From 6 April 2025, a company may be exempt from a statutory audit if it meets at least two of these three tests: turnover of no more than £15 million, balance sheet total of no more than £7.5 million, and 50 or fewer employees. For many growing businesses, that means the UK audit threshold has shifted from being a routine compliance issue to a live strategic decision.

That matters because the headline change is large enough to alter the reporting position for a significant part of the market. Some businesses will be able to reduce compliance burden. Others will assume they’re exempt, only to discover that their group structure, subsidiary status, or filing position still pulls them back into audit territory.

For Finance Directors, MDs and CFOs in the £1 million to £15 million range, the key question isn’t just whether the rules changed. It’s whether the business can rely on the new position safely, and what that means for cost, banking conversations, internal controls, board reporting and Year End planning.

A Major Shift in UK Audit Requirements

The UK audit threshold change taking effect for financial years beginning on or after 6 April 2025 is one of the biggest audit threshold resets in recent years. According to guidance on the 2025 audit threshold changes, the uplift is expected to move around 113,000 companies and LLPs from small to micro status, with another 14,000 moving from medium to small and 6,000 from large to medium.

That scale changes the conversation. This isn’t just a technical adjustment for accountants. It affects budgeting, governance, reporting timetables and how leadership teams plan their finance function.

Why directors should care now

For owner-managed businesses and scaling SMEs, an audit can be both a burden and a benefit. It adds cost, management time and document pressure. But it can also support lender confidence, improve financial discipline and expose weak controls before they become expensive problems.

The risk sits in the gap between those two points.

A business might welcome the chance to step out of audit. But if directors make that call too quickly, they can end up with late surprises around group rules, subsidiary restrictions or filing conditions. Those issues usually emerge at the worst possible moment, during Year End close, investor due diligence, or a refinancing process.

Practical rule: treat the new threshold as a trigger for review, not an automatic green light to stop auditing.

Where the commercial opportunity sits

The opportunity is straightforward. If a business qualifies for exemption, it may be able to:

- Reduce compliance workload and free up internal finance time.

- Shorten the Year End process where the audit has been the main reporting bottleneck.

- Refocus spend on management reporting, forecasting and control improvements instead of purely statutory work.

What doesn’t work is making the decision on standalone turnover alone. That shortcut misses the point of how UK audit rules apply in real life, especially once a business has a holding company, multiple entities, or an overseas parent.

