A company finally puts a share incentive in place. The board expects it to help attract senior hires, retain key staff and align management with long-term value. Then the practical issue lands on the Finance Director’s desk. What exactly has to be reported, when, and how much of the required data exists in one place?

That’s where the employment related securities return stops being an admin task and becomes part of the control environment around pay, tax and governance. If the reporting process is weak, the scheme can still exist on paper, but the operational risk sits with the company. Errors, missing returns and poor records can undermine what was meant to be a smart incentive decision.

Recent HMRC changes show the direction of travel. HMRC simplified net settlement reporting in January 2026, but the wider message is that ERS compliance is moving away from simple form-filling and towards stronger data quality, payroll coordination and employee mobility tracking, as noted in Baker McKenzie’s 2025/26 ERS update. For growing businesses, that means a rushed June exercise usually isn’t enough.

Introduction Why Your ERS Return Is More Than Just Paperwork

Most leadership teams think about employee equity in commercial terms. They want to motivate the right people, protect cash flow and reward growth without overcommitting fixed remuneration. That thinking is sensible. What often gets less attention is the compliance backbone needed to support it.

An employment related securities return is that backbone. It’s the annual HMRC reporting process for share-related events connected with employees and directors. If the company gets it right, the scheme remains a genuine business tool. If it gets it wrong, the burden falls on finance, payroll and often the board.

Why this matters to Finance Directors

For a business in the £1 million to £15 million turnover range, ERS rarely sits neatly in one team. Legal documents may sit with external advisers. Payroll may hold some tax information. HR may know who joined and left. The cap table may sit with founders or the company secretary. That split is exactly why problems arise.

Practical rule: If equity data lives in four places, the annual return will usually be harder, slower and riskier than expected.

A strong ERS process does three things:

- Protects the value of the incentive by reducing the chance that employees face confusion later.

- Protects cash flow by avoiding unnecessary penalties and last-minute remediation work.

- Protects management time because the business can file from an organised transaction log rather than reconstructing events after year end.

The companies that handle ERS well don’t treat it as a one-off tax form. They treat it as an annual output of a year-round process.

