A lot of Finance Directors are in the same position right now. Payroll costs have climbed, hiring is still competitive, and every improvement to remuneration seems to land straight on the P&L.

That’s where Salary Sacrifice UK becomes commercially useful. Done properly, it isn’t a payroll gimmick. It’s a way to reshape part of remuneration so employees get value more efficiently and the business can reduce parts of its employment cost base at the same time.

For a growing company, the primary question isn’t whether salary sacrifice sounds clever in theory. It’s whether the savings justify the admin, whether payroll can run it cleanly, and whether the compliance risk is manageable. Those are the points that matter to a business turning over £1 million to £15 million.

The Commercial Case for Salary Sacrifice in a Growing Business

A typical scaling business often hits the same wall. Staff want better pensions, support with transport costs, or access to benefits that feel meaningful. Leadership wants to stay competitive without solely increasing gross salaries across the board.

Salary sacrifice can help because it changes the structure of remuneration, not just the size of it. Where it fits, the business can offer a stronger package without taking the full cost through payroll in the usual way.

Why finance leaders pay attention

The commercial attraction is straightforward:

- Lower employer NIC exposure: when part of cash salary is given up in exchange for an eligible benefit, the payroll cost can reduce.

- Stronger employee proposition: benefits can feel more valuable than the same amount delivered as taxed salary.

- Better reward design: the business can target benefits that support retention instead of defaulting to blunt pay rises.

A finance team should still be sceptical. A scheme that saves money on paper can become a nuisance if payroll corrections, contract errors, and staff confusion eat up the benefit.

Commercial test: salary sacrifice only earns its place if the employer saving is real, payroll can administer it consistently, and employees understand what they’re giving up.

For most SMEs, that means starting with the schemes that are easiest to explain and most likely to be valued by staff, then stress-testing the administration before rolling anything out widely.

A good way to approach it is as part of a broader review of remuneration and tax efficiency, not as an isolated HR project. That’s why many finance leaders fold it into a wider tax efficiency review for growing businesses, where the payroll impact, cash flow effect, and compliance process are looked at together.

When it usually works best

Salary sacrifice tends to work well when a business has:

- Stable payroll processes: monthly payroll discipline matters.

- A defined employee audience: not every benefit suits every team.

- Management appetite for process: contract changes and communications need proper handling.

It works less well when payroll is already messy, workforce churn is high, or leadership wants a quick saving without investing in setup. In practice, poor implementation usually causes more trouble than the concept itself.

