If a finance team wants to know how to reduce corporation tax UK, the uncomfortable starting point is this. A large share of smaller companies still aren’t using the reliefs already available to them.

According to HMRC, the UK Corporation Tax gap reached 15.8% of theoretical liability in 2023-24, equating to £18.6 billion, and for small businesses the gap was 40.1% or £14.7 billion in HMRC’s corporation tax gap data. In practice, that usually doesn’t mean deliberate non-compliance. It means missed claims, poor timing, weak documentation, and directors taking money out of the business in the wrong way.

For companies turning over £1 million to £15 million, Corporation Tax planning isn’t a once-a-year compliance task. It’s a cash flow tool. Done properly, it helps fund equipment, protect margins, reward directors, and support recruitment without creating problems with HMRC later.

Why Your Business Is Likely Overpaying Corporation Tax

The HMRC numbers matter because they reframe the issue. Overpaying Corporation Tax usually isn’t caused by one dramatic mistake. It’s caused by a series of ordinary decisions that never get reviewed.

A company buys assets but doesn’t map them correctly for allowances. Directors take remuneration in a way that suits payroll convenience rather than tax efficiency. A development project gets treated as routine operating spend instead of innovation work. A group grows informally, but no one tidies up the structure to use losses properly.

That’s why a year-end tidy-up rarely fixes everything. The businesses that reduce tax effectively usually make tax decisions at the same time as commercial decisions.

Where overpayment usually happens

- Expenses are recorded poorly: The tax deduction may exist, but weak bookkeeping means it isn’t claimed cleanly. A practical resource on what should and shouldn’t sit in the accounts is Booksmate’s expense guide.

- Capital spend is treated too casually: Asset purchases affect tax timing as much as operations.

- Founder extraction is too simplistic: Many owner-managed businesses default to salary or ad hoc dividends without a joined-up remuneration plan.

- Growth creates structural drag: Separate entities appear over time, but reliefs aren’t coordinated across them.

Commercial view: The tax bill is usually settled after the profit has already been earned. Planning earlier gives management more control over cash.

For businesses that want a proper review rather than a checklist, a focused tax efficiency review is often the point where missed reliefs become visible.

Maximising Your Capital Allowances on Business Assets

HMRC data shows capital allowances remain one of the most commonly missed or underused corporation tax reliefs. For companies in the £1m to £15m turnover range, that usually means the tax problem is not a lack of spend. It is poor classification, poor timing, or a finance team that records the invoice without asking how the asset should be claimed.

For a growing business, capital allowances are often one of the fastest ways to improve post-tax cash flow. You are already buying equipment, fixtures, tools, machinery, IT hardware, or fitting out premises. The commercial question is how much relief you can claim, and how quickly.

Timing matters because tax relief claimed earlier leaves more cash in the business. That cash can fund stock, recruitment, marketing, or debt reduction instead of sitting with HMRC until later periods.

A simple example makes the point. If your company buys a £20,000 asset that only qualifies for writing down allowances at 18%, the first-year deduction is £3,600. If the company is paying corporation tax at the main rate, that produces a tax saving of £900 for that year. The balance is relieved gradually over future periods. For an SME making several similar purchases in a year, the cash flow difference becomes material.

That is why asset planning should sit inside budgeting, not outside it.

In practice, I see four recurring issues:

- Assets are posted to the wrong category: The accounting entry may be broadly right, but the tax treatment is too simplistic.

- Projects with mixed costs are not split properly: A fit-out can contain items with different tax outcomes, and treating the whole project as one line item often understates relief.

- The fixed asset register is incomplete: Small tools, equipment, or later-stage additions get missed.

- Directors focus on cost, not after-tax cost: The purchase decision gets made commercially, but no one checks the actual net cost after relief.

The trade-off is straightforward. Claiming relief quickly improves cash flow, but only if the analysis is defensible. Aggressive treatment on weak records creates enquiry risk and management time later. Good planning gets both right. Faster relief, with evidence to support it.

