technical uncertainty and the answer was not readily available to a competent professional, the project is worth reviewing.

For teams developing AI-powered products, that distinction is especially important. Using AI tools off the shelf is not the same as resolving technical uncertainty in model behaviour, integration, performance, or deployment.

What qualifying work looks like

Good candidates for review often include:

- Manufacturing improvement work such as prototype iteration, tooling adjustments, material testing, and process redesign.

- Software development where internal teams are solving technical limits in architecture, integrations, speed, reliability, or scale.

- Construction and engineering projects where the challenge lies in delivering a technical outcome that cannot be achieved with standard methods.

Failed work can still qualify. If a trial did not produce the hoped-for result, that can support the technical narrative rather than weaken it.

Cost categories worth reviewing properly

Once the project qualifies, cost capture becomes the next challenge. Common categories include:

- Staffing costs tied to qualifying work, where payroll records and time allocation support the claim.

- Software and consumables used directly in development activity.

- Externally provided workers and subcontracted activity where the contractual and technical facts support inclusion.

- Computing costs linked to eligible activity.

What tends not to work is broad apportionment with little explanation. Finance teams get better outcomes when they can connect spend to named projects, named people, and specific development phases.

A short internal checklist helps:

- Project name and objective

- Technical uncertainty faced

- Who worked on it

- What evidence exists

- Which cost centres or ledger codes capture the spend

That level of discipline makes the claim easier to build and easier to defend.

How to Calculate Your R&D Tax Credit Claim

The commercial value of the new regime becomes clearer when the claim is modelled before submission. For an SME with £500,000 of qualifying R&D spend from April 2024, the claim could generate about £100,000 of taxable credit under the merged scheme or up to £135,000 as a payable credit if the company qualifies for ERIS, according to this summary of the new-scheme financial impact.

Worked example for a standard merged scheme claim

Consider a profitable manufacturing company with qualifying spend of £500,000.

The first calculation is straightforward.

| Line Item | Amount (£) |

|---|---|

| Qualifying R&D expenditure | 500,000 |

| Merged scheme credit rate | 20% |

| Taxable credit | 100,000 |

The commercial issue is not just the headline figure. The Finance Director needs to understand how that taxable credit feeds into the wider Corporation Tax position, the timing of the benefit, and whether any costs have been over- or under-allocated.

In a profitable business, the most frequent problem is understatement. Teams often exclude staff time that was clearly tied to qualifying development because nobody tracked it cleanly during the year.

Worked example for an ERIS claim

Now take a loss-making SaaS business with the same £500,000 of qualifying R&D spend, where the company meets the R&D intensity condition for ERIS.

The possible result changes materially.

- Qualifying R&D expenditure: £500,000

- ERIS payable credit rate: up to 27%

- Potential payable credit: up to £135,000

That difference affects more than the tax return. It can influence runway planning, recruitment timing, and how much external funding the business needs to bridge development cycles.

Commercial reality: For a loss-making scale-up, the difference between standard treatment and ERIS can alter funding conversations well before the claim is filed.

The discipline here is simple. Model both the accounting outcome and the tax outcome early. A Finance Director should not discover after Year End that the business was just below an intensity threshold because costs sat in the wrong buckets or projects were not scoped carefully enough.

The R&D Claim Process and Essential Documentation

Three weeks before the Corporation Tax return goes in, the Finance Director is usually staring at the same problem. The costs are in the ledger, the engineers remember the project differently, and nobody has pulled together a file that explains why the work qualifies if HMRC asks questions later.

That is the point where claim value and enquiry risk start to pull against each other. A business in the £1m to £15m range can often identify more qualifying spend than it first expected, but only if the technical story, cost allocation, and submission documents line up. Under the merged scheme, that discipline matters more because HMRC now expects a clear account of the projects and a clean link from narrative to numbers.

The practical process works best when it is run like year-end financial control, not a last-minute tax exercise. Technical leads should identify the projects that involved genuine scientific or technological uncertainty. Finance should then map those projects to qualifying staff costs, subcontractors, consumables, software, and any other eligible categories already discussed earlier in the article. The final step is to prepare the Corporation Tax treatment and the Additional Information Form so that the filing position is consistent from start to finish.

What a well-evidenced claim process looks like

The strongest claims usually follow a clear sequence:

- Start with project scoping. Define which projects qualify and where the uncertainty sat. Commercial importance is not enough on its own.

- Build the cost file from those projects. Pull payroll records, contractor invoices, software costs, and ledger support once the project list is settled.

- Draft the technical narrative with the people who did the work. Explain the problem, the attempted solutions, and why the outcome was not readily deducible by a competent professional.

- Reconcile before submission. The Additional Information Form, tax computation, and supporting schedules should all tell the same story.

The order matters.

Where finance teams start with the nominal ledger and try to justify the projects afterwards, the claim often becomes cost-led and harder to defend. HMRC can usually spot that quickly. The project descriptions become vague, time apportionments look rounded, and the technical explanation reads like product development marketing rather than evidence.

What documentation helps if HMRC reviews the claim

HMRC does not reward volume for its own sake. It wants evidence that the company identified the right projects, applied a reasonable method to the costs, and kept records close enough to the work to show the claim was prepared on more than hindsight.

Useful documentation often includes:

- Technical specifications and project briefs

- Design records, code logs, and version histories

- Test plans, test results, and defect records

- Project meeting notes and decision logs

- Timesheets, sprint records, or reasoned staff time allocations

- Evidence of failed attempts, rework, and abandoned approaches

- Payroll reports and ledger reconciliations that support the cost build-up

Failed work can help. It often shows that the answer was uncertain at the outset and that the team had to experiment, test, and revise before reaching an outcome.