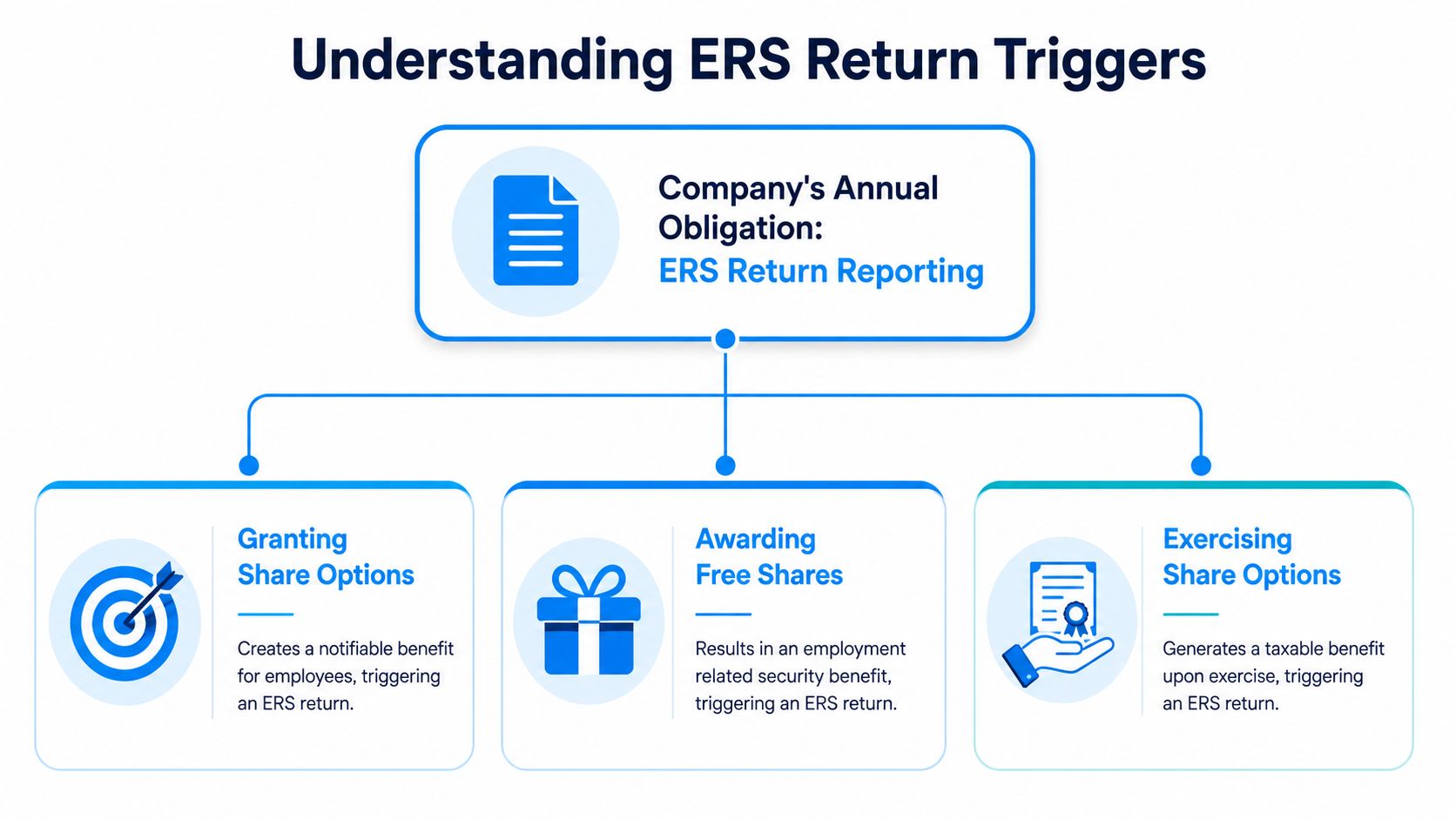

What Events Trigger an ERS Return

An employment related securities return is the company’s annual report to HMRC for share and securities events involving employees or directors in the previous tax year. The obligation sits with the employer. It isn’t something employees file themselves.

The scope is wider than many directors expect. UK ERS reporting covers grants and exercises of options, RSU awards, acquisitions of shares or securities, and certain disposals. HMRC expects reporting even where the securities are modest in value or paid for at market value, which shows how widely the regime captures employment-linked equity compensation, as outlined in Alvarez & Marsal’s ERS reporting overview.

Common reportable events in growing companies

The usual triggers include:

- Granting share options. This includes tax-advantaged and non-tax-advantaged options granted to employees or directors.

- Exercising options. When an employee turns an option into actual shares, that event is usually reportable.

- Awarding RSUs or similar rights. If the business uses more modern equity structures, the reporting obligation still needs checking.

- Issuing shares directly to staff. This often arises with growth shares, founder succession planning or senior recruitment packages.

- Acquiring shares or securities. Even where an employee pays what the company believes is market value, the event may still fall within ERS reporting.

- Disposals and transfers in some cases. If shares move out, rights change or securities are otherwise dealt with, the position needs reviewing.

- Changes, cancellations or lapses. An amendment to rights can be just as important as an initial grant.

What catches businesses out

The mistake isn’t usually failing to understand one dramatic transaction. It’s missing the quieter ones. A director acquires shares on joining. An option lapses after a leaver deadline. A small award is made to a new management hire and everyone assumes it’s too minor to matter.

An ERS review should follow the employment connection, not just the tax charge.

For directors who want broader context on how stock option structures differ conceptually, especially when comparing international terminology, Jumpstart Partners’ stock option insights can be a useful background read. The UK filing question still turns on HMRC’s ERS rules, but the commercial design issues often start earlier.

