A finance director reviews a customer contract that looks commercially sound, but the accounting treatment no longer feels straightforward. There is a set-up phase, a support element, a pricing clause that depends on delivery milestones, and a renewal option that sales expects to convert. Under the frs 102 changes, that contract may produce a very different profit profile from the one management has been used to seeing.

That matters because this is not just a Year End compliance issue. It affects when turnover is recognised, how profit lands in the accounts, what the board sees in monthly reporting, and how comfortably the business stays within banking or investor expectations. For companies in the £1 million to £15 million bracket, especially in technology, manufacturing, construction, and logistics, the impact is often operational before it is technical.

The revised rules apply for accounting periods beginning on or after 1 January 2026, with early adoption permitted. They introduce a more structured approach to revenue recognition under FRS 102, replacing older guidance that gave businesses more room to lean on broad principles around risks and rewards. A useful refresher on what Financial Reporting Standards are helps frame why this shift matters across reporting, governance, and decision-making.

Leadership teams that want to stay ahead of the change need more than a summary of the accounting language. They need to know which contracts create the biggest risk, where systems will struggle, how Corporation Tax planning may change, and how to explain altered profit timing without causing unnecessary concern. For further reading on practical finance leadership issues, the striveX knowledge centre is a useful place to explore related topics.

The Big Picture Shift From Risks and Rewards to Control

The core change is a shift in mindset. Under the older FRS 102 approach, many businesses focused on when the risks and rewards of a sale had passed. Under the revised model, the question becomes when the customer has obtained control of the promised good or service.

That sounds subtle. In practice, it changes how directors need to read contracts.

A straightforward stock sale is still likely to feel familiar. Goods are delivered, the customer takes control, and turnover is recognised at that point. The complexity starts where businesses bundle several promises into one deal, such as implementation, software access, support, maintenance, training, staged delivery, or bespoke production.

Why control changes the answer

Control asks a more precise commercial question. What exactly has the customer received, and when?

For a bespoke service delivered over time, turnover may need to follow the service pattern rather than the invoice date. For a package with several parts, one element may be recognised early while another is spread over the contract term. That is why the revised rules create more discipline around contract analysis.

Key takeaway: The accounting answer now follows the transfer of control for each promised good or service, not the overall commercial feel of the deal.

Why this is good for some businesses and awkward for others

There is a real upside. The revised model improves consistency and makes accounts easier to compare across businesses using UK GAAP. It also gives boards and investors a clearer view of what has been delivered to customers.

The trade-off is workload. Businesses with simple one-off sales may cope without much disruption. Businesses with subscriptions, milestones, project variations, service bundles, retention clauses, or long delivery cycles will need a more deliberate process.

The commercial mistake is to treat this as an accounting technicality. It is really a contract, systems, and reporting issue that lands in the accounts.