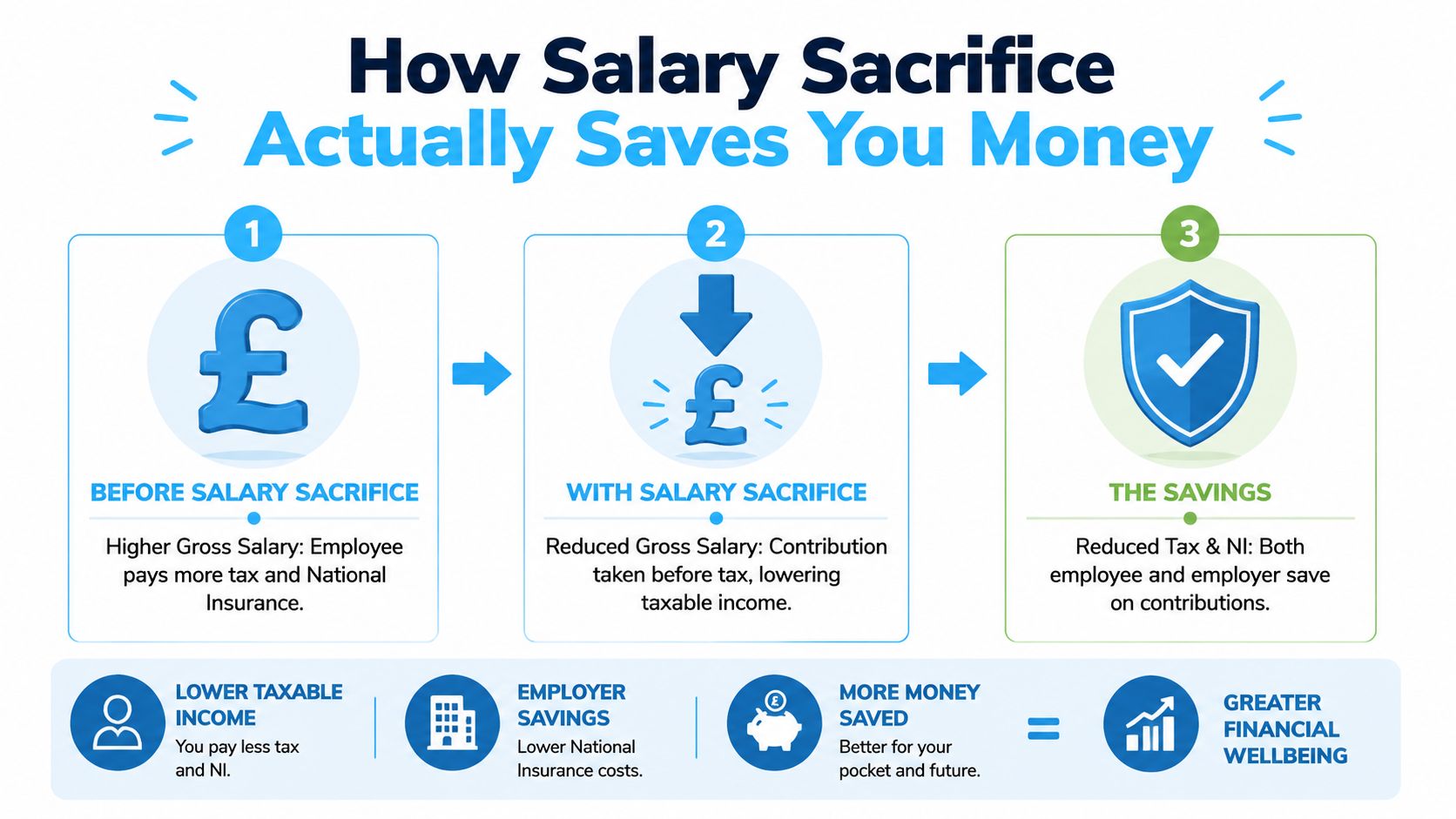

How Salary Sacrifice Actually Saves You Money

The central mechanism is simple. The employee agrees to give up part of cash salary, and the employer provides a non-cash benefit instead. Where the arrangement is valid, the sacrificed amount is excluded from Income Tax and National Insurance calculations, which lowers employee tax and NIC exposure and also reduces employer NIC. Travers Smith notes this employer NIC saving at 13.8% in its explanation of salary sacrifice arrangements, particularly in pension salary sacrifice where the employee’s taxable pay falls and the employer’s NIC bill also falls through the same change in gross pay structure, as outlined in Travers Smith’s salary sacrifice guidance.

What changes in payroll terms

The key distinction is this. Salary sacrifice reduces contractual cash salary before tax and NIC are calculated. That’s different from taking a deduction from net pay after payroll has already worked out tax and NIC.

For a Finance Director, the consequence is practical:

| Payroll treatment | Commercial effect |

|---|---|

| Post-tax deduction | usually helps the employee fund something, but doesn't create the same employer NIC efficiency |

| Valid salary sacrifice | can lower employer NIC because gross taxable pay is reduced before payroll calculations |

That difference is why finance teams should care about the design, not just the label.