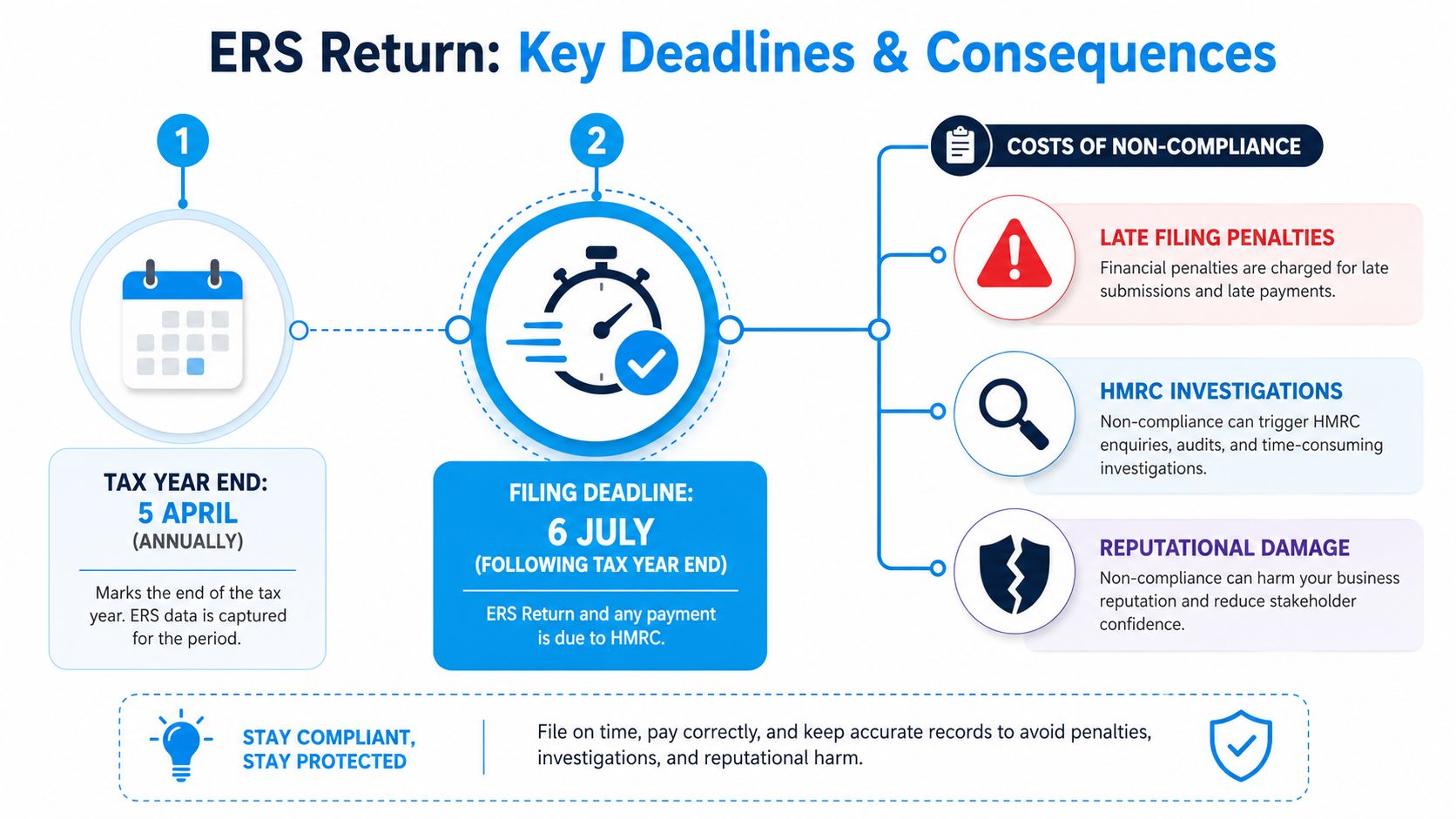

Key Deadlines and The Cost of Getting It Wrong

There is one date finance teams need in the diary early. ERS returns cover the tax year ending 5 April and must be filed by 6 July. HMRC warns that missing the deadline can trigger penalties, and the filing timetable is set out on HMRC’s ERS filing guidance.

The penalty path is simple

BDO notes the late filing sequence as:

| Date | Consequence |

|---|---|

| 6 July | filing deadline passes |

| Initial late filing | £100 penalty |

| 6 October | further £300 penalty if still outstanding |

| 6 January | further £300 penalty if still outstanding |

That sequence matters because ERS penalties don't usually arrive at a convenient time. They hit after the filing failure, when management is already dealing with quarter-end pressure, audit work or payroll cycles. What should have been a routine filing turns into avoidable cash leakage and internal distraction.