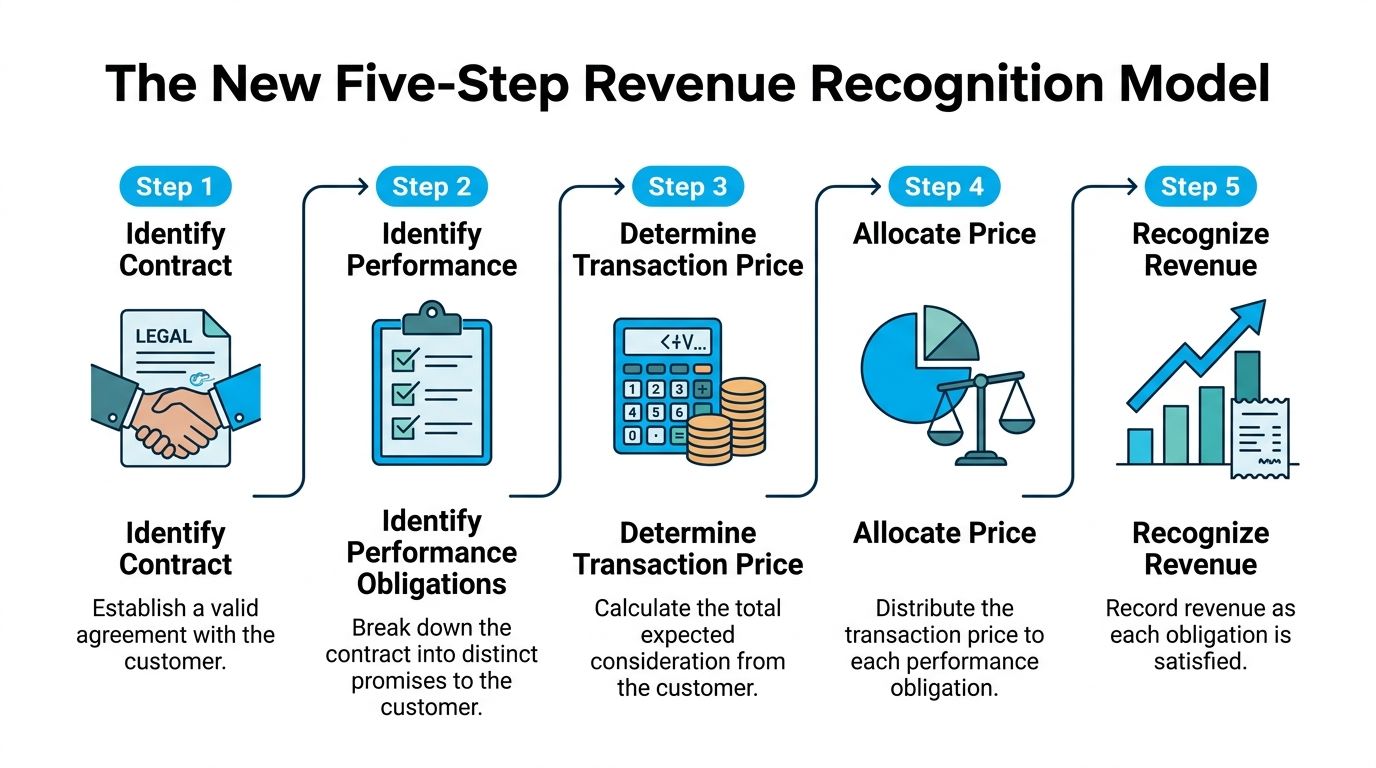

The New Five-Step Revenue Recognition Model Explained

A managing director signs what looks like a strong quarter. The contract is live, the invoice is out, cash is due. Finance then reviews the terms and finds the income cannot all be recognised at once because the deal includes setup, ongoing access, support, and training. That is the practical effect of the new model. It changes when turnover appears in the accounts, even if the commercial deal and cash profile stay the same.

The 2024 amendments to FRS 102 introduce a five-step revenue recognition model for accounting periods beginning on or after 1 January 2026. The Financial Reporting Council finalised the standards in early 2024, marking the biggest change to UK GAAP revenue recognition in many years. For leadership teams, the point is not academic. If your business is growing through bundled contracts, annual licences, project milestones, or custom production, you need a repeatable way to assess income before month end becomes a debate.

A useful companion read on wider UK revenue income reporting standards can help boards compare the logic across service-led businesses.

Step one and step two

Step one: Identify the contract with the customer

Start with the legal and commercial reality. There must be an agreement with enforceable rights and obligations, and it needs enough clarity for finance to assess what has been sold.

Ask: Do the terms make clear what each party must do, when payment is due, and what happens if scope changes?

For SMEs, optimism can sometimes creep in at this stage. Sales may agree side letters, email variations, or milestone wording that works commercially but leaves finance guessing at year end. If contracts are inconsistent, revenue recognition becomes inconsistent too.

Step two: Identify the separate performance obligations

This step usually drives the biggest change in timing. One contract can contain several distinct promises, and each one may need its own recognition pattern.

Ask: Which goods or services are separate, and which are so interlinked that they form one combined obligation?

Typical pressure points include:

-

Tech contracts: implementation, software access, support, upgrades, and training may not all be recognised on the same day.

-

Manufacturing contracts: design, tooling, staged production, delivery, installation, and warranty support may need separate assessment.

-

Project-based work: change requests, phase approvals, and customer acceptance terms can alter whether income is recognised over time or at completion.

The implications are not confined to finance. It affects how sales bundles offers, how operations document delivery, and how management explains monthly performance to the board.

Step three to step five

Step three: Determine the transaction price

Use the amount the business expects to receive under the contract terms. Fixed fees are straightforward. Variable amounts need judgement and discipline.

Ask: Does the deal include rebates, service credits, volume discounts, milestone payments, performance bonuses, or penalties that could change the final amount?

For a scaling SME, optimism can sometimes creep in at this stage. If the commercial team prices in stretch bonuses or uncertain usage fees, finance needs a policy for what can be recognised and when. That policy should be documented early, not argued over during the audit.

Step four: Allocate the transaction price to the performance obligations

Once the separate obligations are clear, the total contract value must be split between them on a basis that reflects their stand-alone selling prices.

Ask: If these elements were sold separately, what would each one reasonably be worth?

That allocation can be uncomfortable where pricing has been heavily negotiated. A software business may discount implementation to win a multi-year licence. A manufacturer may absorb design work into the overall contract price. The accounting still needs a defensible split, and your systems need to capture it.

Step five: Recognise turnover when or as each obligation is satisfied

The accounting result hits reported performance at this stage. Turnover is recognised when control transfers. In some cases that is a single point in time. In others it follows delivery over the contract period.

Ask: What evidence shows the customer has obtained control of each promised good or service?

