A finance director in a growing business rarely worries about tax filing mechanics until a rule change starts pulling at daily operations. That’s where Making Tax Digital 2026 sits. On paper, it looks like another HMRC compliance development. In practice, it reaches into bookkeeping routines, management reporting, software choices, and the pace at which finance teams need to close data.

For businesses turning over £1 million to £15 million, the immediate reaction is often, “We’re a limited company, so does this really matter?” Often, yes. Many owner-managed groups include directors with property income, trading side ventures, or wider self-employment arrangements. Some businesses also support founders whose personal tax position is closely tied to the wider finance function. If those individuals fall into scope, the pressure lands quickly on the business team that already manages year end delivery, cash flow reporting, payroll coordination, and tax records.

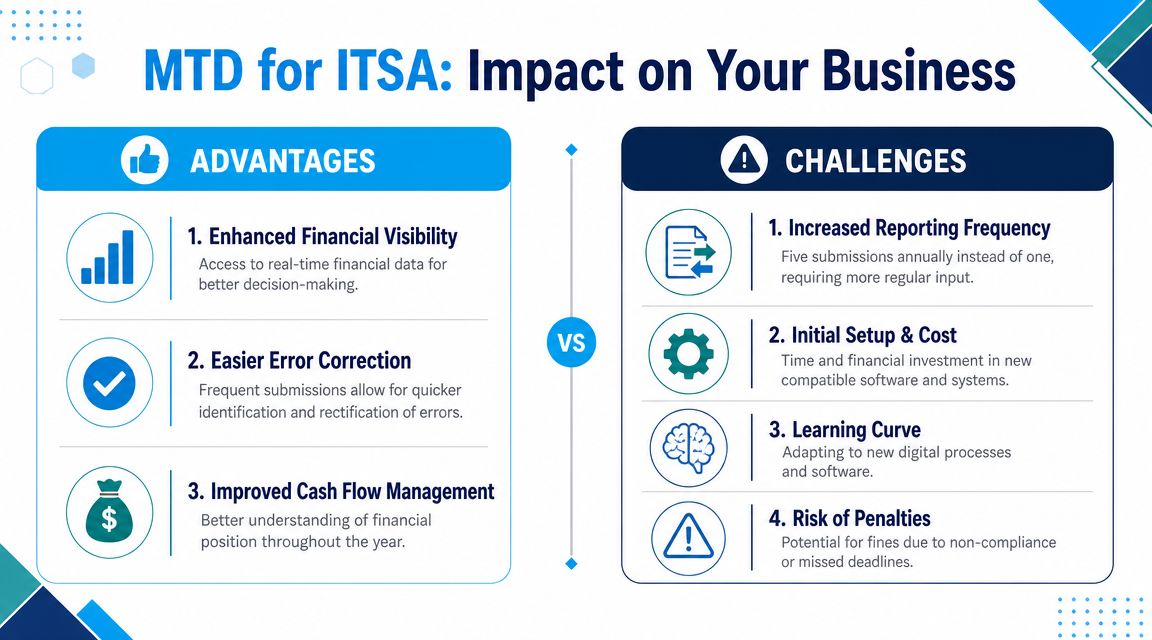

The commercial point is simple. This isn’t just about filing more often. It’s about whether the records behind those filings are clean, digital, and reviewable throughout the year. Businesses that leave that question until the deadline will end up paying in time, disruption, and avoidable stress. Businesses that treat it as an operating model change will usually come out with tighter controls and better visibility.

Introduction Making Tax Digital Arrives in 2026

A common 2026 problem will look like this. The company books are under control, but the founder’s rental income sits on spreadsheets, a side venture is tracked separately, and one person in finance pulls it all together at year end. That setup can survive an annual tax cycle. It becomes expensive once reporting has to be kept current through the year.