A sensible review looks at:

- purchases already made in the current year

- expenditure likely before the year end

- whether items qualify for immediate relief or writing down allowances

- whether building, plant, and integral features need separating

- whether there are older assets or past projects where claims were understated

This matters most for businesses opening sites, upgrading production capacity, investing in warehousing, or scaling operations after a strong trading period. In those cases, allowances are not a technical side issue. They affect the actual cost of expansion.

If your business is investing regularly, specialist advice on capital allowances and related tax treatment can help you claim the right relief at the right time, without creating avoidable risk.

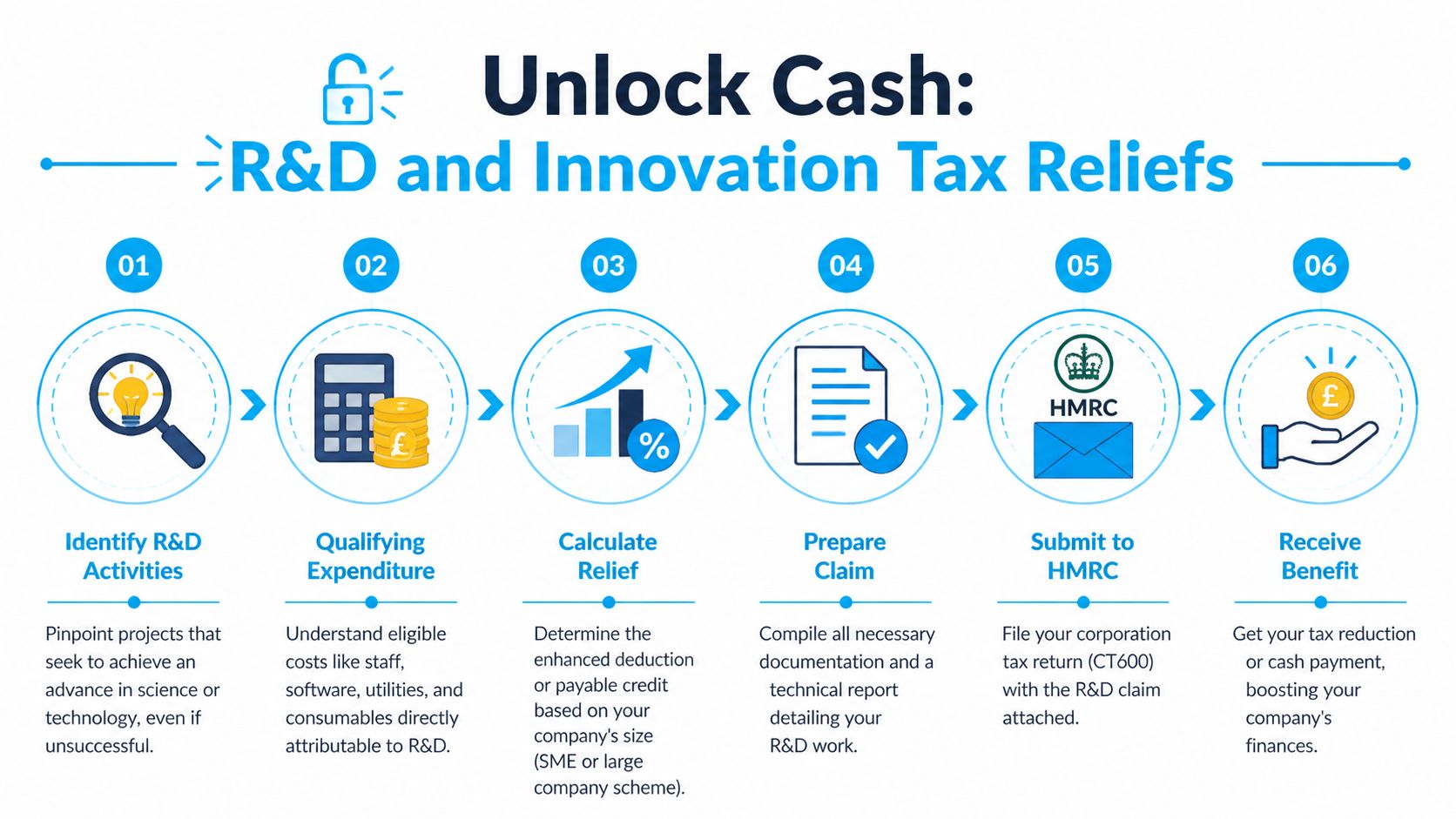

Unlocking Cash from R&D and Innovation Reliefs

A large share of eligible SME claims never get made, and for companies in the £1m to £15m turnover range that usually means one thing. Corporation tax is higher than it needs to be because innovation work is being treated as ordinary overhead.

The commercial point is simple. If your team has spent money solving technical problems, you may be able to turn part of that cost into a tax saving or cash credit. That improves cash flow without changing pricing, headcount, or your sales plan.

I see businesses rule themselves out far too early because they use the wrong test. HMRC is not asking whether you wear the label of an “R&D business”. Instead, the question is whether your staff tried to resolve technical uncertainty, improve capability, or create something that competent professionals could not readily achieve at the outset.

That can apply across a wide spread of sectors. A manufacturer changing materials or tolerances may qualify. A SaaS company building new core functionality may qualify. A construction firm developing a method to deal with site constraints may qualify. A food business reformulating a product to solve stability or shelf-life issues may qualify.

What good claims look like in practice

Poor claims usually start from the accounts and work backwards. Good claims start with the projects.

Finance teams often describe commercial goals such as faster production, lower waste, or a new customer offer. HMRC wants the technical story behind those goals. What was uncertain, who worked on it, what attempts were made, and why the answer was not obvious at the start. If that evidence is thin, the claim becomes harder to defend, even where the underlying work was genuine.