Boards should expect more than a technical answer here. They should ask whether project records, delivery sign-offs, time data, and billing systems support the recognition pattern being used. If they do not, the year-end adjustment will arrive late and create noise in management reporting.

Practical tip: If finance, sales, and operations each describe the same contract differently, the five-step model will be applied inconsistently.

The businesses that handle this well usually do three things early. They review contract templates, tighten approval for non-standard terms, and check whether their accounting software can track multiple obligations within one customer agreement. For a growing business, that is the core commercial value of this model. Better numbers, fewer surprises, and clearer board reporting.

How Your Profit, EBITDA, and Balance Sheet Will Change

The revised model does not just alter disclosures. It can change the timing of reported performance, and that feeds directly into board decisions.

A contract that previously produced earlier turnover may now spread that turnover across later periods. Cash may arrive on the same timetable as before, but profit may not. That distinction matters for leadership teams who track performance through monthly packs, lender reporting, bonus schemes, and investor updates.

Where the commercial pressure shows up

Common consequences include:

-

Reported profit moves later: Businesses may invoice and collect cash early, but still recognise turnover over the delivery period.

-

EBITDA can shift: If turnover recognition changes, EBITDA may move even when the underlying deal economics have not.

-

The balance sheet changes shape: Deferred income and contract-related balances may become more prominent.

-

Banking conversations get harder: Covenants linked to EBITDA or other ratios may need review before the numbers move.

-

Remuneration plans can misfire: Bonus schemes based on profit or turnover may reward or penalise management unfairly if the basis is not updated.

-

Valuation narratives need care: If buyers or investors see lower short-term profit without understanding the accounting transition, they may draw the wrong conclusion.

This is why finance teams should model impacts before the first mandatory reporting period. Historical trends may no longer be directly comparable. Budgeting, forecasting, and board commentary need to be rebuilt around the new recognition pattern, not adjusted after the fact.

What strong finance teams do early

Good preparation usually includes a contract sample review, a bridge from old reporting to new reporting, and a plain-English explanation for non-finance stakeholders.

Board reporting works better when management shows both the statutory number and the commercial story behind the timing difference.

For businesses that rely on regular insight rather than Year End hindsight, strong management accounts support becomes especially important. The aim is not just compliance. It is preserving decision quality while accounting rules change underneath the numbers.

Worked Example A UK Tech Company Before and After

A simple worked example shows why these frs 102 changes catch growing businesses off guard.

Assume a UK software company with annual turnover of several million pounds sells an annual customer contract worth £120,000. The package includes an initial set-up service, access to the platform, and ongoing support.

Old thinking under the previous approach

Under the older approach, some businesses would have leaned heavily on the contract signature and invoicing event, particularly if the up-front work felt commercially significant.

That often led to a front-loaded result. A substantial part of the contract value might have been recognised early, with the remaining support element recognised over the year.

A simplified view might have looked like this:

| Period | Old treatment view |

|---|---|

| Quarter one | Large share of turnover recognised after set-up and contract activation |

| Quarter two to four | Smaller monthly or quarterly amounts recognised for support |

This approach could flatter early-year profit, especially where implementation work was intense and invoicing happened up front.

New thinking under the revised model

Under the revised model, finance would need to identify the distinct performance obligations and decide when control transfers for each one.

A more disciplined analysis might split the contract into:

-

Set-up services

-

Platform access

-

Ongoing support

That does not automatically mean three equal accounting entries. It means each promise must be assessed on its own merits.

A simplified pattern may now look more like this:

| Period | Revised treatment view |

|---|---|

| Quarter one | Turnover recognised for any completed set-up work, plus the first slice of platform access and support |

| Quarter two | Additional turnover recognised as access and support continue |

| Quarter three | Additional turnover recognised as access and support continue |

| Quarter four | Final turnover recognised as the annual service period completes |

The commercial lesson is straightforward. The customer deal has not changed, and cash receipts may not have changed. The timing of profit can still move materially because the accounting now follows delivery in a more granular way.

Directors should test their largest bundled contracts now, not when the first draft accounts reveal an unexpected dip in EBITDA.

Navigating the Knock-On Effects Tax, Software, and Governance

A change in revenue timing rarely stays inside the finance team. For a growing manufacturer or software business, it can alter tax payments, expose weak processes in the finance system, and create awkward board conversations if the numbers move before the story does.

Corporation tax and cash planning

Later profit recognition can mean later taxable profit in some periods. That may ease short-term cash pressure, but it also changes quarterly forecasts, instalment expectations, and the assumptions directors use when setting budgets or approving hires.

The practical risk is complacency. If management still expects tax to follow historic trading patterns, the business can overcommit cash in one quarter and tighten spending unnecessarily in the next.