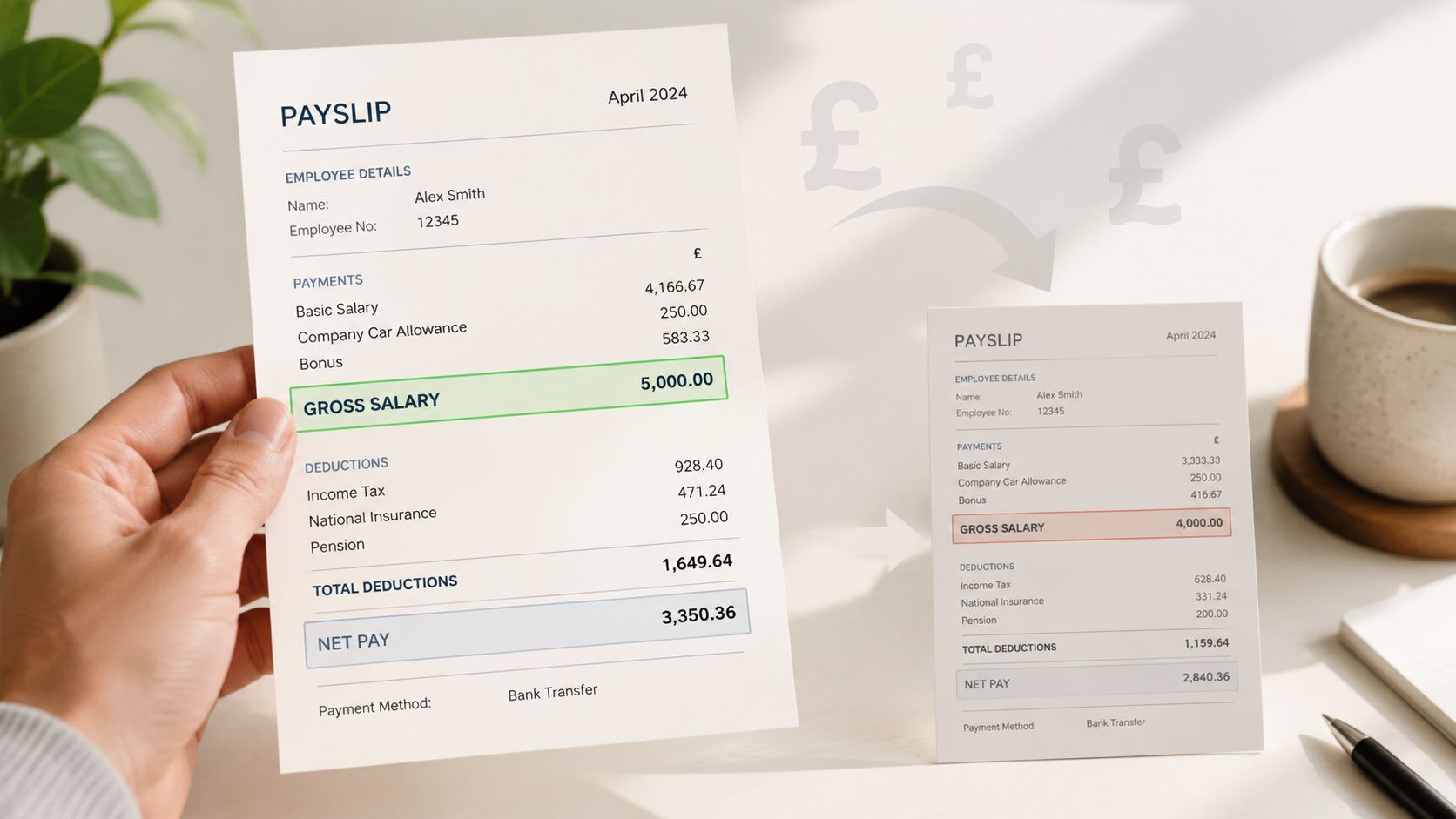

A simple example

Take an employee on £50,000 who agrees to sacrifice £3,000 into pension.

The contractual salary for payroll purposes becomes £47,000, and the £3,000 is provided through the salary sacrifice arrangement rather than taxed cash remuneration. Because that sacrificed amount sits outside the normal Income Tax and NIC calculation, both sides can save NIC compared with taking the same contribution after payroll.

For the employer, using the 13.8% NIC rate cited in the Travers Smith guidance above, the NIC saving on £3,000 would be £414.

For the employee, the exact saving depends on that employee's tax and NIC position. The important commercial point for the employer is simpler. The business has reduced part of the payroll burden without reducing the perceived value of total remuneration in the same way a straight salary cut would.

Payroll teams should model the saving employee by employee. The mechanism is consistent, but the employee impact isn't identical across the workforce.

Where the P&L benefit shows up

In practical terms, the benefit tends to appear in three places:

- Employer NIC savings: the most direct and measurable effect.

- Lower pressure for gross pay increases: some employees value the benefit structure more than a simple rise in taxable cash.

- Retention value: better-designed remuneration can support hiring and retention without fully loading cost into salary.

The strongest schemes are usually the ones with a clear employer saving and a clear employee benefit. If the business has to spend too much time explaining the value, adoption often weakens.

Businesses looking at wider payroll strategy often review this alongside tax planning and saving opportunities for owner-managed companies, because the right answer usually sits inside the full remuneration mix, not in isolation.