For owner-managed businesses, the trade-off is particularly important. A rushed claim may produce a short-term tax benefit, but weak project records increase enquiry risk and pull senior staff into time-consuming follow-up later. A well-built claim takes more discipline, but it usually produces a cleaner result and gives the finance team confidence over the number.

A worked example for a growing company

Take a £5m turnover engineering business with taxable profits of £600,000 before any R&D claim. During the year it spent £180,000 on qualifying staff costs, consumables, and subcontracted development work linked to a production improvement project.

If that spend qualifies, the company may reduce the after-tax cost of the project materially. The exact outcome depends on which regime applies and how the expenditure is structured, but the commercial effect is clear. Part of the development cost comes back through the tax system, which improves project payback and leaves more cash available for stock, recruitment, or debt reduction.

That is why the decision should not be left until the accounts are nearly finalised. For businesses at this size, the better process is to identify candidate projects during the year, track staff time while memories are fresh, and separate routine implementation work from genuine technical problem-solving.

Projects that are commonly missed

- Software builds with real technical uncertainty. Core platform development, integrations, data architecture, or performance work that goes beyond routine coding.

- Manufacturing change projects. New materials, altered tolerances, throughput improvements, or attempts to reduce failure rates where the answer was not known in advance.

- Construction and engineering method development. Adapting build techniques, sequencing, or structural solutions to deal with difficult conditions.

- Internal systems innovation. Creating tools or processes where available methods could not solve the problem reliably.

Patent Box sits slightly further up the planning ladder. It tends to matter once your business has protected innovation and recurring profits linked to that IP. At that point, the question is no longer just whether development spend qualifies for relief. It is whether the value created should also feed into a longer-term tax strategy around patented products or processes. If that applies, review your position with advisers who handle both R&D tax claims and Patent Box planning.

One practical point for finance teams. The modelling matters. Forecasting the tax effect of different project outcomes, claim positions, and profit scenarios is much easier if your board packs and budget files are built properly. If your team is improving that process, mastering Excel AI financial modelling can help tighten analysis before year end.