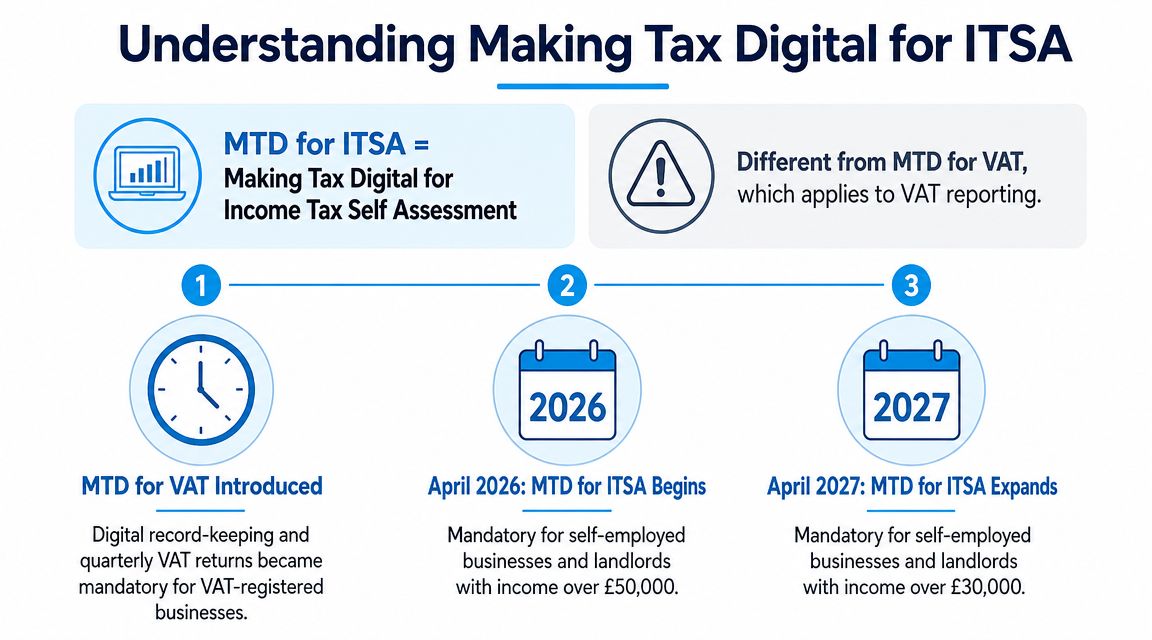

From 6 April 2026, sole traders and landlords with qualifying income above £50,000 are due to come within Making Tax Digital for Income Tax Self Assessment. For scaling businesses, the operational issue is rarely the tax return itself. The pressure falls on the finance function that already supports directors, shareholder matters, group entities, and property records.

This matters most in businesses turning over £1 million to £15 million because growth usually creates workarounds. Finance teams add entities, revenue lines, and reporting demands faster than they redesign process. Owner finances then sit just outside the main controls, often relying on manual exports, late adjustments, and inbox trails. Quarterly reporting exposes those weak points quickly.

The immediate question is not whether HMRC wants more submissions. It is whether the records behind those submissions are accurate, digital, and ready early enough to avoid repeated clean-up work.

If a director or related individual may be affected, now is the time to review income sources, record-keeping, and HMRC setup. In practice, that often starts with checking who is in scope, who owns each data stream, and whether support such as HMRC registration and tax account setup is already in place.

There is also a planning point that many businesses miss. HMRC has indicated that the regime is expected to widen after the first phase, with lower income thresholds planned from later tax years, although future dates should still be treated as subject to change until confirmed. The commercial response is straightforward. Fix the process once, at the right standard, rather than patching it for one individual and revisiting it a year later.

For a useful view of the early administrative pressure on affected individuals, see MTD ITSA sole trader first 30 days.

My advice is simple. Treat Making Tax Digital 2026 as a finance operating model issue with personal tax consequences, not as a narrow filing task. Businesses that act early usually get better visibility, clearer ownership, and fewer surprises once quarterly reporting begins.

What Is Making Tax Digital for ITSA

A director with a profitable trading company can still be caught by MTD for ITSA because the test sits at personal level. Rental income, sole trade income, or both can bring someone into scope even where the main business runs through a limited company. For scaling businesses, that is the first point to get clear, because the practical burden often lands on the same finance team.

MTD for ITSA means Making Tax Digital for Income Tax Self Assessment. It changes the way affected individuals keep tax records and report income to HMRC during the year. This is a wider process change than MTD for VAT, because it reaches into record-keeping discipline, timing, and year-end ownership rather than submission method alone.

