A Finance Director hears “pension salary sacrifice changes” and the first question usually isn’t about policy detail. It’s about cost. What happens to employer NIC, what happens to take-home pay for affected staff, and whether this gradually becomes a wider remuneration problem.

That reaction is the right one. The salary sacrifice budget changes aren’t just a tax technicality for pension specialists. They affect payroll design, cash flow forecasting, reward strategy, employee expectations, and the way leadership teams explain compensation decisions.

For SMEs, this matters because salary sacrifice often sits in the middle of several moving parts. Pension policy, payroll processing, budgeting, annual pay reviews, and benefit communications all connect. If one piece changes, the knock-on effects rarely stay in one department.

Introduction The Budget Change Targeting Your Payroll

The headline change is simple, but the commercial effect isn’t.

From April 2029, the government will limit the amount of pension contribution that can be made through salary sacrifice without National Insurance contributions to £2,000 per employee per year, according to the government’s policy paper on changes to salary sacrifice for pensions from April 2029. Salary sacrifice above that level will still be allowed. It just won’t keep the same NIC treatment on the excess.

That creates a new decision for employers. Leave arrangements largely as they are and accept more NIC cost on the excess, or redesign how pensions fit into the wider reward package.

Why this matters to SME leadership teams

For a growing business, this sits in an awkward place. It’s not immediate enough to force action this quarter, but it’s too material to leave until 2028. Boards that delay will likely end up with rushed payroll changes, weak employee messaging, and poor budgeting assumptions.

Three teams need to care now:

- Finance needs a costed view of future employer NIC exposure.

- Payroll needs system and reporting readiness.

- HR and leadership need a plan for how pension changes affect overall remuneration conversations.

Commercial view: A pension tax change can quickly become a margin issue if employer NIC rises across a broad employee base and no one has built that into forecasts.

The right approach isn’t panic. It’s early modelling, deliberate communication, and a realistic review of whether the current salary sacrifice structure still supports the business.

Decoding the New Salary Sacrifice Pension Rules

The practical rule is straightforward. If the announced reform takes effect from April 2029, the first £2,000 of pension salary sacrifice each year is expected to keep NIC relief, while any amount above that limit is expected to lose that treatment for both employer and employee NIC purposes.

What actually changes

For SME finance leaders, the point to grasp is not the pension contribution itself. It is the split in NIC treatment.

Under the announced policy:

- The first £2,000 of salary sacrificed for pension contributions is expected to remain outside NIC.

- Any sacrificed amount above £2,000 is expected to become subject to employee and employer NIC.

- Ordinary employer pension contributions are still expected to remain exempt, which keeps them relevant in any redesign of pay and pension structures.

That distinction drives strategy. Salary sacrifice would still exist if the measure goes ahead, but its tax efficiency would be narrower for higher sacrifice amounts. In practice, that means businesses with a broad-based 5% sacrifice arrangement may see little change for some staff and a more meaningful cost shift for others, especially where contribution rates rise with seniority or long service.

How to explain the rule inside the business

Managers usually need a version they can repeat without creating confusion. A clear line is enough: salary sacrifice for pensions is not due to disappear, but the NIC benefit is planned to be limited above an annual cap.

That matters because poor wording creates avoidable problems. Employees may assume the pension itself is being taxed more heavily, or that the employer is cutting benefits, when the issue is the NIC treatment on the slice above the threshold. HR and payroll should agree that wording early, then use it consistently in FAQs, template emails, and manager briefings.

A quick HMRC tax check for payroll planning can also help finance teams test where sacrifice arrangements may start creating extra NIC cost under the proposed rules.

The point finance teams should model properly

A worked example helps. An employee sacrificing a modest amount above the cap may only create a small extra NIC cost, which can make the reform look minor at first glance.

That is where boards can get caught out.

If the policy is implemented as announced, the issue is not one employee who is £250 over the limit. It is the cumulative payroll cost across everyone above it, month after month, plus the knock-on effect on pay review discussions and total reward design. Businesses that want a cleaner answer before budgets are locked should model three things now: how many employees are likely to exceed the cap, what the added employer NIC could look like under different contribution patterns, and whether part of the current sacrifice structure should eventually move into ordinary employer contributions instead.

Why payroll design matters

This is also a systems issue. Payroll teams will need rules that separate the NIC-efficient portion from the excess, apply the right treatment consistently, and produce reporting that can stand up to review.

Scheme documents and salary sacrifice agreements may need attention too. If the paperwork still describes salary sacrifice as fully NIC-efficient, it could misstate the position once the proposed cap takes effect. The best time to review those documents is well before any implementation date, while there is still time to test payroll calculations, update employee communications, and decide whether the existing remuneration structure still does the job.