The businesses that get the best result here are usually not the ones doing the most paperwork at the end. They are the ones that identify technical projects early, capture evidence as work happens, and assess the tax benefit in commercial terms. How much cash comes back, how quickly it arrives, and whether it justifies further investment in innovation.

Optimising Director Remuneration and Pensions

Most owner-managed businesses lose tax efficiency because remuneration gets handled in fragments. Payroll decides salary. Dividends get declared when cash allows. Pension contributions happen late, if at all. That approach is common, but it isn’t efficient.

The better approach is to treat salary, dividends, and employer pension contributions as one joined-up extraction strategy.

Why pensions are often the strongest lever

Verified guidance states that employer pension contributions are a fully deductible business expense. A £10,000 employer contribution reduces taxable profit by £10,000, saving £2,500 in Corporation Tax at the 25% rate, and also saves the company about £1,380 in employer National Insurance that would apply to an equivalent salary, based on the figures in this pension planning summary.

That’s why pensions are often described as a clean route for extracting value from a company. The company gets tax relief. There’s no employer NIC on the contribution. The director builds personal wealth in a tax-efficient wrapper.

A simple comparison

| Extraction method | Company deduction | Employer NIC exposure | Personal access |

|---|---|---|---|

| Salary or bonus | Usually deductible | Usually arises on salary | Immediate |

| Dividend | Paid from post-tax profits | No employer NIC | Immediate |

| Employer pension contribution | Deductible if structured correctly | No employer NIC on the contribution | Deferred until pension access rules allow |

The trade-off is obvious. Pensions are efficient, but the money isn’t immediately available in the same way as salary or dividends. For many directors, that means the right answer isn’t “all pension” or “all dividends”. It’s a planned mix.

What usually works in practice

- Keep salary purposeful: It should support wider remuneration planning, not just payroll administration.

- Use dividends carefully: They’re useful, but they don’t reduce Corporation Tax because they’re paid from profits after tax.

- Fund pensions before Year End where appropriate: Timing affects when the company gets relief.

- Document the rationale: Large or irregular pension contributions without context can create avoidable questions.

A finance lead modelling these trade-offs needs a clear forecast of profit, cash, and extraction timing. For teams building that view, resources on mastering Excel AI financial modelling can help structure better scenarios before decisions are signed off.

Don’t ignore EMI for key people

For some growth businesses, remuneration planning goes beyond founders. EMI share schemes can be a useful way to reward and retain senior staff without defaulting to higher cash salaries. They’re not appropriate for every company, and the qualification rules need careful handling, but they can sit well alongside a broader remuneration strategy.

One practical option in the market is striveX Ltd’s Corporate Tax Review and Annual Tax Planning service, which is designed to identify tax efficiencies and review Corporation Tax liabilities for UK companies. The value isn’t the label. It’s the process of joining payroll, dividends, pension funding, and wider tax planning into one decision.

Using Group Structures and Loss Relief for Scale

A single-company structure is often fine at the start. It becomes less efficient as a business diversifies, launches new ventures, ring-fences risk, or acquires separate trading activities.

At that point, structure stops being a legal housekeeping issue and becomes a tax and cash issue.

According to the verified data, 15% of companies with turnover between £1 million and £10 million utilise group relief effectively, compared with 45% of larger groups, based on this guidance discussing group relief usage. That gap says a lot. Smaller scaling groups often have the complexity of a group, but not the planning discipline of one.

Where group structures create value

A group can help when different activities need different risk profiles, management teams, or investment plans. A common example is a trading company sitting alongside a property entity, logistics arm, or development business.

The tax benefit comes when losses and profits are reviewed across the group rather than in isolation. If one entity is investing or loss-making while another is profitable, group relief may improve the overall position.

What directors get wrong

- They set up extra companies without a tax map: Structure follows instinct, not planning.

- They leave losses trapped: One company struggles while another pays full Corporation Tax.

- They mix activities badly: Risk management and tax efficiency both suffer.

- They wait too long to restructure: By the time profits and losses are visible, options are narrower.