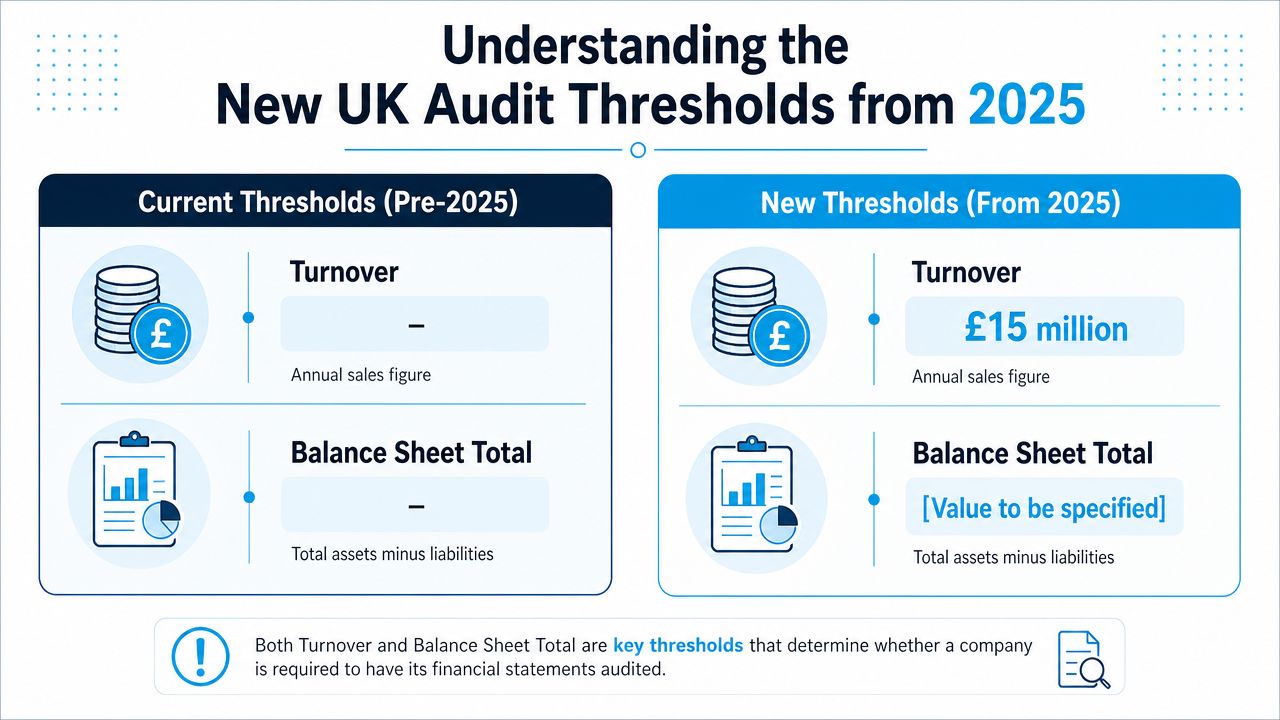

Understanding the New UK Audit Thresholds from 2025

From 6 April 2025, the UK small company turnover threshold for audit exemption rises by nearly 50 percent, from £10.2 million to £15 million. For many SMEs, that is the headline. For groups and UK subsidiaries of overseas parents, it is only the starting point.

For accounting periods beginning on or after 6 April 2025, a company is generally treated as small if it meets at least two of these three tests. Turnover of no more than £15 million, balance sheet total of no more than £7.5 million, and 50 or fewer employees. The updated limits are reflected in the government regulations on company size thresholds.

The new test at a glance

- Turnover test: no more than £15 million

- Balance sheet test: no more than £7.5 million

- Employee test: 50 or fewer employees

Meeting two out of three can be enough. A company can breach one limit and still fall within the small company size criteria.

That sounds straightforward. In practice, the edge cases matter more than the headline numbers.

How far the limits have changed

Before this change, the general thresholds were £10.2 million turnover, £5.1 million balance sheet total, and 50 employees, based on the previous small company limits in UK company law and related guidance from Companies House on company size thresholds.

A short comparison helps:

| Test | Pre-2025 position | From 6 April 2025 |

|---|---|---|

| Turnover | £10.2 million | £15 million |

| Balance sheet total / gross assets | £5.1 million | £7.5 million |

| Employees | 50 | 50 |

The employee cap has not changed. That is often where service businesses and labour-heavy subsidiaries get caught. Revenue may sit comfortably below the new threshold, but a growing headcount can still block the small company classification.

The point many directors miss

The numbers answer only one part of the audit question.

A standalone UK trading company with simple operations may be able to assess its position quickly. A company inside a group usually cannot. If there is a parent company, sister companies, cross-border ownership, or a UK subsidiary of an overseas group, directors need to check whether the size tests should be considered on an individual basis, a group basis, or both.

That matters because the commercial decision is rarely just “Can we avoid audit fees?” It is also whether dropping the audit creates friction with lenders, investors, minority shareholders, or the overseas parent reporting timetable. I often see UK subsidiaries assume the new threshold gives them a clear exemption route, only to find the wider group structure changes the result.

Turnover quality also matters. If revenue recognition is inconsistent, the threshold test can be wrong before anyone starts the exemption analysis. Better month-end discipline and software for accurate revenue reporting can help finance teams assess their position earlier, especially where deferred income, contract cut-off, or multi-entity reporting affects reported turnover.

The threshold review should also sit alongside wider reporting changes. Accounting policy choices, disclosures, and presentation can all affect how prepared a business is to step out of audit. It is more useful to review the position together with these FRS 102 changes for UK businesses than to treat audit exemption as a separate compliance exercise.

The SME Decision Checklist Do You Need an Audit

The most useful way to approach the UK audit threshold is as a decision process, not a single test. Directors usually get into trouble when they answer the wrong question. The question isn't just “Are we under £15 million turnover?” It's “Do we satisfy the full exemption position for this accounting period?”