From 6 April 2026, sole traders and landlords with qualifying income above £50,000 must join the regime. The threshold is then due to fall to £30,000 from 6 April 2027, as noted earlier.

The three moving parts

MTD for ITSA has three core requirements.

-

Digital records

Income and expenses must be kept in electronic form as the year progresses. Paper files and year-end reconstruction create risk because the records need to support regular submissions, not a single annual tidy-up. -

Quarterly updates

The taxpayer sends summary updates during the tax year through compatible software. Those submissions are not the final tax calculation, but they do rely on records being up to date and categorised properly. -

Final declaration

After the year end, the position is finalised with any adjustments, reliefs, and declarations still needed to complete the tax picture.

For owner-managed groups, the trade-off is straightforward. Leaving personal tax records outside the finance process may feel simpler now, but it usually creates duplicated effort later when quarterly deadlines start to drive earlier questions.

What qualifying income means

A common misunderstanding is treating the trigger as company turnover. It is not. The test is based on qualifying income, which broadly looks at relevant trading and property income of the individual.

That matters for growing businesses in the £1 million to £15 million range because the people affected are often founders, directors, or related parties whose personal income streams sit around the main business. The company may have a capable finance function and still be exposed if property records, side ventures, or HMRC account details are incomplete. Where those basics are not aligned, support with HMRC registration and tax account setup can remove avoidable delays.

For a practical counterpart from the individual side, this guide on MTD ITSA sole trader first 30 days is a useful reference.

The businesses that handle this well separate two decisions early. First, who is legally in scope. Second, who inside the business will own the records, reviews, and quarterly submission process once the rules apply.

Beyond Compliance The Real Impact on Your Business

A founder with a strong finance team can still get caught out here. The company books may be tidy, management accounts may land on time, and cash reporting may be sound, but if director property income, side trading activity, or personal record-keeping sit outside a controlled process, quarterly tax reporting starts pulling senior finance time into work that used to wait until year end.

For businesses in the £1 million to £15 million range, the commercial issue is capacity. More frequent reporting shortens the gap between transaction entry, review, correction, and submission. That exposes weak coding rules, slow reconciliations, informal owner record-keeping, and unclear responsibilities across the wider finance function.

Where growing businesses feel the pressure

The first strain usually appears in day-to-day operations, not in the submission itself.

-

Month-end discipline

Quarterly reporting depends on current books. If transactions are posted late, coded inconsistently, or left unresolved until year end, finance teams lose time fixing old periods instead of reviewing current performance. -

Records outside the main ledger

Founder and landlord income often sits in spreadsheets, emails, bank downloads, or adviser queries. That may feel manageable at low volume. It becomes disruptive once it needs a repeatable review cycle. -

Management oversight

Leadership teams need earlier visibility on what is incomplete, estimated, or awaiting evidence. Without that, quarter-end turns into a chase for missing information. -

Ownership of the process

Someone must own collection, review, sign-off, and document retention. Where responsibility is shared loosely between directors, bookkeepers, and advisers, deadlines become harder to control.

The upside is commercial if the business uses the change properly. Cleaner transaction capture and earlier review usually produce better management information, better cash planning, and fewer surprises around drawings, reserves, and funding decisions.

That benefit only shows up when the underlying process is reliable.

| Business condition | Likely operational effect |

|---|---|

| Records are current and coding rules are followed | Quarterly work is predictable and review time stays under control |

| Information sits across disconnected files and inboxes | Finance time is spent chasing support instead of analysing results |

| Owner income is tracked informally outside finance | Personal tax administration starts interrupting core business reporting |

| Reviews happen late in the cycle | Errors carry forward and become more expensive to correct |

In practice, this is why I advise scaling businesses to treat 2026 as a finance process project, not a tax filing project. The best outcomes come from tightening bookkeeping routines, setting approval points during the year, and using systems that give directors and advisers a clear view of what is ready and what is not. If the business already runs on Xero support and implementation for growing businesses, this is usually the right point to standardise workflows rather than add workarounds.

Some firms will manage this with existing accounting software and better controls. Others will need extra tools or specialist cloud based tax software solutions to handle quarterly submissions cleanly. The trade-off is straightforward. A lighter setup may cost less now, but a fragmented process usually costs more in director time, review effort, and avoidable correction work later.