Why missed deadlines usually point to a process problem

Late filing is rarely just a diary issue. It usually means one of three things happened:

- Ownership wasn't clear. Finance assumed payroll had the data, payroll assumed legal had it, and nobody owned the full return.

- The scheme stayed off the operational radar. The business set it up correctly, then didn't maintain a live reporting log.

- Supporting records were weak. Market values, employee details or tax handling had to be rebuilt at the last minute.

For teams tightening controls across payroll and sensitive employee data at the same time, this broader guide to Payroll and data privacy compliance is often useful context. ERS doesn't sit in isolation from the rest of the people-data environment.

A practical way to avoid deadline drift is to align ERS with the rest of the company's compliance calendar, alongside other limited company filing deadlines.

Navigating Common Pitfalls and Exemptions

The obvious ERS errors are usually picked up. The expensive ones are the quiet administrative misses.

The nil return trap

A company registers a scheme, doesn't use it during the year, and assumes there's nothing to file. That assumption can be wrong. HMRC may still expect a nil return for an open scheme even where no reportable events occurred. Whitings also notes that securities generally cease to be employment-related seven years after an employee leaves, which matters when dealing with later events for leavers, as explained in Whitings' ERS guidance.

That creates two practical rules. First, don't assume inactivity means no filing. Second, don't assume a leaver is irrelevant just because they've gone.

Mini-scenarios that come up often

-

An inactive EMI scheme

The company granted options in an earlier year but had no new grants, exercises or changes in the latest tax year. The scheme is still open on HMRC's system. A nil return may still be required. -

A leaver with old options

A former employee keeps rights that remain capable of creating a reportable event. If the company stopped tracking them after departure, finance may miss the later reporting requirement. -

A management hire buying shares at perceived market value

The board views the deal as commercial and assumes ERS doesn't apply because no discount was intended. The reporting regime is broader than that.

The safest question isn't “Was there tax?” It's “Was there an employment-linked securities event?”

What doesn't work

Leaving ERS until June rarely works well if the business has any of the following:

- Leavers with outstanding rights

- Cross-border employees

- More than one type of award

- Historic schemes that were never formally cleaned up

A year-end reconstruction tends to produce patchy employee data, uncertainty over market value support and avoidable debate about whether PAYE or NIC treatment was applied correctly.

What works better

A cleaner control model usually includes:

- One owner in finance who coordinates legal, payroll and HR inputs.

- A live event log updated whenever options, shares or rights move.

- Leaver procedures that ask whether any securities remain within the regime.

- Periodic checks on whether old or unused schemes should still remain open.

If HMRC obligations have become muddled across filings more generally, a review against the company's wider HMRC tax check process can help identify where the control gaps really sit.