A practical checklist for directors

Work through these points in order:

-

Check the period start date

The new limits only apply for financial years beginning on or after 6 April 2025. If the accounting period started before that date, the earlier thresholds may still apply. -

Test all three size criteria

Review turnover, balance sheet total and employee count together. Don't stop after checking one number. -

Apply the two-out-of-three rule properly

Passing two tests may be enough for size classification. Failing two means the company won't qualify as small on that basis. -

Check whether the company is in a category that still needs audit

Some entities remain outside the exemption route. That means size alone doesn't answer the question. -

Review group and subsidiary status

If the business is part of a group, the analysis becomes more complex. Entity-level figures can be misleading. -

Confirm the filing mechanics

Even where an exemption appears available, the company still needs to satisfy the relevant legal and filing conditions.

What tends to go wrong

In practice, the weak point is rarely the arithmetic. It's the assumptions around status.

Common mistakes include:

- Using draft figures too early and making a decision before final adjustments.

- Ignoring headcount because turnover gets all the attention.

- Treating subsidiaries as standalone companies when the wider group position matters.

- Assuming management accounts answer the question without checking statutory definitions and final Year End numbers.

For businesses that already produce comprehensive monthly reporting, the review is easier. But management accounts and statutory audit requirements aren't the same thing. The distinction matters, especially for boards that want clarity on what assurance they have from internal reporting. A helpful starting point is understanding whether management accounts are audited.

A business can be well run, well reported and still get the exemption decision wrong if the legal analysis is incomplete.

What works in practice

The best approach is to run the exemption review before the Year End is locked, not after. That gives the board time to decide whether it wants to rely on exemption, prepare for audit, or continue with voluntary assurance for commercial reasons.

What doesn't work is leaving the decision to the final accounts stage. By then, filing deadlines, board expectations and bank reporting often force a rushed answer.