Choosing MTD-Ready Software and Systems

Software decisions for MTD for ITSA should be made on process design, not on marketing claims. The legal requirement is broader than “buy something compatible”. HMRC’s model requires a digital audit trail, and compliant setups can include full accounting software, API-enabled spreadsheets, or bridging software that transmits spreadsheet data without re-typing. The key risk is whether records can be sent with a valid digital link and preserved electronically, as explained by ATT’s MTD for Income Tax guidance.

The three routes in plain English

Not every route suits a scaling business.

Full accounting software

This is usually the strongest option when the business already needs timely management information, multi-user access, and repeatable approval workflows.

It tends to work best where:

- Records are high volume and there are regular bank, purchase, and sales transactions

- Several people touch the data, including outsourced support or external advisers

- The business wants cleaner reporting, not just tax submission capability

The trade-off is implementation discipline. Poor setup, weak coding rules, and inconsistent user behaviour will still create bad outputs.

API-enabled spreadsheets

Some businesses prefer spreadsheets because key people know them well and specialist schedules already exist there. That can still be compliant if the spreadsheet setup is properly connected and preserved digitally.

This route can work where:

- Data volumes are manageable

- The finance lead has strong spreadsheet control

- The process is documented and reviewable

It tends to fail when spreadsheets become personal workarounds rather than controlled records. Hidden formulas, version confusion, and emailed copies are not a sound operating model.

Bridging software

Bridging software can be a sensible interim step when a business wants to retain an existing spreadsheet-led process but needs a compliant submission layer.

It may suit:

- Simple record structures

- Short-term transition periods

- Cases where replacing the wider finance system isn’t yet practical

What it doesn’t fix is poor bookkeeping. Bridging can connect records to HMRC. It can’t repair weak source data.

What works for a £1 million to £15 million business

For a scaling business, the question isn’t only whether the software can submit. It is whether the system supports control. Most businesses at this size benefit from reducing manual touchpoints and building finance routines around a central ledger.

A practical benchmark is whether the business can answer these questions quickly:

- Can source records be captured digitally at transaction level?

- Can the team trace a figure from entry to submission without re-keying?

- Can someone else step in if the usual finance lead is away?

- Can records be backed up and retrieved without hunting through inboxes?

For teams reviewing broader options and workflows, this overview of cloud based tax software solutions is a helpful reference point when mapping software capability against process requirements. Businesses already considering a more integrated setup may also want to explore Xero support and implementation as part of a wider finance modernisation plan.

Decision test: If the current system depends on one person remembering where the final numbers come from, it is not ready for quarterly digital tax reporting.

Navigating the New Penalties and Risks

A founder with profitable property income or side trading income can go from one annual tax pinch point to a repeating quarterly timetable very quickly. For a business in the £1 million to £15 million range, that rarely stays a personal admin issue. It pulls finance staff, advisers, and directors into a tighter reporting rhythm, especially where owner finances and business records overlap.

Under Making Tax Digital for ITSA, affected taxpayers will move to multiple submissions each tax year rather than one annual self assessment filing. HMRC’s published guidance indicates quarterly updates followed by an end-of-period process and final declaration, so the practical risk is frequency. Planned quarterly deadlines are expected to fall shortly after each quarter end, but businesses should check the final timetable and HMRC guidance at the point they set their reporting calendar.

Late filing risk becomes a control issue

Recurring deadlines expose weak routines. If bookkeeping runs behind, reconciliations are left until month end, or supporting records sit in inboxes until someone has time to sort them, the risk is no longer isolated to one filing. It repeats through the year.

For scaling businesses, the main cost is management distraction. A missed or rushed update can trigger more than a penalty point. It can force finance teams into rework, pull directors into avoidable review, and reduce confidence in the numbers being used for cash flow and tax planning.

The right response is operational, not just technical. Put clear ownership around each update cycle, fix internal cut-off dates before HMRC deadlines, and make sure review and approval sit with different people where the team structure allows. Businesses that tighten routines through automated bookkeeping and reporting processes usually reduce deadline pressure because the records are being maintained as part of the normal finance cycle.

Inaccuracy risk usually costs more than filing late

Late filing is visible. Poor accuracy is more expensive because it can run through several updates before anyone spots it.