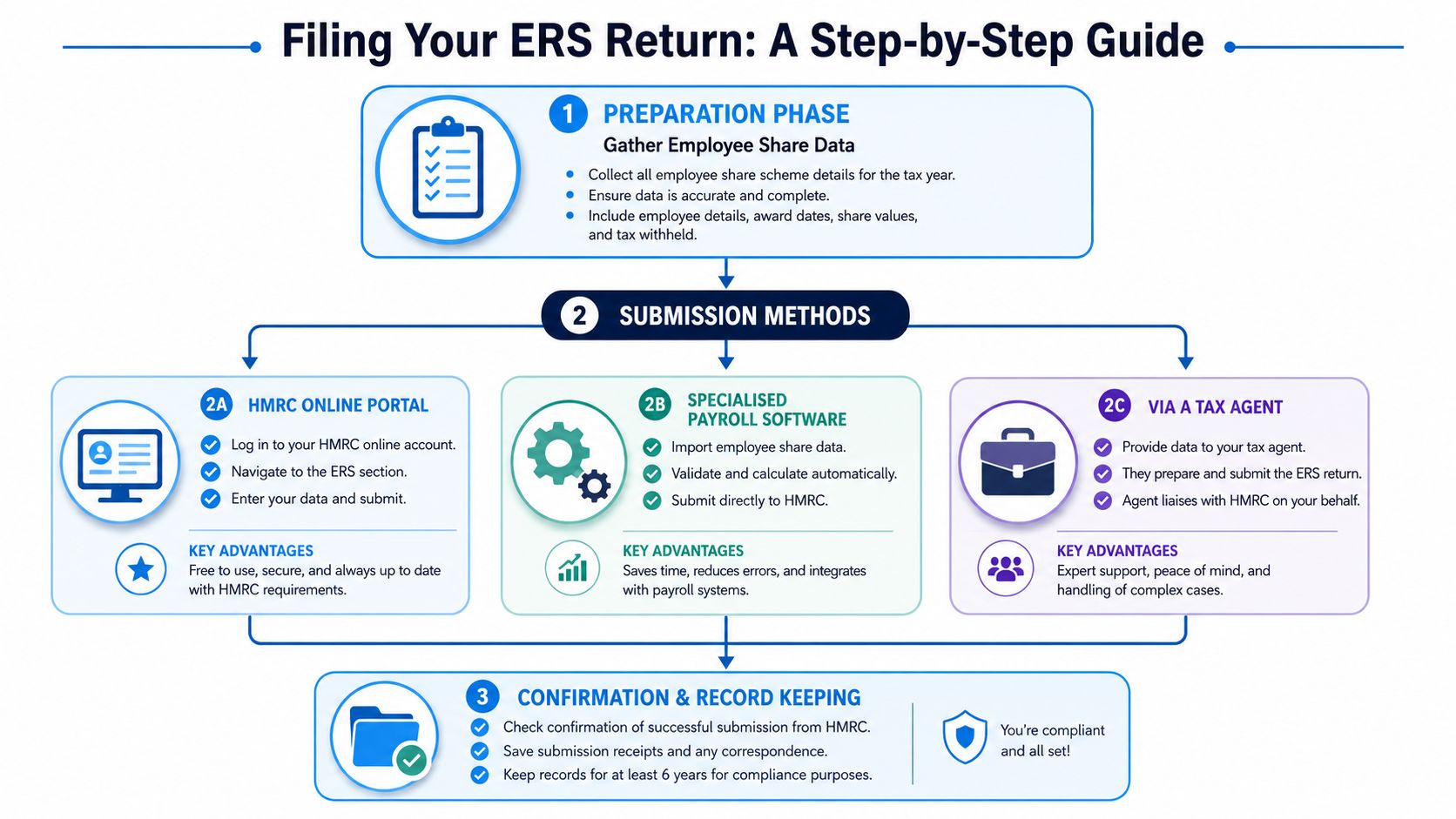

A Step-by-Step Guide to Filing Your ERS Return

Good filing starts long before the submission window opens. The return needs technically specific data, not broad descriptions. Blick Rothenberg notes that a compliant ERS return requires the issuer's details, each employee's name and NI number, security type and quantity, restrictions affecting market value, market value, amounts paid and whether PAYE/NIC was applied. Their summary also makes the operational point clearly. Equity events should be tracked at transaction level throughout the year, as set out in Blick Rothenberg's ERS reporting guidance.

Step one Gather the right data

Before choosing a filing route, the business needs a complete dataset. That usually means pulling together:

- Issuer information for the company whose shares or securities are involved

- Employee identifiers, including names and NI numbers

- Transaction details, including dates, type of event and quantities

- Security details, such as the class of share or nature of the option

- Restrictions and valuations that affect market value

- Amounts paid by the employee

- PAYE and NIC treatment, where relevant

Many SMEs lose time. The documents exist, but they haven't been captured in a structured way.

Step two Choose the filing route

Most businesses use one of three routes.

Filing direct through HMRC

This can work if the volume of events is low and the internal records are clean. The advantage is control. The downside is that finance still needs to interpret the data correctly and upload it in the right format.

Filing through software

This suits businesses that already maintain structured payroll or share-plan records and want a more repeatable process. It can reduce manual rekeying, but only if the underlying data is accurate in the first place.

Filing through an authorised agent

This is often the most practical route when the company has multiple schemes, unusual awards, leavers or mobile employees. The company still owns the data quality, but an adviser can pressure-test the treatment and manage submission mechanics.

Operational test: If finance would struggle to explain every equity event from a single spreadsheet, the issue is data capture, not filing method.

Step three Prepare for the submission format

HMRC's ERS service uses templates in CSV or ODS format. That sounds straightforward, but it forces discipline. Inconsistent naming, incomplete NI numbers or unclear event descriptions create friction quickly.