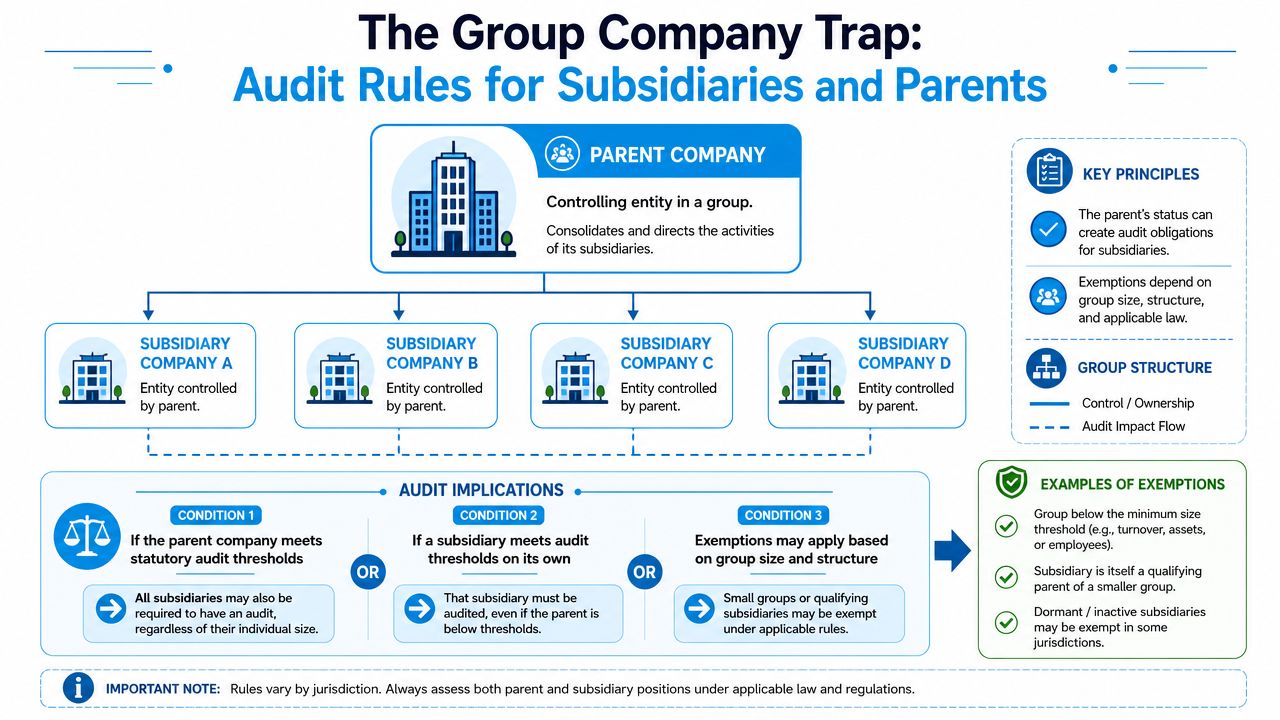

The Group Company Trap Audit Rules for Subsidiaries and Parents

Most summaries of the UK audit threshold become less helpful when addressing group companies. For group companies, the test isn't applied by looking solely at each entity in isolation. According to ACCA's guidance on determining group size for audit purposes, the UK audit test for groups is applied at the consolidated level, with turnover and balance sheet totals derived after consolidation adjustments.

Consolidation changes the answer

That matters because internal trading, intercompany balances and group structure can distort the picture if directors just add up entity accounts or rely on one company's standalone numbers.

The practical rule is this:

- Use consolidated figures, not just the subsidiary's own totals.

- Eliminate intercompany balances and revenue before comparing the group to the thresholds.

- Don't time-apportion assets and liabilities in consolidation, because ACCA's guidance specifically warns against that approach.

A subsidiary that looks comfortably below the threshold on its own can still lose the benefit of exemption if the wider group breaches the tests or the exemption mechanics aren't available.

Why overseas-parent groups get caught out

This issue comes up repeatedly where a UK company sits inside an international structure. The UK entity may be modest in size, but UK company law still looks closely at whether the subsidiary itself qualifies and how the broader group affects that answer.

GOV.UK states that for financial years beginning on or after 6 April 2025, a private limited company may qualify for audit exemption if it meets at least two of the three tests, but it also makes clear that certain entities must still be audited and that subsidiaries only qualify if they themselves meet exemption rules, as outlined in the government's audit exemption guidance for private limited companies.

Being below the headline threshold doesn't settle the issue for a subsidiary. Group status can override the simple reading.

The real trade-off for scaling groups

For fast-growing SMEs, the threshold uplift gives more room. It can delay the point at which a group falls into mandatory audit territory. That flexibility is useful for holding structures, founder-led groups and acquisition strategies.

But the room created by the new threshold also creates a planning trap. Directors may assume they can restructure freely or launch a new subsidiary without affecting audit exposure. In reality, every added entity increases the chance that the consolidated test, filing position or subsidiary mechanics need fresh review.

A sensible board treats this as part of corporate structure planning, not as a last-minute statutory accounts query.

Worked Examples in Practice

A small change in structure can move a business from audit-exempt to audit-required, even when turnover barely changes. That is why worked examples matter more than the headline threshold.

Standalone company nearing the threshold

A manufacturing company has grown quickly and expects turnover close to the new limit. Employee numbers are still below the threshold, and the balance sheet total also appears to sit within range.

The practical question is not just whether the company can claim exemption. Directors also need to ask whether they should. If lenders, investors, or a major customer rely on audited accounts, dropping the audit can save cost in one area and create friction in another. I often see businesses focus on the filing position and miss the commercial one.

The sensible approach is to finalise the statutory numbers first, then test the position using the year-end figures rather than management accounts alone. Late stock provisions, debtor recoverability issues, or accruals can change the outcome.

UK subsidiary of an overseas parent

Nonetheless, many guides stop too early.

A UK trading subsidiary may look comfortably below the small company thresholds on its own numbers. Management assumes the UK company is exempt, because the overseas parent is much larger and audited elsewhere.

That assumption can be expensive. The UK company still needs its own exemption analysis, and group relationships can affect the answer. In practice, I would check the ownership chain, whether group accounts are prepared, whether any guarantees or support arrangements are in place, and how the parent expects the UK entity to report. The legal test sits in UK company law, but the operational pressure often comes from overseas group reporting deadlines and audit expectations.

This is also where finance teams need a clear handle on UK company filing and compliance requirements. A technically correct conclusion reached too late can still create filing problems.