Popular Salary Sacrifice Schemes for UK SMEs

The most commercially relevant schemes for SMEs are usually pensions, electric vehicles, and lower-cost commuter-style benefits. They aren't equal. Some are easy to administer and broadly valued. Others look attractive in theory but create more operational friction than expected.

Pension salary sacrifice

For many SMEs, pensions are the cleanest place to start. Staff already understand workplace pension contributions, payroll teams are used to handling pension data, and the commercial logic is easy to explain.

There is, however, a policy change ahead. The 2025 Autumn Statement announced that from 6 April 2029, the National Insurance exemption for pension contributions made via salary sacrifice will be capped at £2,000. The Institute for Fiscal Studies reported that 18% of private-sector employees make salary sacrifice pension contributions above £2,000 a year, so private-sector employers are more exposed to that change, as set out in M&G's summary of salary sacrifice pension facts.

That doesn't make pension salary sacrifice a poor option now. It means finance teams should avoid treating the current position as permanent.

What tends to work

- Default enrolment with clear opt-in communication: simple messaging usually improves understanding.

- Sharing employer NIC savings intentionally: some employers use part of the saving to strengthen the pension offer.

- Regular payroll review: this matters more as future rule changes approach.

What tends not to work

- Over-engineered choices: too many employee options create admin drag.

- No communication on side effects: staff need to understand the effect on contractual cash salary.

- Ignoring 2029 planning: long-term remuneration design should already reflect the announced cap.

Electric vehicle arrangements

Electric vehicle salary sacrifice can be attractive because employees often understand the benefit immediately. It's visible, tangible, and easier to position in recruitment than a technical tax explanation.

From an FD perspective, the issue is less about popularity and more about operational fit. Vehicle arrangements can involve longer commitments, leavers, and policy decisions around damage, insurance, or early termination. A business should only proceed if those rules are nailed down before launch.

The best salary sacrifice schemes combine tax efficiency with something employees genuinely value. If either side is weak, uptake usually follows.

Cycle to Work and commuter-type benefits

Lower-cost schemes can still be worthwhile, especially where the workforce has broad commuting needs. They're not always transformational from a pure employer saving perspective, but they can improve the perceived quality of the package without creating a major fixed cost commitment.

For businesses reviewing options around commuting support and transport-related benefit design, this Benely guide for commuter benefits is a useful external reference point for thinking through how these benefits are positioned and communicated.

Which scheme usually wins for SMEs

A simple decision frame helps:

| Scheme type | Typical SME attraction | Main caution |

|---|---|---|

| Pensions | familiar, scalable, efficient | future NI cap from 6 April 2029 |

| Electric vehicles | highly visible employee value | policy complexity and leaver risk |

| Cycle to Work and similar | straightforward and accessible | smaller strategic impact |

For most companies, pensions remain the starting point because they're easier to integrate into payroll and easier to govern properly.

Compliance Guardrails and Contractual Rules

Many salary sacrifice arrangements often go wrong. The commercial upside disappears quickly if the structure is defective.

HMRC's position is clear. A salary sacrifice arrangement is a legally binding change to an employment contract. HMRC also requires that the arrangement must not reduce cash earnings below National Minimum Wage levels. If employees can move back to cash whenever they want, the tax and NI advantages are lost. HMRC further notes that, for new arrangements, the benefit is valued at the higher of the salary given up or the normal taxable benefit-in-kind amount, and exemptions on benefits in kind don't apply to salary sacrifice schemes, which is why the legal and payroll design has to be right from the start, as explained in HMRC's salary sacrifice and PAYE guidance.

The contract point is not paperwork theatre

A lot of employers underestimate this. Salary sacrifice isn't created by adding a note to a payslip or by getting an employee to tick a box in a portal without changing the underlying contractual position.

The arrangement has to reflect a genuine change to terms. That means documentation, timing, and payroll treatment all need to agree with each other.

The main guardrails finance teams should enforce

- Written contractual variation: the employee must agree to give up cash salary in exchange for a benefit.

- Timing before salary is earned: if the arrangement is implemented too late, the treatment can fail.

- National Minimum Wage protection: gross cash earnings after sacrifice can't drop below the permitted floor.

- Controlled change windows: if employees can flip between cash and benefit at will, the expected tax treatment doesn't hold.

Risk management rule: if payroll, HR, and contracts are all saying slightly different things, the scheme isn't ready.