The Financial Impact on Your Business and Employees

This is a major revenue-raising measure. The reform is forecast to raise up to £4.7 billion in 2029-30 and £2.6 billion in 2030-31, and analysis notes that around 7.5 million employees currently use salary sacrifice for pension contributions, according to TLT’s summary of the Budget 2025 pension salary sacrifice changes.

For SME employers, the important point isn’t the national total. It’s that a tax measure designed to raise that much is unlikely to stay invisible inside company payroll costs.

The impact won’t be even across your workforce

The cost isn’t linear. Staff contributing just above the cap may see a small change. Staff sacrificing materially more can create a larger NIC drag for both employer and employee.

A simple planning table helps boards see where the pressure appears.

| Gross Salary | Sacrifice Amount (5%) | Excess over £2,000 Cap | Annual Extra Employer NI | Annual Extra Employee NI |

|---|---|---|---|---|

| £45,000 | £2,250 | £250 | £34 | £30 |

| Below the point where 5% stays within the cap | Qualitative only | None | None | None |

| Higher salary levels with larger sacrificed amounts | Qualitative only | More excess | Higher cost | Higher cost |

Only the first row uses HMRC's published example. The other rows are shown qualitatively because no further verified figures are available.

What this means for business budgeting

Most finance teams should test at least three scenarios:

-

Absorb the extra employer NIC cost

This keeps the employee offer stable, but pushes the cost into payroll budgets. -

Redesign the pension arrangement

This may reduce future NIC leakage, but can create employee relations and documentation work. -

Offset elsewhere in remuneration

This can protect margin, but often shifts pressure into pay reviews, bonuses, or benefit decisions.

Board question: If the business absorbs the additional NIC cost, where does that sit in the model. Gross margin, overhead base, or reduced headroom for future reward increases?

The employee side matters as much as the employer side

If affected employees see lower net pay than expected, the conversation won't stay inside payroll. It usually lands with line managers first, then with HR, then back with finance during pay review season.

That's why these salary sacrifice budget changes shouldn't be modelled only as a tax issue. They need to be built into workforce planning assumptions and salary review messaging.

A useful control step is to stress-test payroll data now and identify who currently sacrifices above the future cap. Businesses that want a quick sense check on wider HMRC risk areas can also use an HMRC tax check resource as part of a broader compliance review.