A miscoding early in the year can carry forward into later submissions, distort tax estimates, and create correction work at the worst possible time. That matters for owner-managed groups where drawings, rental activity, mixed-use costs, or personal expenditure need careful separation. Quarterly reporting puts those judgement calls under more pressure, more often.

The businesses that handle this well treat quarterly submissions as a by-product of good records. They do not rely on year-end clean-up to repair weak transaction coding or missing evidence.

Filing on time helps. Filing from incomplete records creates a different problem.

There is also a planning point. HMRC has set out a phased approach to who comes into scope first, with lower income thresholds expected to follow after the initial wave. For firms and business owners near those thresholds, the sensible approach is to prepare earlier than strictly necessary. That gives time to test controls, clarify responsibilities, and avoid forcing the finance team into a compliance sprint once the rules apply.

Your Practical Readiness Checklist for 2026

A growing business can absorb a lot of inefficiency until reporting starts running to fixed quarterly deadlines. Then weak processes show up quickly. What looked manageable at year end becomes a recurring drain on the finance team, on directors’ time, and on confidence in the numbers.

For owner-managed businesses in the £1m to £15m turnover range, MTD readiness is not just a tax task. It is an operating model question. The businesses that cope well have clear ownership, consistent record-keeping, and a finance process that can produce usable figures during the year, not just after it.

A checklist worth using

-

Confirm who is in scope

Check whether any founder, director, shareholder, or connected individual has self-employment or property income that brings them within MTD for ITSA. For many businesses, the exposure sits with the people around the company rather than with the company itself. -

Map the record flow end to end

Follow one quarter of transactions from source document through bookkeeping, review, and submission. Any step that depends on rekeying, spreadsheet workarounds, or one person’s memory should be treated as a risk. -

Test whether the system works in practice

A software package can look suitable and still fail operationally. The key question is whether records are kept digitally, retained properly, and passed through the process without breaks that create rework or compliance risk. -

Tighten coding rules early

Quarterly reporting leaves less room for vague expense coding, uncleared balances, or mixed personal and business costs. If the chart of accounts is too loose, review time rises and tax estimates become less reliable. -

Set a quarterly close timetable

Put dates against bookkeeping cut-off, reconciliations, internal review, adviser input, and approval. Without that cadence, submissions become a deadline exercise instead of a controlled finance process. -

Train the people who do the work

The process needs to survive holidays, staff changes, and growth. If only one bookkeeper or one external adviser understands how the records turn into submissions, the business is exposed. -

Document recurring judgement areas

Mixed-use costs, property expenses, director-funded items, and year-end adjustments should be written down with agreed treatment. That reduces inconsistency from quarter to quarter and shortens review time.

This is also a good point to remove avoidable manual effort. Businesses reviewing their finance process can improve automated bookkeeping and reporting workflows before quarterly submissions start, which usually gives management better visibility as well as cleaner compliance.

FAQ

Does Making Tax Digital 2026 apply to limited companies

Not in the same way as MTD for ITSA applies to sole traders and landlords. The immediate issue for many limited company groups is whether directors or connected individuals have qualifying trading or property income personally.

Who has to use MTD for ITSA from 6 April 2026

Sole traders and landlords with qualifying income above £50,000 are due to come within MTD for ITSA from 6 April 2026. For affected business owners, the practical point is to check the position early rather than wait for HMRC contact.

How often do affected taxpayers file under MTD for ITSA

The reporting cycle changes from an annual filing pattern to quarterly updates during the year, followed by a final declaration. That means more frequent deadlines, more review points, and less tolerance for weak bookkeeping.

Can spreadsheets still be used for MTD for ITSA

Yes, if the process is compliant. Professional tax bodies and HMRC guidance have long recognised that spreadsheets can still form part of the process where records are kept electronically and submissions are made through compatible software with the required digital links.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.

If making tax digital 2026 is likely to affect a founder, director, landlord, or self-employed activity connected to the business, review the process now, while there is still time to fix ownership, systems, and reporting routines properly. striveX Ltd helps growing UK businesses build finance systems that are compliant, practical, and commercially useful. A focused readiness review shows who is in scope, where the weak points sit, and which changes will make the biggest difference first.