Small UK group with a simple holding company

A trading company sits under a UK holding company with one additional dormant or low-activity subsidiary. On first review, the trading entity looks small enough to avoid audit.

The board still needs to test the group position properly. Intercompany balances must be eliminated. Management charges, loans, and year-end adjustments can all affect the final numbers. A dormant company is not always harmless either. If it changes the group analysis, it still needs attention.

This is the point many owner-managed groups underestimate. Small on the face of the individual company accounts does not always mean small for the statutory group test.

Short accounting period and pro-rated turnover

Short periods are another area where mistakes happen. Turnover may need to be time apportioned for a period shorter than 12 months, which can change whether the threshold is met. Other measures are not automatically adjusted in the same way, so a quick spreadsheet check can give a false answer.

That matters most in first-year accounts, period-end changes, and reorganisations. Those are common in growing groups and in UK subsidiaries being aligned to an overseas parent's reporting timetable.

The safest route is to document the basis for the calculation early, before the accounts are nearly finished. Teams that automate financial reconciliations usually find these judgement points easier to support because the close process is cleaner and the audit trail is stronger.

My Company Needs an Audit What Happens Next

Once a company concludes that audit is required, the priority shifts from eligibility to execution. That part is manageable if the process is organised early.

The first steps

Most businesses need to get four things in place:

- An agreed timetable so the audit doesn't drift into filing season panic.

- A clean Year End close with reconciled balance sheet accounts and clear supporting papers.

- Named owners for key schedules such as fixed assets, debtors, creditors and payroll.

- Board alignment on what the audit is expected to deliver beyond legal compliance.

Where finance teams struggle, it's usually because the close process isn't ready for external scrutiny. Reconciliations are incomplete, documentation is scattered and judgement areas haven't been written down. Businesses that want to automate financial reconciliations often find that better month-end discipline makes the first statutory audit far less disruptive.

What the audit will test in practice

Auditors generally focus on whether the financial statements are properly supported and whether management can explain the numbers with evidence. That means the business should expect questions around revenue cut-off, accruals, debtor recoverability, stock where relevant, payroll, related parties and control processes.

A calm audit usually depends on preparation more than complexity.

A workable roadmap

A practical sequence looks like this:

- Confirm the requirement early and document the basis.

- Prepare statutory accounts support files rather than relying on ad hoc spreadsheets.

- Resolve technical accounting issues before fieldwork where possible.

- Keep Companies House deadlines visible so the audit timetable fits the filing window.

For many businesses, the sharpest early focus is on statutory compliance and filing responsibilities. A useful reference point is Companies House requirements, especially where directors are dealing with a first audit or a change in filing expectations.

FAQs on UK Audit Exemption

Do all companies under the new UK audit threshold automatically become audit exempt

No. Being under the size limits is only part of the answer. A company may still need an audit if it falls into a category that must be audited or if subsidiary and group exemption conditions aren't met.

Does the UK audit threshold apply differently to subsidiaries

Yes. Subsidiaries need their own exemption position reviewed carefully. GOV.UK makes clear that subsidiaries only qualify if they themselves meet the exemption rules, so the headline threshold alone doesn't settle the question.

Can a group structure force an audit even if one company is small

Yes. Group status can change the analysis because the test may need to be considered using consolidated figures rather than only the standalone company numbers. That's where many directors get caught out.

If audit exemption is available, should a business always stop auditing

Not necessarily. Some businesses still choose audit for lender confidence, shareholder comfort, board assurance or stronger internal controls. The legal answer and the commercial answer aren't always the same.

Does a short accounting period change the threshold test

It can affect turnover calculations. Historic guidance shows that turnover could be pro-rated for a short accounting period, which means non-standard Year Ends need extra care when assessing eligibility.

If the new UK audit threshold leaves any doubt about your group position, subsidiary status or next filing steps, striveX Ltd can help review the facts and turn them into a clear decision. For growing companies, that usually means cutting through the noise quickly, determining if an exemption applies, and making sure the reporting process supports the commercial plan. A focused conversation can save a great deal of last-minute disruption.

Meta title: UK Audit Threshold 2025 for Growing UK Businesses

Meta description: Understand the UK audit threshold from 2025, including group company traps and exemption risks, so you can plan compliance with confidence.

Disclaimer: This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.