For companies already reviewing controls around filings and reporting, it makes sense to look at the wider HMRC requirements support available. The accounting policy, tax timetable, and cash forecast need to line up.

Deferred profit is still profit. The question is when it lands, and whether the business has planned for that shift.

Software and process changes

This is usually where scaling SMEs feel the strain first.

A spreadsheet can cope with a small number of straightforward contracts. It starts to break down when sales agreements include staged delivery, renewals, upgrades, service credits, or several promises within one deal. At that point, finance is not just posting journals. The team is rebuilding contract logic by hand every month, which is slow, expensive, and difficult to defend under audit.

ICAEW has reported that many mid-sized firms expect a meaningful increase in finance time for contract reviews and system changes as the revised rules take effect. For owner-managed businesses, that matters commercially. Extra month-end effort means slower reporting, more pressure on a lean finance team, and less time spent on margin analysis, stock control, pricing, or funding discussions.

Directors should ask four direct questions:

-

Can the current system track separate obligations inside one customer contract?

-

Can it deal with contract amendments without manual recalculation?

-

Can finance show a clear audit trail for judgement and allocation decisions?

-

Can monthly management accounts still go out on time?

If the answer is no to two or more, the business probably has a systems issue, not just an accounting issue.

Governance and board communication

Boards do not need a technical lecture on the standard. They need a clear explanation of what has changed in the numbers and what action follows.

For a business in the £1 million to £15 million turnover range, the pressure points are usually familiar. EBITDA may move. Bank covenant headroom may tighten. Earn-out targets, bonus schemes, and investor reporting may need to be recalibrated. None of that means trading has weakened, but someone has to explain that early and plainly.

A useful board paper should cover:

-

Which revenue streams are most affected

-

How reported profit compares under the old and revised approach

-

Whether banking metrics or shareholder expectations need resetting

-

What operational changes are required in sales, delivery, and finance

The strongest finance leaders translate the rule change into commercial language. They show whether this is a timing issue, a systems investment issue, or a wider governance issue. In many SMEs, it is all three.

Your FRS 102 Implementation Checklist

The deadline feels distant until it is not. A business with complex customer contracts should treat this as a project with ownership, milestones, and accountability.

A practical project plan

A workable checklist looks like this:

-

Catalogue revenue streams

List every major contract type, not just the biggest customers. Subscription, project, maintenance, support, milestone, and bundled deals often need different treatment.

-

Flag complex contracts early

Focus on agreements with several deliverables, variable pricing, staged delivery, or modifications. Those usually create the biggest timing changes.

-

Model the accounting effect

Take a sample of representative contracts and compare old recognition with the revised model. This helps quantify where the board needs early warning.

-

Review systems and data quality

Check whether the existing finance process captures enough detail to support performance obligations, allocations, and timing decisions.

-

Plan process changes

Contract review should not start after invoicing. Finance, sales, and operations need a shared handoff point.

-

Train the people who shape contracts

Sales teams, commercial managers, and finance staff all influence the accounting outcome. Training should focus on practical contract features, not only technical wording.

-

Discuss transition with external advisers

Auditors and accountants should be involved before the first mandatory reporting cycle. Late technical debates usually create rework.

Practical tip: The best transition plans start with real contracts, not abstract policy documents.

A short monthly project review between now and the first affected accounting period will usually deliver better results than a rushed technical exercise near Year End.

FAQs on the FRS 102 Amendments

Does FRS 102 apply to small UK companies

It can. FRS 102 is the main UK financial reporting standard for non-IFRS entities, although some very small entities may use a different framework. The practical question is not size alone. It is which reporting framework the company currently uses and whether its contracts make revenue recognition more complex.

Can a business adopt the FRS 102 changes early

Yes. Early adoption is permitted. That said, early adoption is rarely sensible unless the business has a clear reason, the systems are ready, and the impact has been modelled properly. Adopting early without process readiness can create reporting noise rather than clarity.

Which businesses are most affected by the new revenue rules

Businesses with bundled offers, subscriptions, long-term projects, implementation phases, support arrangements, or variable pricing usually feel the biggest effect. That includes many companies in technology, construction, manufacturing, and logistics.

Will the changes affect company valuation

Potentially, yes. If reported profit or EBITDA moves because of timing changes, buyers and investors may need help understanding the bridge between old and new reporting. The underlying economics of the business may be unchanged, but the presentation of performance may differ.

Do these changes affect cash flow

Not automatically. The accounting treatment for turnover can change even when customer billing and cash receipts stay the same. That is why businesses should separate three questions: when cash arrives, when turnover is recognised, and when tax is paid.

If your business is reviewing complex contracts ahead of the 2026 changes, striveX can help map the accounting impact, pressure-test your reporting, and turn the technical rules into clear board-level actions. For scaling companies that need commercially sharp support, the next step is a focused conversation through the contact options on the site.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.