A group structure should solve a commercial problem first. Tax relief is strongest when the structure also makes operational sense.

A useful decision test

A more complex structure is worth considering when the business has:

- distinct trading activities

- different risk profiles

- planned acquisitions or spin-outs

- founders who want cleaner ownership arrangements

- profit and loss patterns that don’t sit neatly in one company

This area needs careful handling because relief claims depend on facts, ownership, timing, and the way entities interact. It’s one of the few planning areas where a poor setup creates both tax waste and operational confusion. For directors dealing with multi-entity growth, speaking to a specialist such as the team behind Rachel Harris’s profile can help turn a messy structure into a usable one.

Frequently Asked Questions on Corporation Tax

Around a quarter of taxable profit can go to Corporation Tax once your profits move above the upper threshold. For owner-managed companies in the £1 million to £15 million turnover bracket, that is usually large enough to affect hiring plans, capital investment, and how much cash stays in the business.

How much Corporation Tax does a company pay in the UK?

Corporation Tax is charged on taxable profits, not turnover. The rate depends on profit levels and associated company rules, so two businesses with similar sales can face very different tax bills. As noted earlier in this guide, smaller profit levels may fall into the lower rate band, while larger profit levels can push the company into the main rate.

In practice, the question directors should ask is not only “what rate applies?” but “what profit figure am I being taxed on?” That is where planning pays. A company making £300,000 before tax that misses £40,000 of available deductions pays tax on money it did not need to leave exposed.

What is the best way to reduce Corporation Tax legally?

The best answer is usually the one that fits how your business makes money and where it needs cash next.

For most SME companies, the biggest savings come from getting the basics right early. That means claiming allowable costs in full, timing capital spend properly, structuring director pay with care, using employer pension contributions where they suit the cash position, and checking whether technical project work supports an R&D claim. The commercial test matters. A relief is only useful if it improves post-tax cash and still fits the wider plan for growth, dividends, borrowing, or an eventual exit.

A simple example shows the point. If your company expects a strong year and is already planning to buy qualifying equipment, bringing that purchase into the current period may reduce the current tax bill and preserve cash that would otherwise go to HMRC. If cash is tight, delaying spend just to chase relief can be the wrong move. Good planning weighs both sides.

Can dividends reduce Corporation Tax?

No. Dividends are paid out of post-tax profits, so they do not reduce the company’s taxable profit.

They still have a place in remuneration planning for shareholders, but they work very differently from salary, bonus, or employer pension contributions. For directors, the key decision is usually about the mix. Too much salary can create avoidable PAYE and National Insurance cost. Too much dividend extraction can weaken pension funding and may not suit a long-term wealth plan.

Do all businesses qualify for R&D relief?

No. Many growing companies either assume they qualify when they do not, or miss claims because they think R&D only applies to lab-based businesses.

The test lies in whether your team tried to achieve an advance in science or technology and had to resolve genuine technical uncertainty. In the £1 million to £15 million turnover range, I often see qualifying work in software development, manufacturing improvement, engineering, product redesign, and process automation. The quality of the evidence matters as much as the project itself. Weak descriptions and loose cost calculations turn a good claim into a risky one.

When should Corporation Tax planning happen?

Before the year end, while decisions can still be changed.

That is the point when you can still alter timing, adjust remuneration, make pension contributions, review capital spend, and tighten up evidence for relief claims. After the year closes, the job becomes more restrictive. At that stage, you are often limited to filing the position rather than improving it.

For companies growing quickly, I prefer to review this at least a few months before year end and then revisit the numbers once management accounts are clearer. That gives you room to act, not just report.

If your company is turning over £1 million to £15 million and wants a sharper view of how to reduce corporation tax UK without drifting into aggressive planning, book a consultation with striveX Ltd. A focused review can identify where cash is being lost through missed reliefs, weak remuneration planning, or an outdated structure. The advice should be clear, commercial, and tied to what your business is trying to achieve.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.