Where businesses usually slip

The common failures are operational, not conceptual.

One is launching the scheme with poor documentation. Another is allowing too much flexibility because management wants the benefit to feel consumer-friendly. That instinct is understandable, but too much flexibility can undermine the tax treatment.

A third problem sits with payroll configuration. If the scheme is legally correct but the payroll run doesn't reflect the agreed reduction in contractual cash salary, the business can still end up with errors, employee complaints, and rework.

A practical control checklist

| Control area | What good looks like |

|---|---|

| Contracts | signed variation or valid contractual acceptance process |

| Payroll setup | sacrifice recorded correctly before tax and NIC calculations |

| NMW checks | employee-specific review before approval |

| Employee comms | clear explanation of impact on cash salary and other entitlements |

This is one reason salary sacrifice should sit inside wider payroll governance. Businesses already preparing for regulatory change often tie this work into broader Making Tax Digital planning for 2026 and beyond, because fragmented finance processes rarely stay contained.

The Hidden Impact on Statutory Payments and Employee Finances

The standard sales pitch around salary sacrifice often sounds too clean. It focuses on tax efficiency and ignores what happens when an employee's contractual cash salary is lower for other purposes.

That matters because some statutory entitlements and personal finance decisions rely on earnings measures that may be affected by the reduced salary figure.

Statutory payments can be affected

Where pay is reduced through salary sacrifice, that lower contractual figure can influence calculations linked to earnings. In practical terms, this can affect how employees think about:

- Statutory maternity arrangements

- Statutory paternity arrangements

- Statutory adoption arrangements

- Statutory sick pay considerations

The exact effect depends on the employee's circumstances and timing. That's why businesses shouldn't present salary sacrifice as a universal win with no downside.

Mortgage and borrowing conversations matter too

Lenders often look closely at basic salary and payslip evidence. An employee may still feel better off overall under salary sacrifice, but a lower stated salary can complicate a mortgage application or force extra explanation during underwriting.

That doesn't mean employees shouldn't join. It means they should do so with full visibility.

Some employees value immediate tax efficiency. Others care more about preserving a higher contractual salary for borrowing or family planning. A good scheme leaves room for informed choice.

What responsible employers do

The better approach is plain-English communication before enrolment. That usually includes:

- A summary of side effects: not just the headline savings.

- A reminder to seek personal advice where needed: especially before major borrowing decisions.

- A documented election process: so the employee's choice is clear and voluntary.

That level of transparency protects both the employer and the employee. It also reduces the risk of a benefit that looked efficient becoming a source of avoidable complaints later.

Salary Sacrifice FAQs

Is salary sacrifice worth the admin for a small or mid-sized company?

Usually, yes, if the scheme is focused and payroll is disciplined. The strongest commercial case is where the business gets a clear employer NIC saving and the benefit is easy for employees to value. It's less attractive when the process is overly bespoke or the payroll function is already under strain.

Can a company offer salary sacrifice to some employees and not others?

Yes, but it should be done on a clear and defensible basis. Eligibility rules should be documented, practical, and consistent with employment law and payroll constraints. Finance leaders should avoid informal arrangements that look selective without a commercial reason.

What happens if an employee leaves during a salary sacrifice arrangement?

The answer depends on the scheme rules, employment contract wording, and the nature of the benefit. This is especially important for benefits tied to longer commitments. Before launch, employers should define leaver treatment, payroll handling, and any recovery terms where appropriate.

Is pension salary sacrifice still worth doing before 2029?

For many employers, yes. The announced change applies from 6 April 2029 and relates to the National Insurance exemption above £2,000 for pension salary sacrifice contributions, rather than removing the wider structure altogether. For broader background written for another audience, businesses can also explore salary sacrifice with Umbrella Company.

Can employees change their mind whenever they want?

Not if the employer wants to preserve the expected tax and NI treatment. As covered earlier, unrestricted switching back to cash can undermine the arrangement. Employers should set defined rules for entry, change events, and review points, then make sure contracts and payroll follow those rules exactly.

If salary sacrifice could improve your remuneration design, reduce employer NIC, and tighten payroll efficiency, striveX Ltd can help assess whether it's worth implementing for your business. A focused review can cover scheme fit, contract process, payroll handling, and the likely commercial impact on your P&L. For growing companies, that usually starts with a practical conversation, not a theoretical one.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.