From a Finance Director’s perspective, the documentation process is not just about defending a claim after filing. It improves forecasting as well. If the business captures qualifying activity during the year, it is easier to estimate the cash impact of the claim, avoid missed costs, and support board decisions on hiring, runway, and investment in further development.

The businesses that handle scrutiny best are usually not the ones with the longest reports. They are the ones with a disciplined audit trail, credible cost allocations, and technical records that match the tax position.

Common R&D Claim Errors and How to Avoid HMRC Enquiries

Most HMRC problems start with a bad assumption, not a bad intention.

The assumptions that usually cause trouble

The first is thinking that anything new for the business must qualify. It does not. A project can be commercially valuable and still be routine for tax purposes.

The second is claiming costs first and justifying the project later. That usually produces generic descriptions, broad percentages, and weak links between staff time and R&D activity.

The third is treating the Additional Information Form as a summary box rather than a risk document. If the project description is vague, the cost profile is inconsistent, or the narrative reads like marketing copy, the claim becomes harder to defend.

A better pre-submission review asks:

- Is this really technical uncertainty, or merely implementation work?

- Can the business show who did what and when?

- Do the numbers reconcile to payroll and ledgers?

- Does the narrative explain failed attempts and technical obstacles clearly?

Where leadership teams want extra protection from the cost of wider tax disputes, reviewing options such as investigation insurance can be sensible. It does not fix a weak claim, but it can help manage the financial disruption of enquiries more generally.

The strongest defence is still accuracy. Claims built on specific projects, traceable costs, and credible evidence tend to look exactly like what they are. Genuine claims.

How striveX Partners with Scale-Ups for R&D Claims

A Finance Director usually feels the pressure long before the claim is filed. Year-end is approaching, project teams are busy, the numbers need to reconcile, and nobody wants a promising relief claim to turn into an avoidable HMRC enquiry because the evidence was assembled too late.

That is the point at which specialist support changes the economics of the claim.

For businesses spending serious sums on product development, engineering, or technical improvement, the issue is rarely awareness. The issue is converting that spend into a claim that is technically credible, financially accurate, and efficient to prepare. In the post-2024 merged scheme era, that also means making better decisions during the year, not just producing a narrative after the event.

striveX works with scale-ups on that wider job, not only the submission itself.

The first part is claim selection. Some projects feel ground-breaking internally but fall outside the tax definition of R&D. Testing that boundary early helps finance teams avoid building forecasts around relief that may never materialise. It also helps direct documentation effort towards the projects that can support a claim.

The second part is cost discipline. Qualifying staff costs, externally provided workers, software, subcontracted activity, and consumables all need to tie back to the accounting records in a way HMRC can follow. For a £1m to £15m business, weak cost mapping often creates more risk than the technical argument. A credible claim starts with clean ledgers, sensible project coding, and a methodology that can be explained without hand-waving.

Then there is the technical narrative. Engineers tend to describe what was built. HMRC wants to understand the scientific or technological uncertainty, what attempts were made to resolve it, and why the outcome was not readily deducible by a competent professional. Translating that work into clear claim language is not a cosmetic exercise. It often determines whether a genuine project reads like qualifying R&D or routine delivery.

End-to-end handling matters too. That includes coordinating with technical leads, preparing the figures, aligning the corporation tax position with the Additional Information Form, and dealing with follow-up questions if they come. Done properly, the process reduces disruption for senior staff and gives the finance function a cleaner audit trail.

For Finance Directors, the commercial upside is broader than the claim value alone. Better project identification, tighter evidence capture, and earlier review of scheme position improve forecasting, reduce rework near submission, and lower the chance of expensive disputes later.

One option is striveX Ltd, which provides accounting, tax planning, and R&D claim support for growing UK businesses. The practical value is in helping leadership teams treat R&D relief as part of financial planning and control, rather than a one-off tax exercise assembled under deadline pressure.

R&D Tax Credit FAQs

How much can an SME claim for R&D tax credits?

It depends on the scheme and the company’s position. For accounting periods beginning on or after 1 April 2024, most SMEs claim under the merged scheme, while some loss-making R&D-intensive SMEs may qualify for ERIS. The result depends on qualifying spend, profitability, and whether the intensity test is met.

Do software companies qualify for R&D tax credits?

Yes, many do. The key issue is not whether the company writes software, but whether it faced technical uncertainty and tried to resolve it through development work. Routine implementation, configuration, or cosmetic upgrades are less likely to qualify than real technical problem-solving.

Can failed R&D projects still qualify?

Yes. Failure does not prevent a claim. In many cases, failed attempts help demonstrate that the technical solution was uncertain and required experimentation, testing, and iteration.

What records should an SME keep for an R&D claim?

The most useful records are project notes, technical specifications, design changes, test results, time records, payroll support, and evidence of failed attempts. The aim is to show what the problem was, who worked on it, what was tried, and how the costs tie back to that work.

Is the Additional Information Form mandatory?

Yes. It is a core part of the compliance process for R&D claims and should align with both the technical narrative and the financial calculations. Weak or inconsistent information in that form can make an otherwise valid claim harder to support.

A Finance Director who wants more certainty around r&d tax credits for SME’s should treat the claim as part of planning, not paperwork. striveX supports growing businesses with R&D claim preparation, tax planning, and practical finance processes that stand up to scrutiny. A short review can clarify whether projects qualify, which scheme may apply, and what documentation gaps need fixing before submission. This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.