A useful internal checkpoint is to test whether the company could populate the template accurately without searching old email chains. If not, the process needs tightening before next year.

Step four Keep evidence after filing

Submission isn't the end of the job. Finance should retain:

- Board approvals and award documents

- Valuation support

- Employee communications

- Payroll treatment evidence

- A final filed copy and submission confirmation

If a new scheme or employer registration issue is holding up the wider process, the company may also need support with registering with HMRC.

Worked Examples for Common SME Share Schemes

Abstract rules become easier when tied to ordinary business activity. These examples focus on what needs to be captured for the employment related securities return, not the full tax analysis.

EMI option grant to key developers

A software company grants EMI options to three developers during the tax year. Nothing is exercised yet. For ERS purposes, the company needs to record the grant details for each employee, the nature of the option, the number covered and the relevant employee identifiers.

The reporting point isn't delayed just because no cash changed hands. The grant itself is the event that must be tracked properly.

Unapproved option exercise by a sales director

A manufacturing business gave a sales director unapproved options in an earlier year. During the latest tax year, the director exercises them and receives shares. The company needs to capture the exercise event, the quantity involved, the relevant market value information, any amount paid and whether PAYE/NIC treatment was handled.

Often, finance and payroll need to coordinate closely. If the data sits in separate places, the return becomes harder than it should be.

Growth shares for a newly recruited operations director

A logistics business recruits an Operations Director and issues growth shares as part of the package. The board may see this as a commercial investment by the individual rather than a remuneration event. ERS still needs reviewing because the acquisition is linked to employment.

The return should reflect the acquisition details, the security type, the employee information, any restrictions affecting value and what the individual paid.

What these examples have in common

All three scenarios depend on the same discipline:

- Capture the event when it happens

- Record who was involved

- Retain support for valuation and restrictions

- Check the payroll interaction early

The filing itself is usually the easy part once those basics are in place.

Your ERS Compliance Checklist and Next Steps

Finance teams don't need a perfect system. They need a system that is clear, owned and repeatable.

A practical checklist

- Identify every open scheme and confirm whether it remains active on HMRC's system.

- Maintain a live log of share-related events across grants, exercises, acquisitions, lapses, transfers and leavers.

- Make one person accountable for pulling data from payroll, HR, legal and company secretarial records.

- Check leaver files carefully where rights may still exist after departure.

- Document valuation support and restrictions at the point of transaction, not months later.

- Review nil return exposure for any scheme with no activity.

- Diarise the filing cycle early so the return isn't left to the end of June.

ERS compliance works best when it is built into the company's incentive process, not bolted on after the event.

For many businesses, that's a significant shift. The return is not just an annual submission. It is evidence that the company can control the tax and data consequences of its incentive strategy.

ERS Return Frequently Asked Questions

Do all employee share schemes need an employment related securities return?

Most share, option and securities transactions involving UK employees or directors need review for ERS reporting. The regime is broad and can apply even where the employee paid market value or the amounts involved seem modest. The obligation sits with the company.

Do you need to file an ERS return if nothing happened in the year?

Potentially, yes. If a scheme is still open on HMRC's system, a nil return may still be required even when there were no reportable events in the tax year. Inactivity doesn't automatically remove the filing obligation.

What information is needed for an ERS return?

The return can require issuer details, employee names and NI numbers, the security type, quantities, restrictions affecting market value, market value, amounts paid and whether PAYE/NIC was applied. That's why year-round record keeping matters.

What happens if an employee left years ago?

A leaver doesn't automatically fall outside the regime. Securities generally cease to be employment-related seven years after the employee leaves, so businesses should keep leaver records under review where rights or holdings remain relevant.

Can an accountant file the employment related securities return for the company?

Yes, an authorised agent can handle the submission process. That often helps where there are multiple awards, difficult valuations or cross-team data issues. The company still needs to provide complete and accurate underlying information.

If the company has employee shares, options or growth shares and there's any doubt over what should be reported, striveX Ltd can help review the position, tidy the process and support filing. A focused conversation can usually identify the gaps quickly and show whether the issue is scheme design, payroll coordination or missing data. This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.