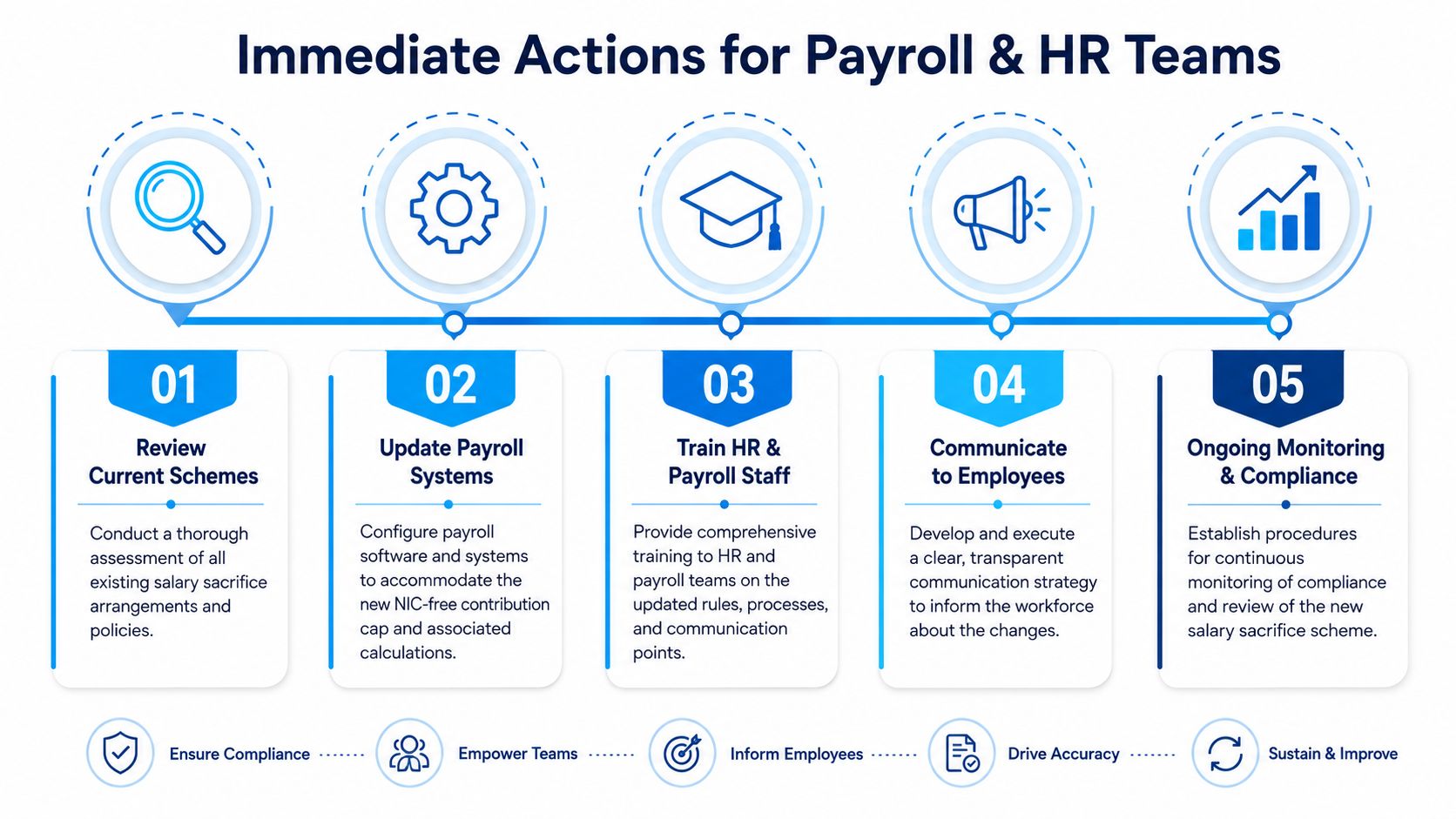

Immediate Actions for Your Payroll and HR Teams

The best time to prepare is well before any formal employee communication. Once a message goes out, staff expect answers, not caveats.

Immediate reviews

Start with the facts inside the current scheme.

- Map current participants and identify which employees already sacrifice above the future NIC-efficient cap.

- Review scheme rules and employment wording so leadership knows what can be changed administratively and what may require consultation.

- Identify who owns the decision-making between finance, payroll, HR, and pensions governance.

This first pass often reveals a practical gap. Many businesses know they operate salary sacrifice, but don't have a clean management view of who uses it, at what level, and whether employer NIC savings are shared back through pension contributions or retained by the business.

Mid-term modelling

Once the population is clear, the next step is forecasting.

- Build a payroll impact model using current contribution patterns and likely future headcount.

- Test different remuneration responses, including absorbing cost, changing contribution structures, or adjusting benefit policy.

- Assess knock-on effects on annual budgeting, pay reviews, and benefit affordability.

Many SMEs benefit from external support. A broader finance consultancy service can help turn a payroll rule change into a board-level decision model rather than a narrow compliance exercise.

A strong model doesn't just ask, “What extra NIC might arise?” It also asks, “What response creates the fewest downstream problems?”

Long-term system preparation

The administrative side needs attention as well. Analysis notes that employers will need payroll reporting of total sacrificed amounts through existing software from April 2029, making this a structural payroll and benefits change rather than a complete end to salary sacrifice.

That means teams should:

- Speak to payroll software providers early about how the new reporting and calculation process will work.

- Document process ownership for year-round monitoring rather than treating this as a one-off update.

- Train payroll and HR staff so employee queries get consistent answers.

A rushed implementation usually causes two avoidable problems. Incorrect deductions, and inconsistent employee messaging.

Communicating Salary Sacrifice Changes to Your Workforce

Most businesses focus first on tax mechanics. Staff focus on what changes on their payslip and whether the company is taking something away.

That's why communication can't be an afterthought. If the message is vague, late, or defensive, employees often assume the business is making a discretionary cut rather than responding to a government policy change.

What good communication sounds like

The strongest messages are usually direct and calm:

- Explain the cause clearly. This is a government policy change, not a new internal deduction.

- Be precise about who may be affected. Don't alarm employees whose contribution levels are unlikely to change.

- Set out the company's review process. Staff cope better with change when they know what decisions are still being considered and when they'll hear more.

Employees don't expect tax law to stay still. They do expect their employer to explain changes in plain English.

A practical message structure

A company-wide announcement usually works best when it follows this order:

-

What's changing

Keep it factual and avoid jargon-heavy pension language. -

When it takes effect

Give context that planning is happening in advance. -

Who is more likely to notice an impact

Avoid creating concern across the full workforce if only part of the population is likely to feel it. -

What the company is doing now

Reviewing payroll, pension arrangements, and support materials. -

Where staff can ask questions

A named route matters. Generic inboxes often create frustration.

Line managers also need a separate briefing. They shouldn't be left improvising answers on take-home pay, pensions, or why policy is changing. Teams looking to improve how leaders handle these conversations may find RedactAI's executive communication guide helpful as a practical framework for clearer briefings and tougher employee conversations.

What doesn't work

Three communication mistakes show up repeatedly:

-

Over-reassuring too early

If leadership says “no one will be affected” before modelling is complete, trust can fall quickly. -

Using payroll language without explanation

Terms like sacrificed earnings, exempt contributions, and NIC treatment often confuse rather than reassure. -

Treating this as only an HR memo

Employees read benefit changes as a statement about company priorities. Finance, leadership, and managers need a shared line.

Strategic Alternatives and Remuneration Planning

The weakest response is to assume the business should absorb the extra cost and move on.

Independent analysis from the IFS describes the policy as a substantial reform and highlights an important commercial question: whether employers will absorb the extra NIC cost or respond by changing compensation structures such as freezing pay or trimming benefits, potentially affecting a wider group of staff, as discussed in the IFS assessment of the reform to National Insurance treatment for salary sacrifice pensions.

Option one and keep salary sacrifice but accept the cost

This is the least disruptive route operationally.

It may suit businesses where pension participation is a core part of the employer proposition and leadership wants stability more than optimisation. The downside is obvious. Employer NIC cost can rise while the business still carries the administration of a more complex arrangement.

Option two and cap the salary sacrifice design

Some employers may choose to limit NIC-efficient salary sacrifice behaviour around the future threshold and redesign pension communications accordingly.

That can improve cost control and make payroll outcomes more predictable. But it can also frustrate higher-contributing employees who value the current structure and see pensions as part of their personal financial planning.

Decision test: If the scheme changed tomorrow, would the leadership team still design it in the same way from scratch?

Option three and shift emphasis to employer contributions or a hybrid model

Because ordinary employer pension contributions remain exempt, some businesses may review whether a different blend of employer contribution and employee arrangement better fits the post-2029 environment.

That isn't automatically better. It changes employee perception, may require consultation, and can alter how staff think about flexibility and control. But it deserves proper modelling rather than dismissal.

The wider remuneration question

These salary sacrifice budget changes can spill into areas that look unrelated at first glance:

- Annual pay reviews

- Bonus design

- Benefit selection

- Retention discussions for senior or specialist staff

A remuneration package works as a system. If one tax-efficient element loses value, leadership may need to decide whether to replace that value elsewhere, leave it as is, or reposition the package more realistically around affordability.

That's why this belongs inside wider financial strategy planning for growing companies, not just pension administration.

Employees may also need help understanding their own budgeting trade-offs if contribution patterns change. For that reason, a practical resource such as this comprehensive professional budgeting guide can support internal signposting without turning the employer into a personal finance adviser.

What usually works best

The most effective approach is rarely a blanket answer.

For many SMEs, the sensible path is to segment the workforce, model the cost by employee group, decide what outcome matters most, and then align pension policy with the broader reward strategy. Businesses that skip that step often end up with a scheme that is technically compliant but commercially untidy.

Frequently Asked Questions

Will salary sacrifice for pensions end in 2029

No. Salary sacrifice can still be used. The change is that only the first £2,000 per employee per year keeps NIC-free treatment for pension salary sacrifice, while the excess becomes subject to employee and employer NICs.

Do employers still save National Insurance on pension salary sacrifice

Yes, but only within the NIC-efficient portion covered by the new rules. Above the cap, the employer NIC advantage on the excess falls away, so the business needs to model whether the arrangement still works commercially.

Should SMEs change pension arrangements now

Most SMEs shouldn't rush into rewriting schemes immediately. They should review current participation, model future cost exposure, and decide whether the existing remuneration structure still makes sense before changing contracts or communications.

Will this affect only higher earners

Not necessarily. The direct NIC impact falls on employees whose sacrificed pension contributions exceed the cap, but wider effects can spread further if employers respond by changing compensation structures, benefits, or pay review decisions.

If these salary sacrifice budget changes raise questions about payroll cost, cash flow forecasting, or remuneration strategy, striveX Ltd can help. The team works with growing UK businesses to model financial impact, review payroll and pension arrangements, and support commercially sound decisions before changes hit the P&L. Book a conversation through the contact page and expect a practical response focused on next steps, not jargon.

This article is for informational purposes only and does not constitute professional advice. Tax rules apply as of April 2026. Consult a qualified accountant for your specific circumstances.